Code

source("../dsan-globals/_globals.r")DSAN 5650: Causal Inference for Computational Social Science

Summer 2026, Georgetown University

Today’s Planned Schedule:

| Start | End | Topic | |

|---|---|---|---|

| Lecture | 6:30pm | 7:00pm | Final Project Templates → |

| 7:00pm | 7:30pm | Propensity Score Weighting → | |

| 7:30pm | 8:00pm | Regression Discontinuity → | |

| Break! | 8:00pm | 8:10pm | |

| 8:30pm | 9:00pm | Violations of Causal Inference Axioms in NLP and Network Analysis → |

source("../dsan-globals/_globals.r")\[ \DeclareMathOperator*{\argmax}{argmax} \DeclareMathOperator*{\argmin}{argmin} \newcommand{\bigexp}[1]{\exp\mkern-4mu\left[ #1 \right]} \newcommand{\bigexpect}[1]{\mathbb{E}\mkern-4mu \left[ #1 \right]} \newcommand{\definedas}{\overset{\small\text{def}}{=}} \newcommand{\definedalign}{\overset{\phantom{\text{defn}}}{=}} \newcommand{\eqeventual}{\overset{\text{eventually}}{=}} \newcommand{\Err}{\text{Err}} \newcommand{\expect}[1]{\mathbb{E}[#1]} \newcommand{\expectsq}[1]{\mathbb{E}^2[#1]} \newcommand{\fw}[1]{\texttt{#1}} \newcommand{\given}{\mid} \newcommand{\green}[1]{\color{green}{#1}} \newcommand{\heads}{\outcome{heads}} \newcommand{\iid}{\overset{\text{\small{iid}}}{\sim}} \newcommand{\lik}{\mathcal{L}} \newcommand{\loglik}{\ell} \DeclareMathOperator*{\maximize}{maximize} \DeclareMathOperator*{\minimize}{minimize} \newcommand{\mle}{\textsf{ML}} \newcommand{\nimplies}{\;\not\!\!\!\!\implies} \newcommand{\orange}[1]{\color{orange}{#1}} \newcommand{\outcome}[1]{\textsf{#1}} \newcommand{\param}[1]{{\color{purple} #1}} \newcommand{\pgsamplespace}{\{\green{1},\green{2},\green{3},\purp{4},\purp{5},\purp{6}\}} \newcommand{\pedge}[2]{\require{enclose}\enclose{circle}{~{#1}~} \rightarrow \; \enclose{circle}{\kern.01em {#2}~\kern.01em}} \newcommand{\pnode}[1]{\require{enclose}\enclose{circle}{\kern.1em {#1} \kern.1em}} \newcommand{\ponode}[1]{\require{enclose}\enclose{box}[background=lightgray]{{#1}}} \newcommand{\pnodesp}[1]{\require{enclose}\enclose{circle}{~{#1}~}} \newcommand{\purp}[1]{\color{purple}{#1}} \newcommand{\sign}{\text{Sign}} \newcommand{\spacecap}{\; \cap \;} \newcommand{\spacewedge}{\; \wedge \;} \newcommand{\tails}{\outcome{tails}} \newcommand{\Var}[1]{\text{Var}[#1]} \newcommand{\bigVar}[1]{\text{Var}\mkern-4mu \left[ #1 \right]} \]

HERO or VILLAIN)library(tidyverse) |> suppressPackageStartupMessages()

rug_df <- read_csv("assets/rugged_data.csv", show_col_types=FALSE)

# Compute Box-Cox params

bc_params <- car::powerTransform(

object = cbind(

rug_df$rgdppc_2000,

rug_df$rugged

)

)

rug_df <- rug_df |> mutate(

continent = ifelse(cont_africa == 1, "African", "Non-African"),

gdpc_transformed = rgdppc_2000_m ^ bc_params$lambda[1],

rugged_transformed = rugged ^ bc_params$lambda[2],

)

rug_df |> ggplot(aes(

x = rugged_transformed,

y = gdpc_transformed

)) +

geom_text(aes(label=isocode), size=3) +

geom_smooth(method="lm", fullrange=TRUE) +

facet_wrap(~ continent) +

theme_classic() +

theme(

panel.background = ggplot2::element_rect(fill='transparent'),

plot.background = ggplot2::element_rect(fill='transparent', color=NA),

plot.title = element_text(hjust=0.5),

) +

labs(

title="Differential Effects of Ruggedness by Continent",

x="Terrain Ruggedness",

y="Log GDP Per Capita, 2000",

)

library(tidyverse)

library(Rlab)Rlab 4.5.1 attached.

Attaching package: 'Rlab'The following object is masked from 'package:dplyr':

countThe following object is masked from 'package:tibble':

viewThe following objects are masked from 'package:stats':

dexp, dgamma, dweibull, pexp, pgamma, pweibull, qexp, qgamma,

qweibull, rexp, rgamma, rweibullThe following object is masked from 'package:datasets':

precipset.seed(5650)

n <- 250

motiv_vals <- runif(n, 0, 1)

enroll_vals <- ifelse(

motiv_vals < 0.25,

0,

# We know motiv > 0.25

ifelse(

motiv_vals > 0.75,

1,

# We know 0.25 < motiv < 0.75

rbern(n, prob=(motiv_vals - 0.125)*1.5)

)

)Warning in rbinom(n, size = 1, prob = prob): NAs producedncigs_vals <- rbinom(n, size=30, prob=0.6-0.2*enroll_vals)

smoke_df <- tibble(

motiv=motiv_vals,

enroll=enroll_vals,

ncigs=ncigs_vals

)

(smoke_mean_df <- smoke_df |> group_by(enroll) |> summarize(mean_ncigs=mean(ncigs)))| enroll | mean_ncigs |

|---|---|

| 0 | 17.88060 |

| 1 | 12.26724 |

naive_smoke_lm <- lm(ncigs ~ enroll, data=smoke_df)

summary(naive_smoke_lm) |> broom::tidy() |>

select(term, estimate)| term | estimate |

|---|---|

| (Intercept) | 17.880597 |

| enroll | -5.613356 |

smoke_df |> ggplot(aes(x=enroll, y=ncigs)) +

geom_boxplot(

aes(group=enroll),

width=0.5

) +

geom_smooth(

method='lm',

formula='y ~ x',

se=TRUE

) +

geom_point(

data=smoke_mean_df,

aes(x=enroll, y=mean_ncigs),

size=3

) +

theme_dsan(base_size=24) +

transparent_bg() +

labs(

title="Naïve Estimate of Program Effectiveness",

x="Enrolled?",

y="Cigarettes Per Day",

) +

scale_x_continuous(breaks=c(0, 1))

eprop_model <- glm(enroll ~ motiv, family='binomial', data=smoke_df)

eprop_preds <- predict(eprop_model, type="response")

smoke_df <- smoke_df |> mutate(pred=eprop_preds)

# Use the preds to compute IPW

smoke_df <- smoke_df |> rowwise() |> mutate(

ipw=ifelse(enroll, 1/pred, 1/(1-pred))

) |> arrange(pred)

#smoke_df

smoke_df |> mutate(enroll=factor(enroll)) |>

ggplot(aes(x=motiv, y=ncigs, color=enroll)) +

geom_point() +

theme_dsan(base_size=24) +

labs(title="Before Weighting") +

transparent_bg()

smoke_df |> mutate(enroll=factor(enroll)) |>

ggplot(aes(

x=motiv, y=ncigs, color=enroll, size=ipw,

alpha=log(ipw-1)

)) +

geom_point() +

guides(alpha="none") +

theme_dsan(base_size=24) +

labs(title="After Weighting") +

transparent_bg()

smoke_df |>

ggplot(aes(x=motiv)) +

# Predictions

geom_point(

aes(y=enroll, color=factor(enroll))

) +

# Values

geom_point(

aes(y=pred, color=factor(enroll))

) +

labs(color="enroll") +

theme_dsan(base_size=24) +

transparent_bg() +

labs(title="Propensity to Enroll")

ipw_min <- min(smoke_df$ipw)

ipw_max <- max(smoke_df$ipw)

smoke_df <- smoke_df |> mutate(

ipw_scaled = (ipw - ipw_min) / (ipw_max - ipw_min)

)

smoke_df |>

ggplot(aes(x=motiv)) +

# Predictions

geom_point(

aes(y=enroll, color=factor(enroll))

) +

# Values

geom_point(

aes(y=ipw_scaled, color=factor(enroll))

) +

theme_dsan(base_size=24) +

transparent_bg() +

labs(

title="Inverse Probability-of-Treatment Weights (IPTW)",

color="enroll"

)↓

→

↑

lm_with_weights <- lm(ncigs ~ enroll,

data=smoke_df, weights=smoke_df$ipw

)

summary(lm_with_weights) |> broom::tidy() |>

select(term, estimate, std.error)| term | estimate | std.error |

|---|---|---|

| (Intercept) | 18.10133 | 0.2466712 |

| enroll | -5.66453 | 0.3571696 |

library(WeightIt)

W <- weightit(

enroll ~ motiv, data = smoke_df, ps="pred"

)

smoke_weighted_lm <- lm_weightit(

ncigs ~ enroll, data = smoke_df, weightit = W

)

summary(smoke_weighted_lm, ci = FALSE)

Call:

lm_weightit(formula = ncigs ~ enroll, data = smoke_df, weightit = W)

Coefficients:

Estimate Std. Error z value Pr(>|z|)

(Intercept) 18.1013 0.2479 73.02 <1e-06 ***

enroll -5.6645 0.5463 -10.37 <1e-06 ***

Standard error: HC0 robustW_default <- weightit(

enroll ~ motiv, data = smoke_df

)

smoke_default_lm <- lm_weightit(

ncigs ~ enroll, data = smoke_df,

weightit = W_default

)

summary(smoke_default_lm, ci = FALSE)

Call:

lm_weightit(formula = ncigs ~ enroll, data = smoke_df, weightit = W_default)

Coefficients:

Estimate Std. Error z value Pr(>|z|)

(Intercept) 18.1013 0.2441 74.16 <1e-06 ***

enroll -5.6645 0.5444 -10.41 <1e-06 ***

Standard error: HC0 robust (adjusted for estimation of weights)When one’s margin of victory switches from a negative number to a positive number, we would expect a large, discontinuous, positive jump in the personal wealth of electoral candidates, if serving in office actually financially benefits them. (Imai 2018)

library(tidyverse) |> suppressPackageStartupMessages()

# load the data and subset them into two parties

MPs <- read_csv("assets/mps.csv")Rows: 427 Columns: 10

── Column specification ────────────────────────────────────────────────────────

Delimiter: ","

chr (4): surname, firstname, party, region

dbl (6): ln.gross, ln.net, yob, yod, margin.pre, margin

ℹ Use `spec()` to retrieve the full column specification for this data.

ℹ Specify the column types or set `show_col_types = FALSE` to quiet this message.MPs |> head()| surname | firstname | party | ln.gross | ln.net | yob | yod | margin.pre | region | margin |

|---|---|---|---|---|---|---|---|---|---|

| Llewellyn | David | tory | 12.13591 | 12.135906 | 1916 | 1992 | NA | Wales | 0.0569040 |

| Morris | Claud | labour | 12.44809 | 12.448091 | 1920 | 2000 | NA | South West England | -0.0497383 |

| Walker | George | tory | 12.42845 | 10.349009 | 1914 | 1999 | -0.0571682 | North East England | -0.0415887 |

| Walker | Harold | labour | 11.91845 | 12.395034 | 1927 | 2003 | -0.0725089 | Yorkshire and Humberside | 0.0232952 |

| Waring | John | tory | 13.52022 | 13.520219 | 1923 | 1989 | -0.2696896 | Greater London | -0.2300058 |

| Brown | Ronald | labour | 12.46051 | 9.631837 | 1921 | 2002 | 0.3409587 | Greater London | 0.3679703 |

library(modelr)

library(tidyr)

library(broom)

Attaching package: 'broom'The following object is masked from 'package:modelr':

bootstrap## load the data

## Subset the data

labour_winners <- filter(MPs, party == "labour", margin > 0)

labour_losers <- filter(MPs, party == "labour", margin < 0)

tory_winners <- filter(MPs, party == "tory", margin > 0)

tory_losers <- filter(MPs, party == "tory", margin < 0)

### the regressions

labour_fit_win <- lm(ln.net ~ margin, data = labour_winners)

labour_fit_lose <- lm(ln.net ~ margin, data = labour_losers)

tory_fit_win <- lm(ln.net ~ margin, data = tory_winners)

tory_fit_lose <- lm(ln.net ~ margin, data = tory_losers)

y1_labour_win <- labour_winners %>%

data_grid(margin) %>%

add_predictions(labour_fit_win)

y2_labour_lose <- labour_losers %>%

data_grid(margin) %>%

add_predictions(labour_fit_lose)

y1_tory_win <- tory_winners %>%

data_grid(margin) %>%

add_predictions(tory_fit_win)

y2_tory_lose <- tory_losers %>%

data_grid(margin) %>%

add_predictions(tory_fit_lose)

## setting the ggplot theme

theme_set(theme_classic(base_size = 22))

## Labour

ggplot() +

geom_point(data = labour_winners,

mapping = aes(x = margin, y = ln.net), shape = 1, alpha=0.6) +

geom_point(data = labour_losers,

mapping = aes(x = margin, y = ln.net), shape = 1, alpha=0.6) +

geom_line(data = y1_labour_win,

mapping = aes(x = margin, y = pred),

color = "blue", size = 1, linewidth=2) +

geom_line(data = y2_labour_lose,

mapping = aes(x = margin, y = pred),

color = "blue", size = 1, linewidth=2) +

geom_vline(xintercept = 0,

linetype = "dashed") +

labs(x = "Margin of victory",

y = "log net wealth at death",

title = "Labour") +

xlim(-0.5, 0.5) +

ylim(6, 18) +

transparent_bg()Warning: Using `size` aesthetic for lines was deprecated in ggplot2 3.4.0.

ℹ Please use `linewidth` instead.

## Tory

ggplot() +

geom_point(data = tory_winners,

mapping = aes(x = margin, y = ln.net), shape = 1, alpha=0.6) +

geom_point(data = tory_losers,

mapping = aes(x = margin, y = ln.net), shape = 1, alpha=0.6) +

geom_line(data = y1_tory_win,

mapping = aes(x = margin, y = pred),

color = "blue", size = 1, linewidth=2) +

geom_line(data = y2_tory_lose,

mapping = aes(x = margin, y = pred),

color = "blue", size = 1, linewidth=1) +

geom_vline(xintercept = 0,

linetype = "dashed") +

labs(x = "Margin of victory",

y = "log net wealth at death",

title = "Tory") +

xlim(-0.5, 0.5) +

ylim(6, 18) +

transparent_bg()

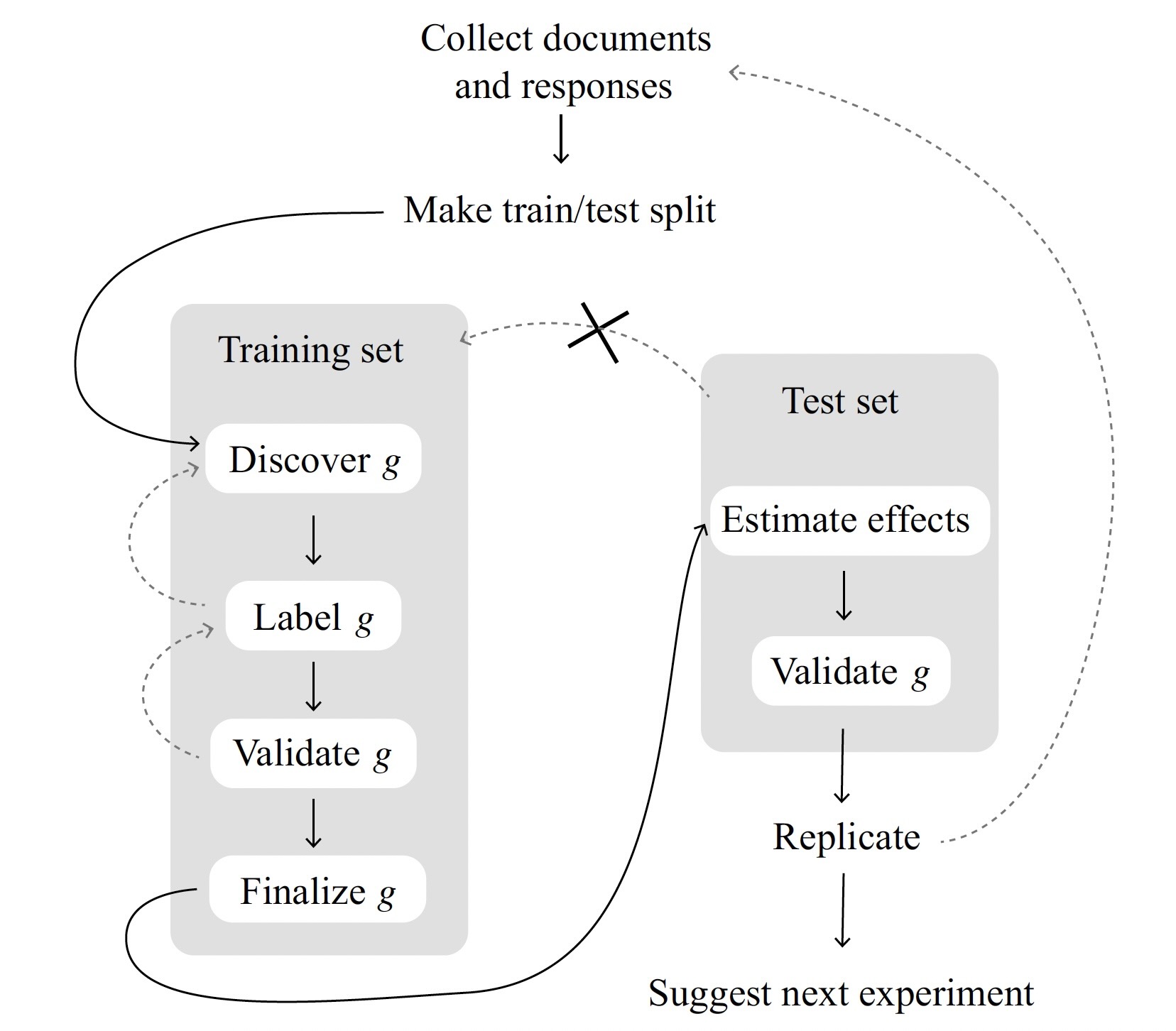

(The necessity for sample splitting!)

| \(Y_i \mid \textsf{do}(D_i \leftarrow 1)\) | \(Y_i \mid \textsf{do}(D_i \leftarrow 0)\) | |

|---|---|---|

| Person 1 | Candidate’s Morals | Taxes |

| Person 2 | Candidate’s Morals | Taxes |

| Person 3 | Polarization | Immigration |

| Person 4 | Polarization | Immigration |

| \(Y_i \mid \textsf{do}(D_i \leftarrow 1)\) | \(Y_i \mid \textsf{do}(D_i \leftarrow 0)\) | |

|---|---|---|

| Person 1 | Candidate’s Morals | Taxes |

| Person 2 | Candidate’s Morals | Taxes |

| Person 3 | Polarization | Immigration |

| Person 4 | Polarization | Immigration |

| Actual Assignment | Outcome \(Y_i\) | |

|---|---|---|

| Person 1 | \(D_1 = 1\) | Morals |

| Person 2 | \(D_2 = 1\) | Morals |

| Person 3 | \(D_3 = 0\) | Immigration |

| Person 4 | \(D_4 = 0\) | Immigration |

| Actual Assignment | Outcome \(Y_i\) | |

|---|---|---|

| Person 1 | \(D_1 = 1\) | Morals |

| Person 2 | \(D_2 = 0\) | Taxes |

| Person 3 | \(D_3 = 1\) | Polarization |

| Person 4 | \(D_4 = 0\) | Immigration |