Code

source("../dsan-globals/_globals.r")

set.seed(5300)DSAN 5300: Statistical Learning

Spring 2026, Georgetown University

What happens to my dependent variable \(Y\) when my independent variable \(X\) changes by 1 unit?

Whenever you carry out a regression, keep the goal in the front of your mind:

source("../dsan-globals/_globals.r")

set.seed(5300)\[ \DeclareMathOperator*{\argmax}{argmax} \DeclareMathOperator*{\argmin}{argmin} \newcommand{\bigexp}[1]{\exp\mkern-4mu\left[ #1 \right]} \newcommand{\bigexpect}[1]{\mathbb{E}\mkern-4mu \left[ #1 \right]} \newcommand{\definedas}{\overset{\small\text{def}}{=}} \newcommand{\definedalign}{\overset{\phantom{\text{defn}}}{=}} \newcommand{\eqeventual}{\overset{\text{eventually}}{=}} \newcommand{\Err}{\text{Err}} \newcommand{\expect}[1]{\mathbb{E}[#1]} \newcommand{\expectsq}[1]{\mathbb{E}^2[#1]} \newcommand{\fw}[1]{\texttt{#1}} \newcommand{\given}{\mid} \newcommand{\green}[1]{\color{green}{#1}} \newcommand{\heads}{\outcome{heads}} \newcommand{\iid}{\overset{\text{\small{iid}}}{\sim}} \newcommand{\lik}{\mathcal{L}} \newcommand{\loglik}{\ell} \DeclareMathOperator*{\maximize}{maximize} \DeclareMathOperator*{\minimize}{minimize} \newcommand{\mle}{\textsf{ML}} \newcommand{\nimplies}{\;\not\!\!\!\!\implies} \newcommand{\orange}[1]{\color{orange}{#1}} \newcommand{\outcome}[1]{\textsf{#1}} \newcommand{\param}[1]{{\color{purple} #1}} \newcommand{\pgsamplespace}{\{\green{1},\green{2},\green{3},\purp{4},\purp{5},\purp{6}\}} \newcommand{\pedge}[2]{\require{enclose}\enclose{circle}{~{#1}~} \rightarrow \; \enclose{circle}{\kern.01em {#2}~\kern.01em}} \newcommand{\pnode}[1]{\require{enclose}\enclose{circle}{\kern.1em {#1} \kern.1em}} \newcommand{\ponode}[1]{\require{enclose}\enclose{box}[background=lightgray]{{#1}}} \newcommand{\pnodesp}[1]{\require{enclose}\enclose{circle}{~{#1}~}} \newcommand{\purp}[1]{\color{purple}{#1}} \newcommand{\sign}{\text{Sign}} \newcommand{\spacecap}{\; \cap \;} \newcommand{\spacewedge}{\; \wedge \;} \newcommand{\tails}{\outcome{tails}} \newcommand{\Var}[1]{\text{Var}[#1]} \newcommand{\bigVar}[1]{\text{Var}\mkern-4mu \left[ #1 \right]} \]

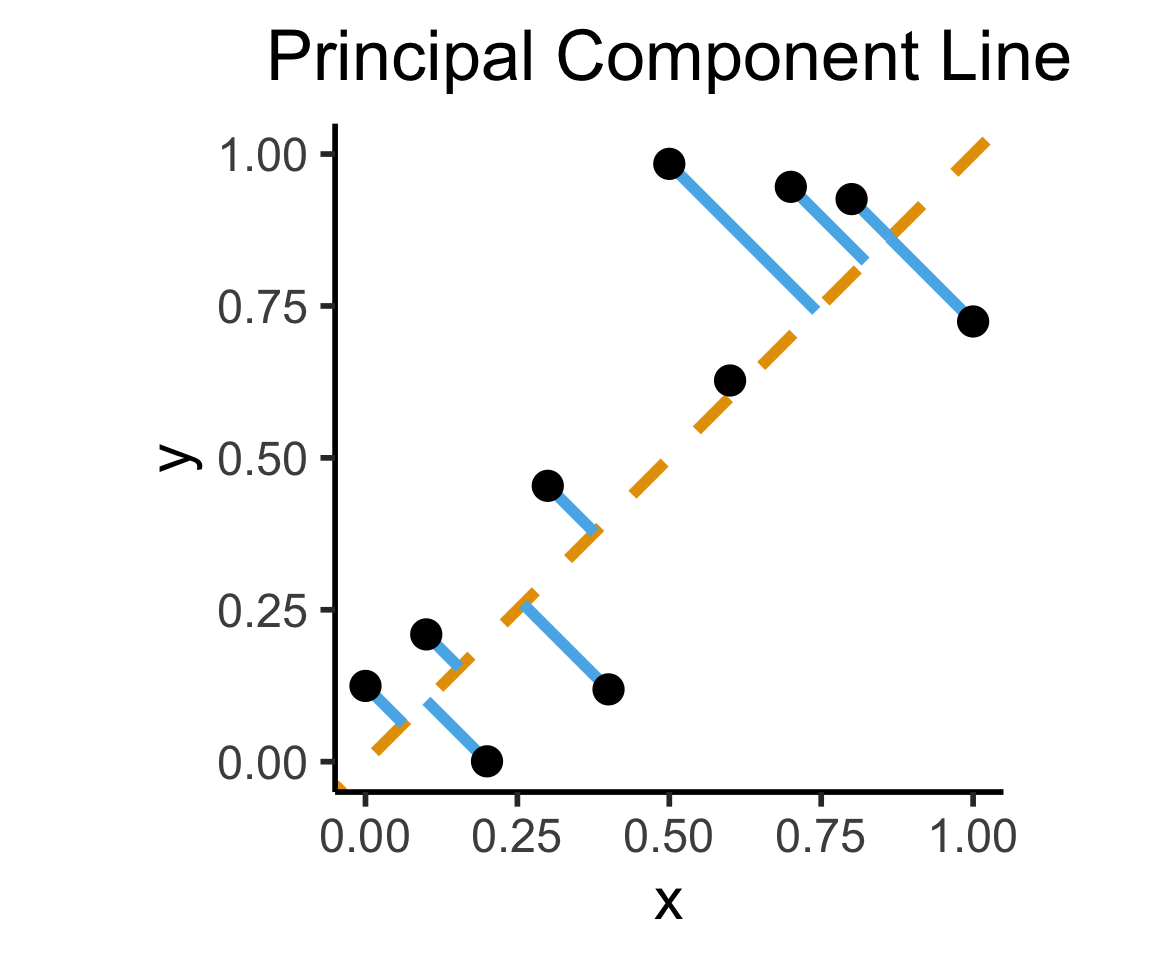

Final reminder that Regression, PCA have different goals!

If your goal was to, e.g., generate realistic \((x,y)\) pairs, then (mathematically) you want PCA! Roughly:

\[ \widehat{f}_{\text{PCA}} = \min_{\mathbf{c}}\left[ \sum_{i=1}^{n} (\widehat{x}_i(\mathbf{c}) - x_i)^2 + (\widehat{y}_i(\mathbf{c}) - y_i)^2 \right] \]

Our goal is a good predictor of \(Y\):

\[ \widehat{f}_{\text{Reg}} = \min_{\beta_0, \beta_1}\left[ \sum_{i=1}^{n} (\widehat{y}_i(\beta) - y_i)^2 \right] \]

library(tidyverse)

set.seed(5321)

N <- 11

x <- seq(from = 0, to = 1, by = 1 / (N - 1))

y <- x + rnorm(N, 0, 0.2)

mean_y <- mean(y)

spread <- y - mean_y

df <- tibble(x = x, y = y, spread = spread)

ggplot(df, aes(x=x, y=y)) +

geom_abline(slope=1, intercept=0, linetype="dashed", color=cbPalette[1], linewidth=g_linewidth*2) +

geom_segment(xend=(x+y)/2, yend=(x+y)/2, linewidth=g_linewidth*2, color=cbPalette[2]) +

geom_point(size=g_pointsize) +

coord_equal() +

xlim(0, 1) + ylim(0, 1) +

dsan_theme("half") +

labs(

title = "Principal Component Line"

)

ggplot(df, aes(x=x, y=y)) +

geom_abline(slope=1, intercept=0, linetype="dashed", color=cbPalette[1], linewidth=g_linewidth*2) +

geom_segment(xend=x, yend=x, linewidth=g_linewidth*2, color=cbPalette[2]) +

geom_point(size=g_pointsize) +

coord_equal() +

xlim(0, 1) + ylim(0, 1) +

dsan_theme("half") +

labs(

title = "Regression Line"

)── Attaching core tidyverse packages ──────────────────────── tidyverse 2.0.0 ──

✔ dplyr 1.2.1 ✔ readr 2.2.0

✔ forcats 1.0.1 ✔ stringr 1.6.0

✔ lubridate 1.9.5 ✔ tibble 3.3.1

✔ purrr 1.2.1 ✔ tidyr 1.3.2

── Conflicts ────────────────────────────────────────── tidyverse_conflicts() ──

✖ dplyr::filter() masks stats::filter()

✖ dplyr::lag() masks stats::lag()

ℹ Use the conflicted package (<http://conflicted.r-lib.org/>) to force all conflicts to become errorsWarning: Removed 1 row containing missing values or values outside the scale range

(`geom_segment()`).Warning: Removed 1 row containing missing values or values outside the scale range

(`geom_point()`).

Warning: Removed 1 row containing missing values or values outside the scale range

(`geom_segment()`).Warning: Removed 1 row containing missing values or values outside the scale range

(`geom_point()`).

On the difference between these two lines, and why it matters, I cannot recommend Gelman and Hill (2007) enough!

\[ Y = \beta_1 X + \varepsilon \]

library(latex2exp)

set.seed(5300)

# rand_slope <- log(runif(80, min=0, max=1))

# rand_slope[41:80] <- -rand_slope[41:80]

# rand_lines <- tibble::tibble(

# id=1:80, slope=rand_slope, intercept=0

# )

# angles <- runif(100, -pi/2, pi/2)

angles <- seq(from=-pi/2, to=pi/2, length.out=50)

possible_lines <- tibble::tibble(

slope=tan(angles), intercept=0

)

num_points <- 30

x_vals <- runif(num_points, 0, 1)

y0_vals <- 0.5 * x_vals + 0.25

y_noise <- rnorm(num_points, 0, 0.07)

y_vals <- y0_vals + y_noise

rand_df <- tibble::tibble(x=x_vals, y=y_vals)

title_exp <- TeX("Parameter Space ($\\beta_1$)")

# Main plot object

gen_lines_plot <- function(point_size=2.5) {

lines_plot <- rand_df |> ggplot(aes(x=x, y=y)) +

geom_point(size=point_size) +

geom_hline(yintercept=0, linewidth=1.5) +

geom_vline(xintercept=0, linewidth=1.5) +

# Point at origin

geom_point(data=data.frame(x=0, y=0), aes(x=x, y=y), size=4) +

xlim(-1,1) +

ylim(-1,1) +

# coord_fixed() +

theme_dsan_min(base_size=28)

return(lines_plot)

}

main_lines_plot <- gen_lines_plot()

main_lines_plot +

# Parameter space of possible lines

geom_abline(

data=possible_lines,

aes(slope=slope, intercept=intercept, color='possible'),

# linetype="dotted",

# linewidth=0.75,

alpha=0.25

) +

# True DGP

geom_abline(

aes(

slope=0.5,

intercept=0.25,

color='true'

), linewidth=1, alpha=0.8

) +

scale_color_manual(

element_blank(),

values=c('possible'="black", 'true'=cb_palette[2]),

labels=c('possible'="Possible Fits", 'true'="True DGP")

) +

remove_legend_title() +

labs(

title=title_exp

)

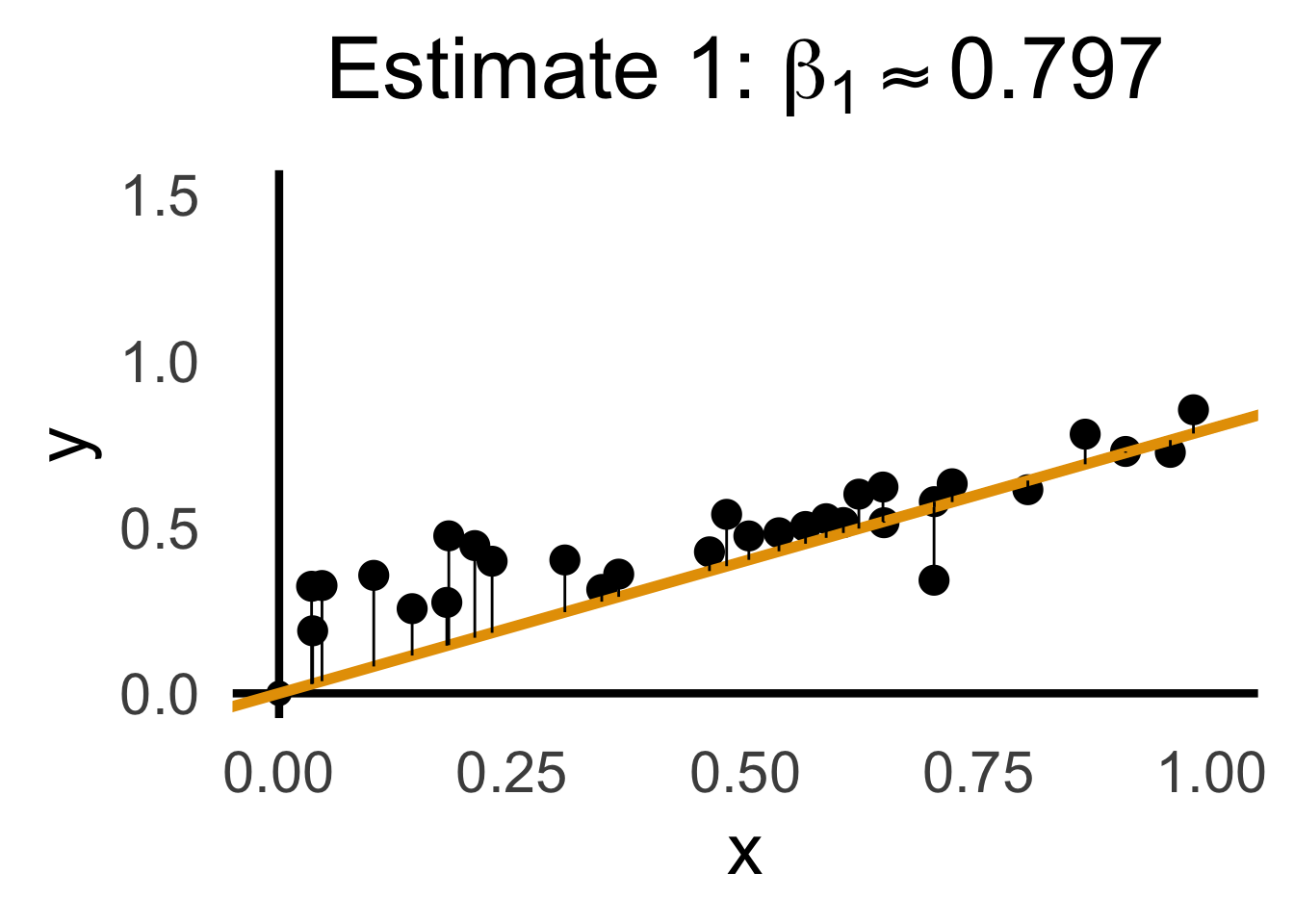

rc1_df <- possible_lines |> slice(n() - 14)

# Predictions for this choice

rc1_pred_df <- rand_df |> mutate(

y_pred = rc1_df$slope * x,

resid = y - y_pred

)

rc1_label <- TeX(paste0("Estimate 1: $\\beta_1 \\approx ",round(rc1_df$slope, 3),"$"))

rc1_lines_plot <- gen_lines_plot(point_size=5)

rc1_lines_plot +

geom_abline(

data=rc1_df,

aes(intercept=intercept, slope=slope),

linewidth=2,

color=cb_palette[1]

) +

geom_segment(

data=rc1_pred_df,

aes(x=x, y=y, xend=x, yend=y_pred),

# color=cb_palette[1]

) +

xlim(0, 1) + ylim(0, 1.5) +

labs(

title = rc1_label

)

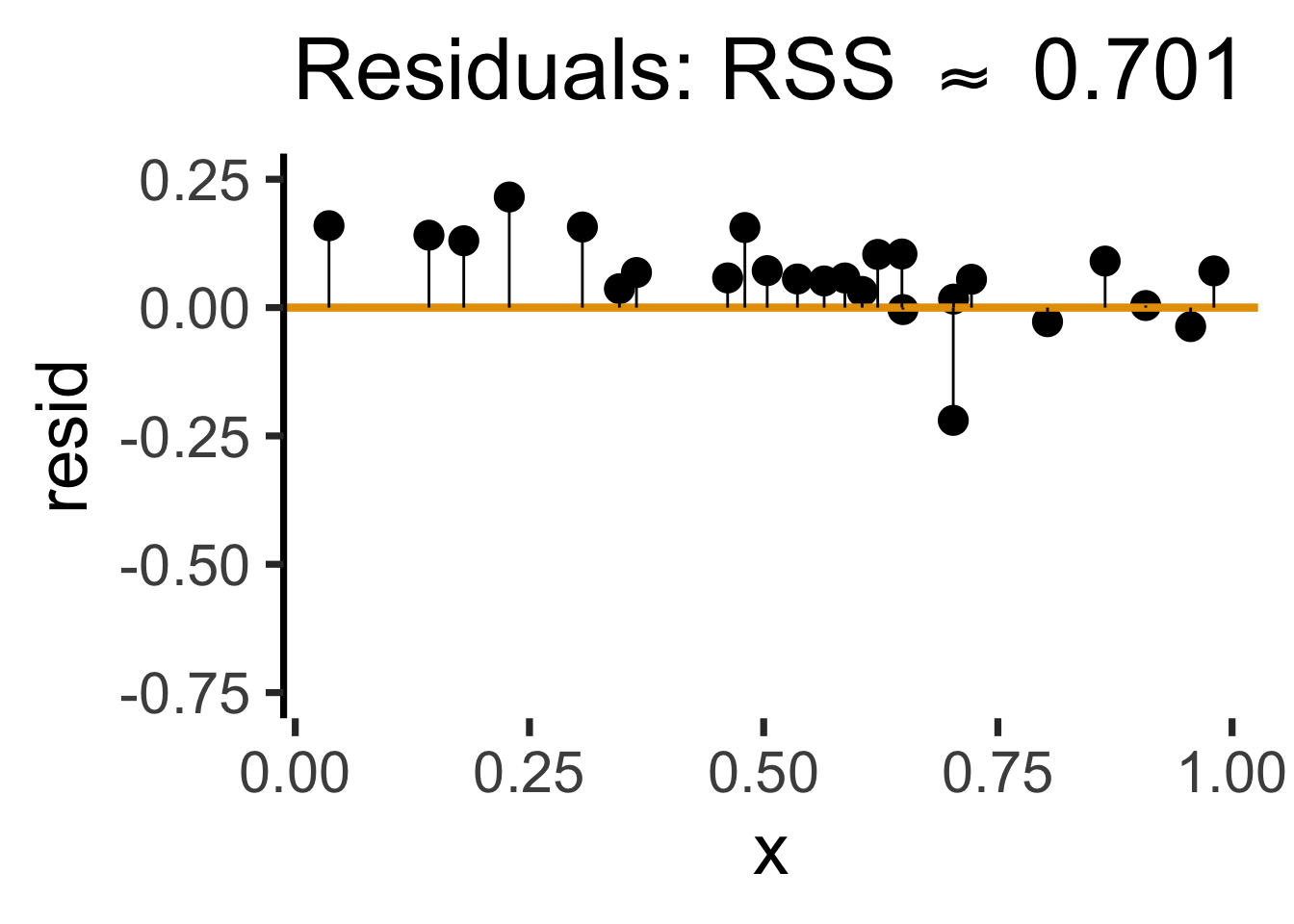

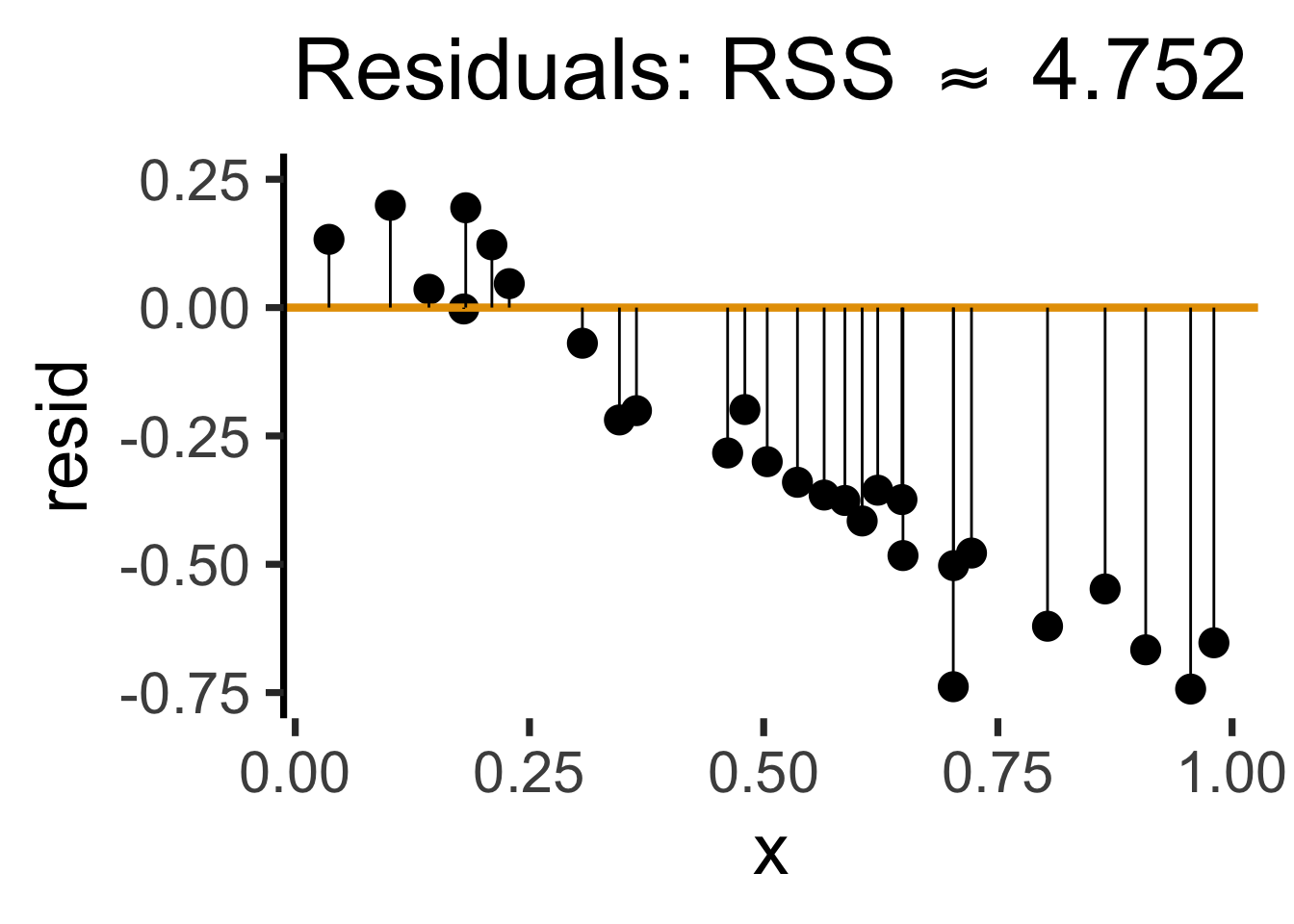

gen_resid_plot <- function(pred_df) {

rc_rss <- sum((pred_df$resid)^2)

rc_resid_label <- TeX(paste0("Residuals: RSS $\\approx$ ",round(rc_rss,3)))

rc_resid_plot <- pred_df |> ggplot(aes(x=x, y=resid)) +

geom_point(size=5) +

geom_hline(

yintercept=0,

color=cb_palette[1],

linewidth=1.5

) +

geom_segment(

aes(xend=x, yend=0)

) +

theme_dsan(base_size=28) +

theme(axis.line.x = element_blank()) +

ylim(-0.75, 0.25) +

labs(

title=rc_resid_label

)

return(rc_resid_plot)

}

rc1_resid_plot <- gen_resid_plot(rc1_pred_df)

rc1_resid_plot

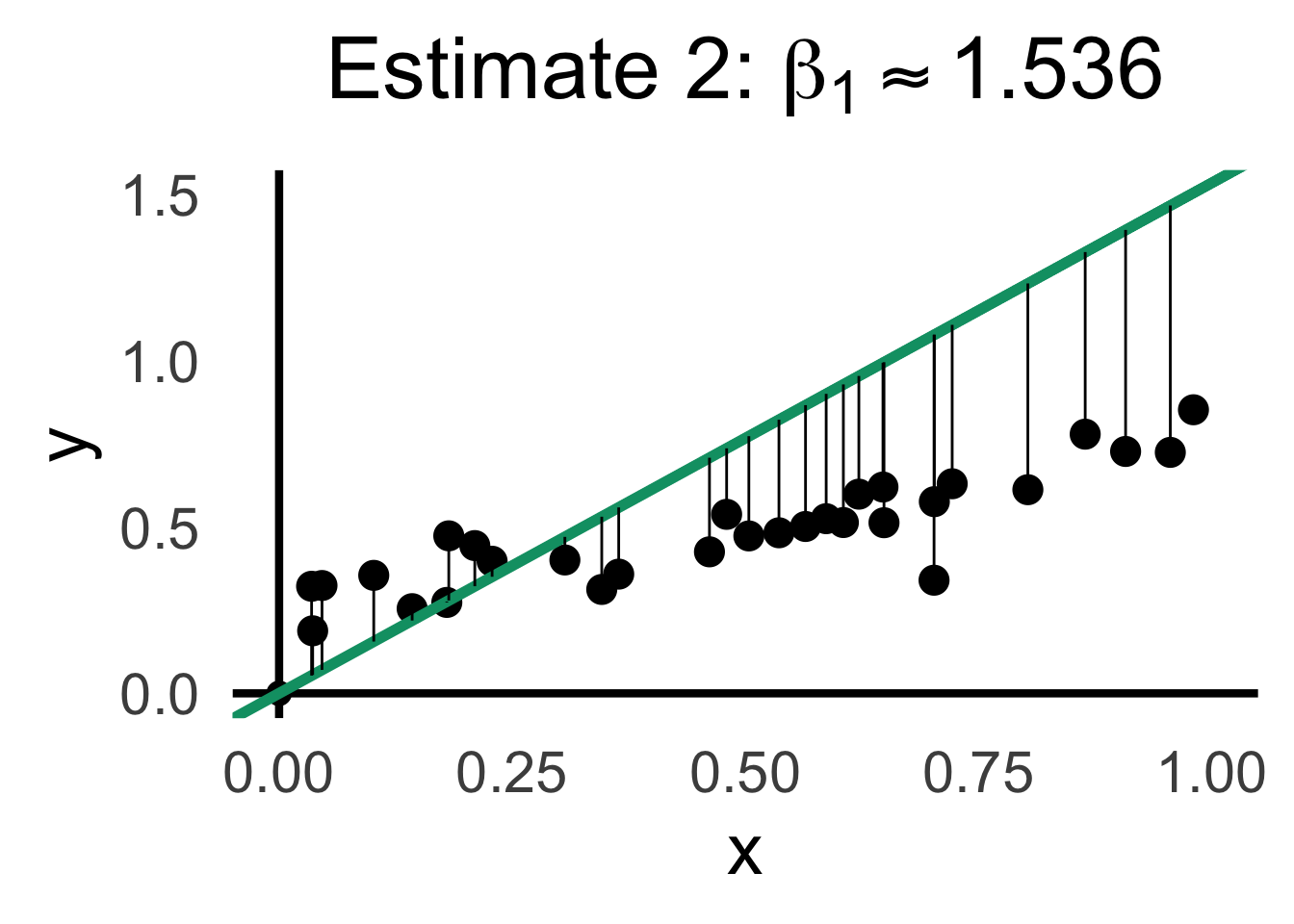

rc2_df <- possible_lines |> slice(n() - 9)

# Predictions for this choice

rc2_pred_df <- rand_df |> mutate(

y_pred = rc2_df$slope * x,

resid = y - y_pred

)

rc2_label <- TeX(paste0("Estimate 2: $\\beta_1 \\approx ",round(rc2_df$slope,3),"$"))

rc2_lines_plot <- gen_lines_plot(point_size=5)

rc2_lines_plot +

geom_abline(

data=rc2_df,

aes(intercept=intercept, slope=slope),

linewidth=2,

color=cb_palette[3]

) +

geom_segment(

data=rc2_pred_df,

aes(

x=x, y=y, xend=x,

# yend=ifelse(y_pred <= 1, y_pred, Inf)

yend=y_pred

)

# color=cb_palette[1]

) +

xlim(0, 1) + ylim(0, 1.5) +

labs(

title=rc2_label

)

rc2_resid_plot <- gen_resid_plot(rc2_pred_df)

rc2_resid_plotWarning: Removed 2 rows containing missing values or values outside the scale range

(`geom_point()`).Warning: Removed 2 rows containing missing values or values outside the scale range

(`geom_segment()`).

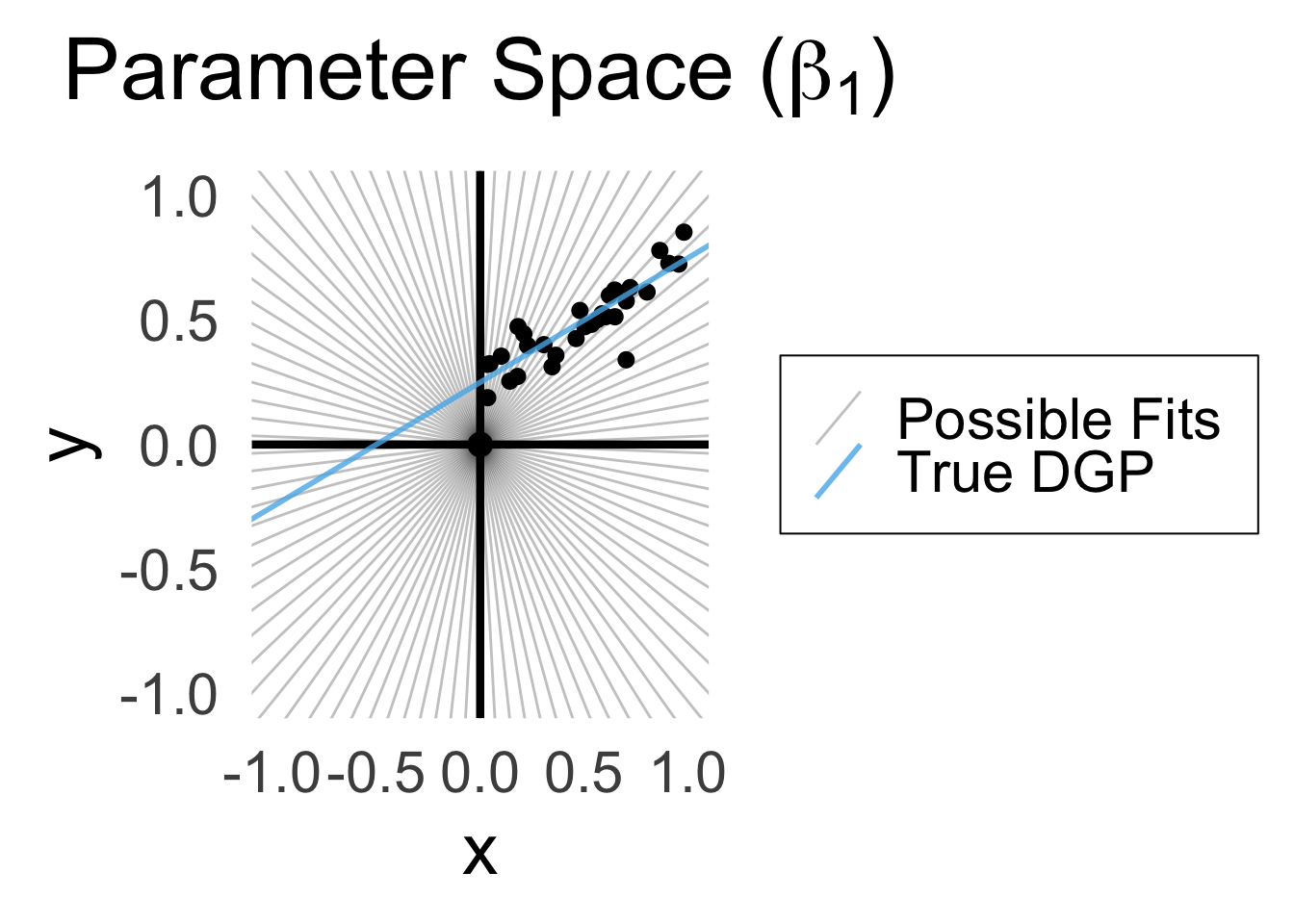

\[ \begin{align*} \beta_1^* = \overbrace{\argmin}^{\begin{array}{c} \text{\small{Find thing}} \\[-5mm] \text{\small{that minimizes}}\end{array}}_{\beta_1}\left[ \sum_{i=1}^{n}(y_i - \widehat{y}_i)^2 \right] = \argmin_{\beta_1}\left[ \sum_{i=1}^{n}(y_i - \beta_1x_i)^2 \right] \end{align*} \]

We can compute this derivative to obtain:

\[ \frac{\partial}{\partial\beta_1}\left[ \sum_{i=1}^{n}(\beta_1x_i - y_i)^2 \right] = \sum_{i=1}^{n}\frac{\partial}{\partial\beta_1}(\beta_1x_i - y_i)^2 = \sum_{i=1}^{n}2(\beta_1x_i - y_i)x_i \]

And our first-order condition means that:

\[ \sum_{i=1}^{n}2(\beta_1^*x_i - y_i)x_i = 0 \iff \beta_1^*\sum_{i=1}^{n}x_i^2 = \sum_{i=1}^{n}x_iy_i \iff \boxed{\beta_1^* = \frac{\sum_{i=1}^{n}x_iy_i}{\sum_{i=1}^{n}x_i^2}} \]

R vs. statsmodelslm()

ad_df <- read_csv('assets/Advertising.csv')New names:

Rows: 200 Columns: 5

── Column specification

──────────────────────────────────────────────────────── Delimiter: "," dbl

(5): ...1, TV, radio, newspaper, sales

ℹ Use `spec()` to retrieve the full column specification for this data. ℹ

Specify the column types or set `show_col_types = FALSE` to quiet this message.

• `` -> `...1`lin_model <- lm(sales ~ TV, data=ad_df)

summary(lin_model)

Call:

lm(formula = sales ~ TV, data = ad_df)

Residuals:

Min 1Q Median 3Q Max

-8.3860 -1.9545 -0.1913 2.0671 7.2124

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 7.032594 0.457843 15.36 <2e-16 ***

TV 0.047537 0.002691 17.67 <2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 3.259 on 198 degrees of freedom

Multiple R-squared: 0.6119, Adjusted R-squared: 0.6099

F-statistic: 312.1 on 1 and 198 DF, p-value: < 2.2e-16General syntax:

lm(

dependent ~ independent + controls,

data = my_df

)smf.ols()

import statsmodels.formula.api as smf

results = smf.ols("sales ~ TV", data=ad_df).fit()

print(results.summary(slim=True)) OLS Regression Results

==============================================================================

Dep. Variable: sales R-squared: 0.612

Model: OLS Adj. R-squared: 0.610

No. Observations: 200 F-statistic: 312.1

Covariance Type: nonrobust Prob (F-statistic): 1.47e-42

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept 7.0326 0.458 15.360 0.000 6.130 7.935

TV 0.0475 0.003 17.668 0.000 0.042 0.053

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.General syntax:

smf.ols(

"dependent ~ independent + controls",

data = my_df

)library(tidyverse)

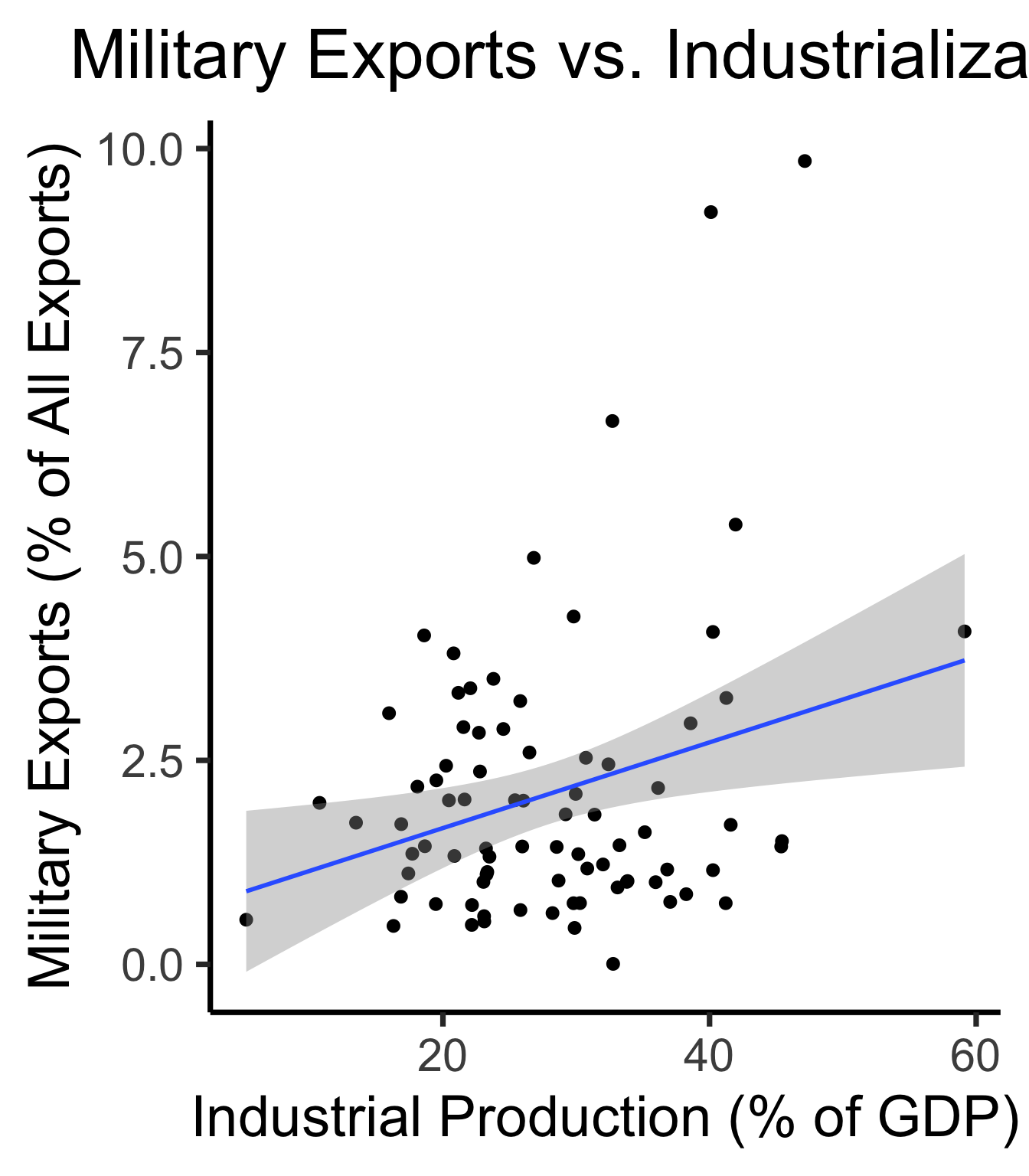

gdp_df <- read_csv("assets/gdp_pca.csv")

mil_plot <- gdp_df |> ggplot(aes(x=industrial, y=military)) +

geom_point(size=0.5*g_pointsize) +

geom_smooth(method='lm', formula="y ~ x", linewidth=1) +

theme_dsan() +

labs(

title="Military Exports vs. Industrialization",

x="Industrial Production (% of GDP)",

y="Military Exports (% of All Exports)"

)mil_plot + theme_dsan("quarter")

gdp_model <- lm(military ~ industrial, data=gdp_df)

summary(gdp_model)

Call:

lm(formula = military ~ industrial, data = gdp_df)

Residuals:

Min 1Q Median 3Q Max

-2.3354 -1.0997 -0.3870 0.6081 6.7508

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.61969 0.59526 1.041 0.3010

industrial 0.05253 0.02019 2.602 0.0111 *

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 1.671 on 79 degrees of freedom

(8 observations deleted due to missingness)

Multiple R-squared: 0.07895, Adjusted R-squared: 0.06729

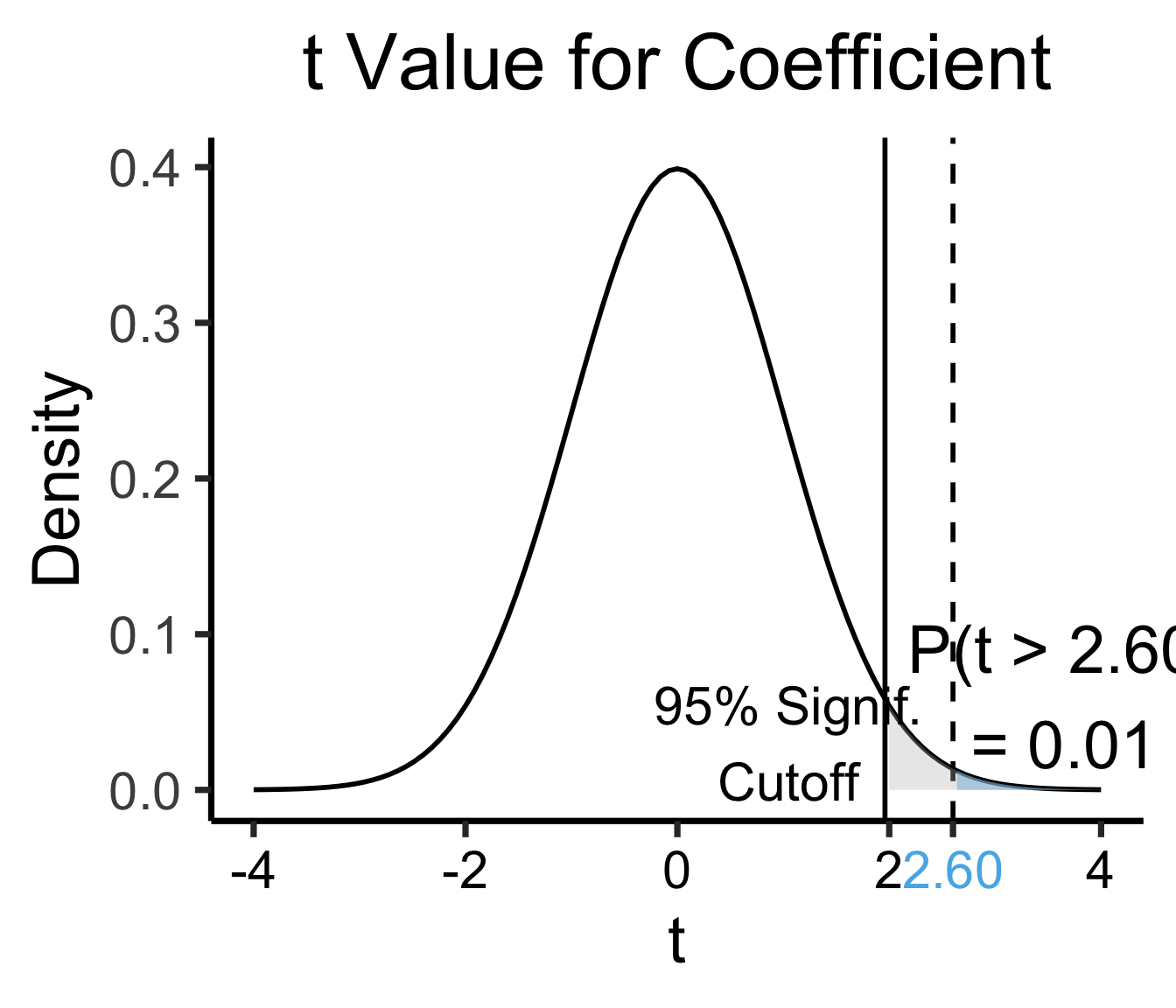

F-statistic: 6.771 on 1 and 79 DF, p-value: 0.01106| Estimate | Std. Error | t value | Pr(>|t|) | ||

|---|---|---|---|---|---|

| (Intercept) | 0.61969 | 0.59526 | 1.041 | 0.3010 | |

| industrial | 0.05253 | 0.02019 | 2.602 | 0.0111 | * |

| \(\widehat{\beta}\) | Uncertainty | Test stat \(t\) | How extreme is \(t\)? | Signif. Level |

\[ \widehat{y} \approx \class{cb1}{\overset{\beta_0}{\underset{\small \pm 0.595}{0.620}}} + \class{cb2}{\overset{\beta_1}{\underset{\small \pm 0.020}{0.053}}} \cdot x \]

| Estimate | Std. Error | t value | Pr(>|t|) | ||

|---|---|---|---|---|---|

| (Intercept) | 0.61969 | 0.59526 | 1.041 | 0.3010 | |

| industrial | 0.05253 | 0.02019 | 2.602 | 0.0111 | * |

| \(\widehat{\beta}\) | Uncertainty | Test stat \(t\) | How extreme is \(t\)? | Signif. Level |

library(ggplot2)

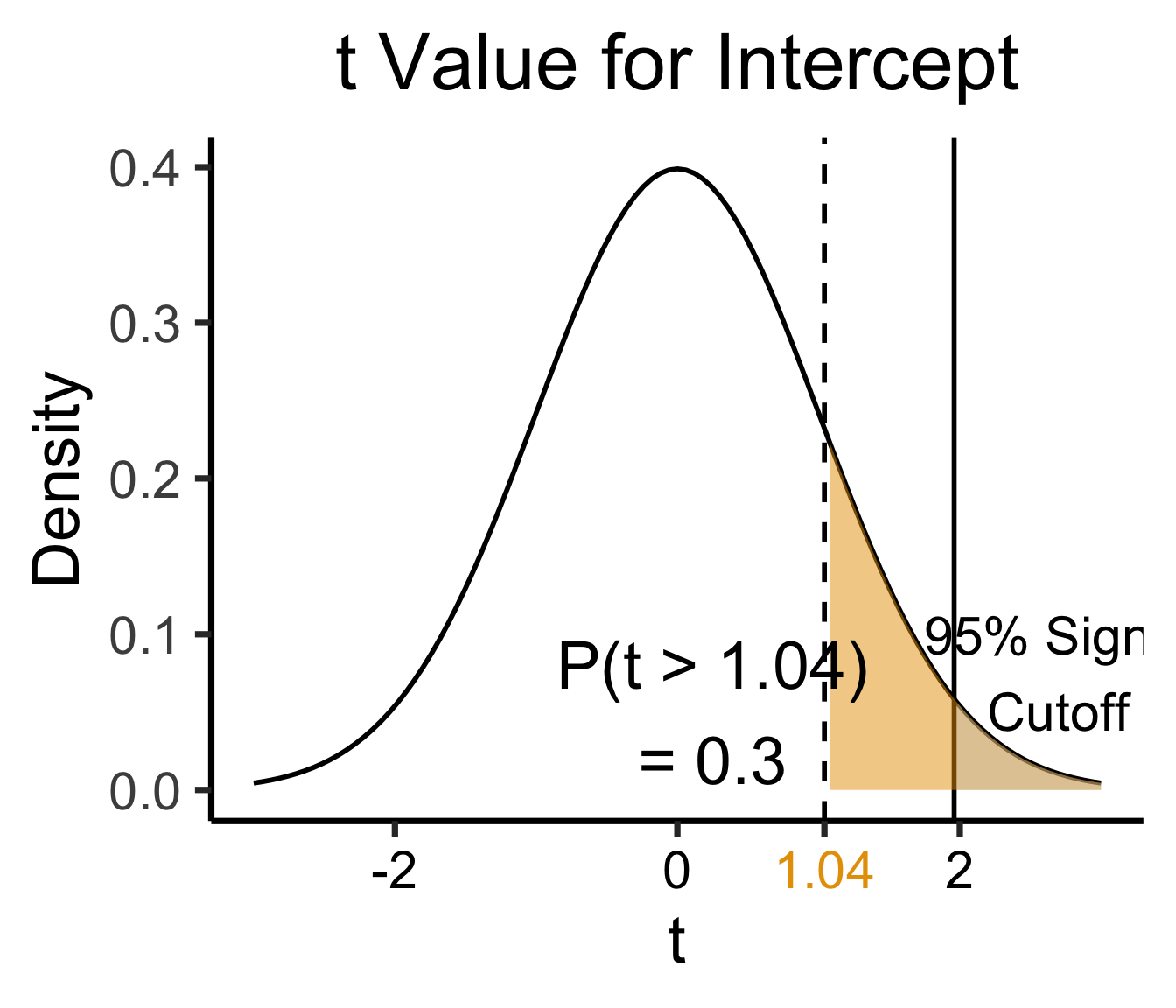

int_tstat <- 1.041

int_tstat_str <- sprintf("%.02f", int_tstat)

label_df_int <- tribble(

~x, ~y, ~label,

0.25, 0.05, paste0("P(t > ",int_tstat_str,")\n= 0.3")

)

label_df_signif_int <- tribble(

~x, ~y, ~label,

2.7, 0.075, "95% Signif.\nCutoff"

)

funcShaded <- function(x, lower_bound, upper_bound){

y <- dnorm(x)

y[x < lower_bound | x > upper_bound] <- NA

return(y)

}

funcShadedIntercept <- function(x) funcShaded(x, int_tstat, Inf)

funcShadedSignif <- function(x) funcShaded(x, 1.96, Inf)

ggplot(data=data.frame(x=c(-3,3)), aes(x=x)) +

stat_function(fun=dnorm, linewidth=g_linewidth) +

geom_vline(aes(xintercept=int_tstat), linewidth=g_linewidth, linetype="dashed") +

geom_vline(aes(xintercept = 1.96), linewidth=g_linewidth, linetype="solid") +

stat_function(fun = funcShadedIntercept, geom = "area", fill = cbPalette[1], alpha = 0.5) +

stat_function(fun = funcShadedSignif, geom = "area", fill = "grey", alpha = 0.333) +

geom_text(label_df_int, mapping = aes(x = x, y = y, label = label), size = 10) +

geom_text(label_df_signif_int, mapping = aes(x = x, y = y, label = label), size = 8) +

# Add single additional tick

scale_x_continuous(breaks=c(-2, 0, int_tstat, 2), labels=c("-2","0",int_tstat_str,"2")) +

dsan_theme("quarter") +

labs(

title = "t Value for Intercept",

x = "t",

y = "Density"

) +

theme(axis.text.x = element_text(colour = c("black", "black", cbPalette[1], "black")))

library(ggplot2)

coef_tstat <- 2.602

coef_tstat_str <- sprintf("%.02f", coef_tstat)

label_df_coef <- tribble(

~x, ~y, ~label,

3.65, 0.06, paste0("P(t > ",coef_tstat_str,")\n= 0.01")

)

label_df_signif_coef <- tribble(

~x, ~y, ~label,

1.05, 0.03, "95% Signif.\nCutoff"

)

funcShadedCoef <- function(x) funcShaded(x, coef_tstat, Inf)

ggplot(data=data.frame(x=c(-4,4)), aes(x=x)) +

stat_function(fun=dnorm, linewidth=g_linewidth) +

geom_vline(aes(xintercept=coef_tstat), linetype="dashed", linewidth=g_linewidth) +

geom_vline(aes(xintercept=1.96), linetype="solid", linewidth=g_linewidth) +

stat_function(fun = funcShadedCoef, geom = "area", fill = cbPalette[2], alpha = 0.5) +

stat_function(fun = funcShadedSignif, geom = "area", fill = "grey", alpha = 0.333) +

# Label shaded area

geom_text(label_df_coef, mapping = aes(x = x, y = y, label = label), size = 10) +

# Label significance cutoff

geom_text(label_df_signif_coef, mapping = aes(x = x, y = y, label = label), size = 8) +

coord_cartesian(clip = "off") +

# Add single additional tick

scale_x_continuous(breaks=c(-4, -2, 0, 2, coef_tstat, 4), labels=c("-4", "-2","0", "2", coef_tstat_str,"4")) +

dsan_theme("quarter") +

labs(

title = "t Value for Coefficient",

x = "t",

y = "Density"

) +

theme(axis.text.x = element_text(colour = c("black", "black", "black", "black", cbPalette[2], "black")))

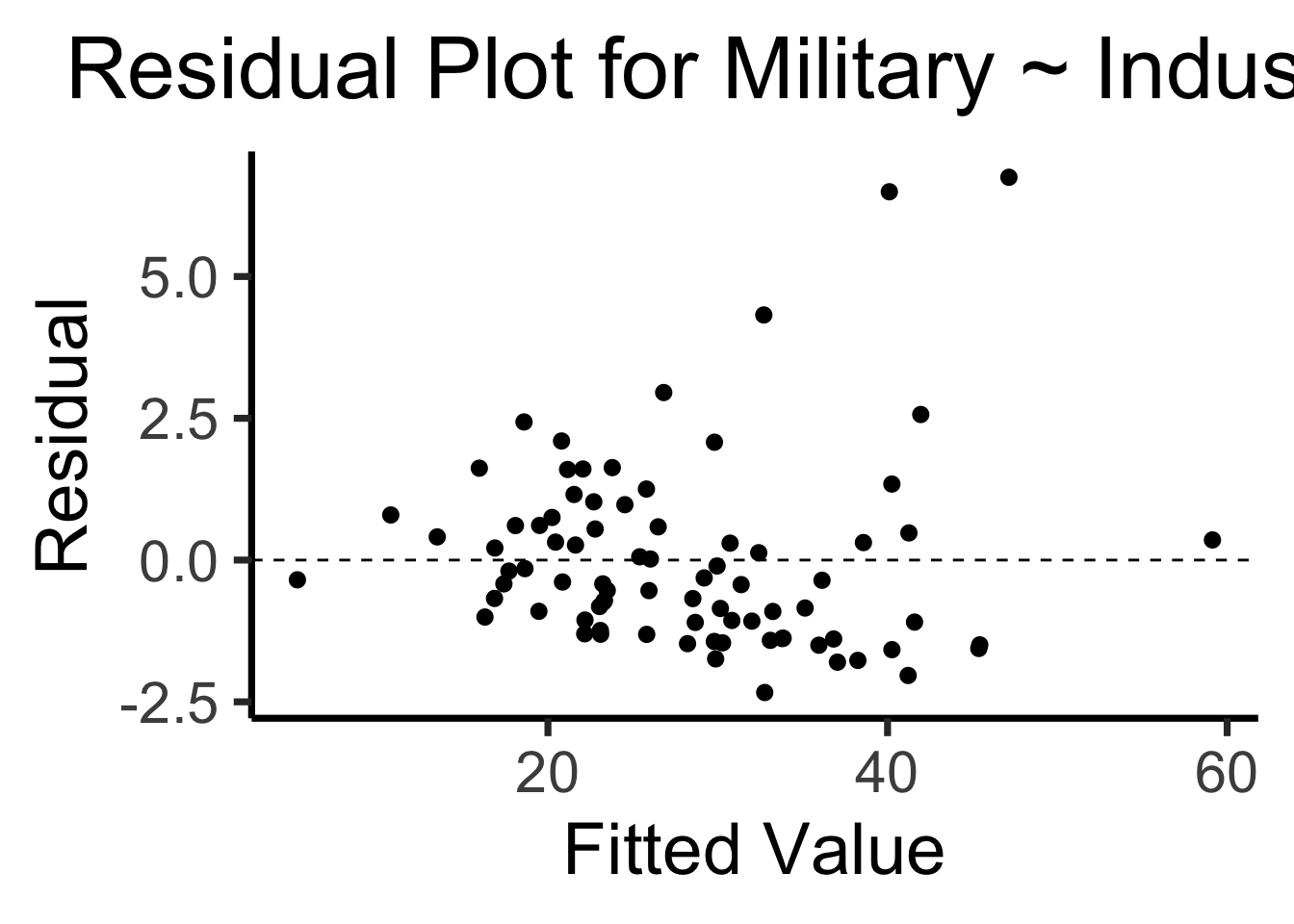

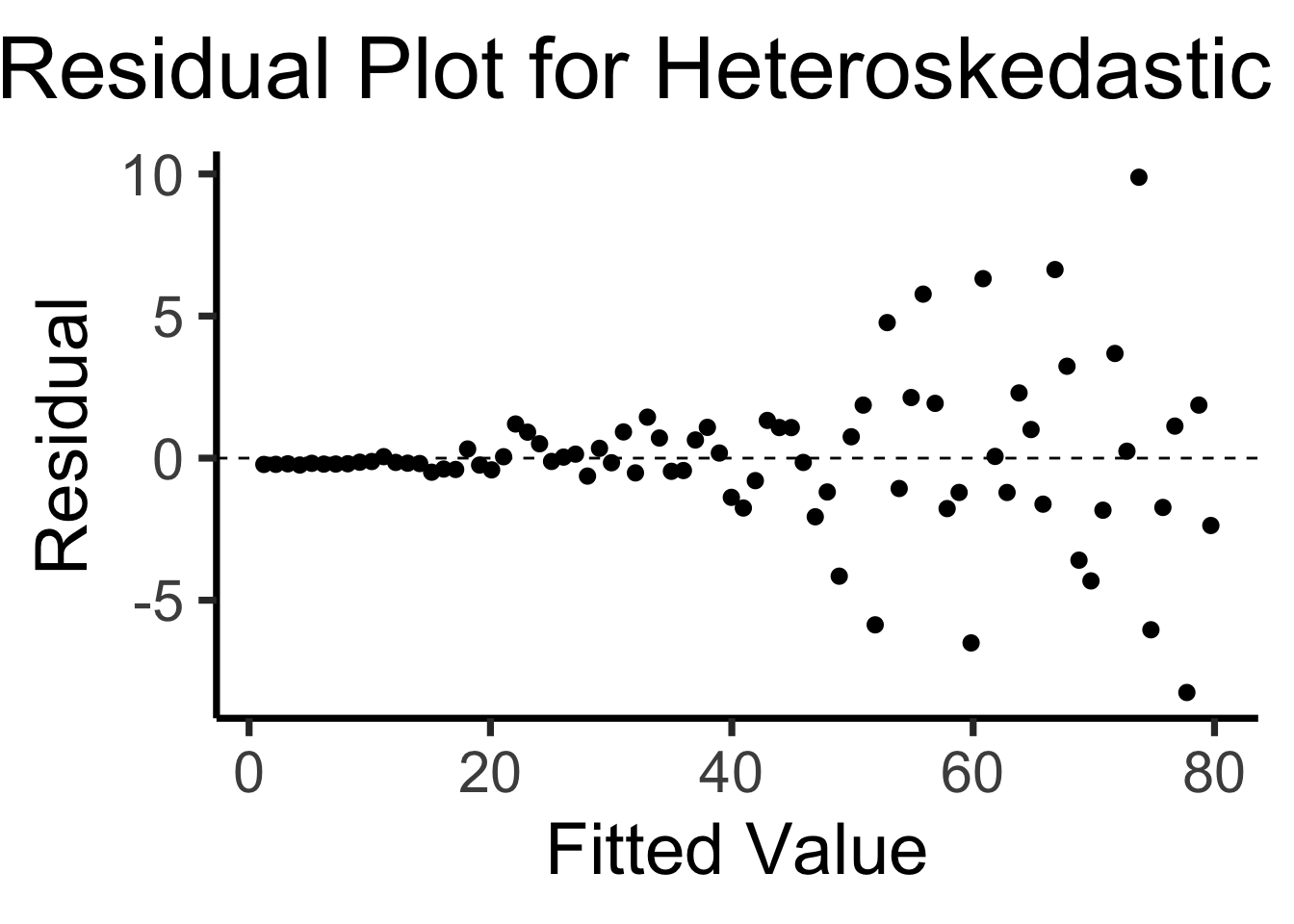

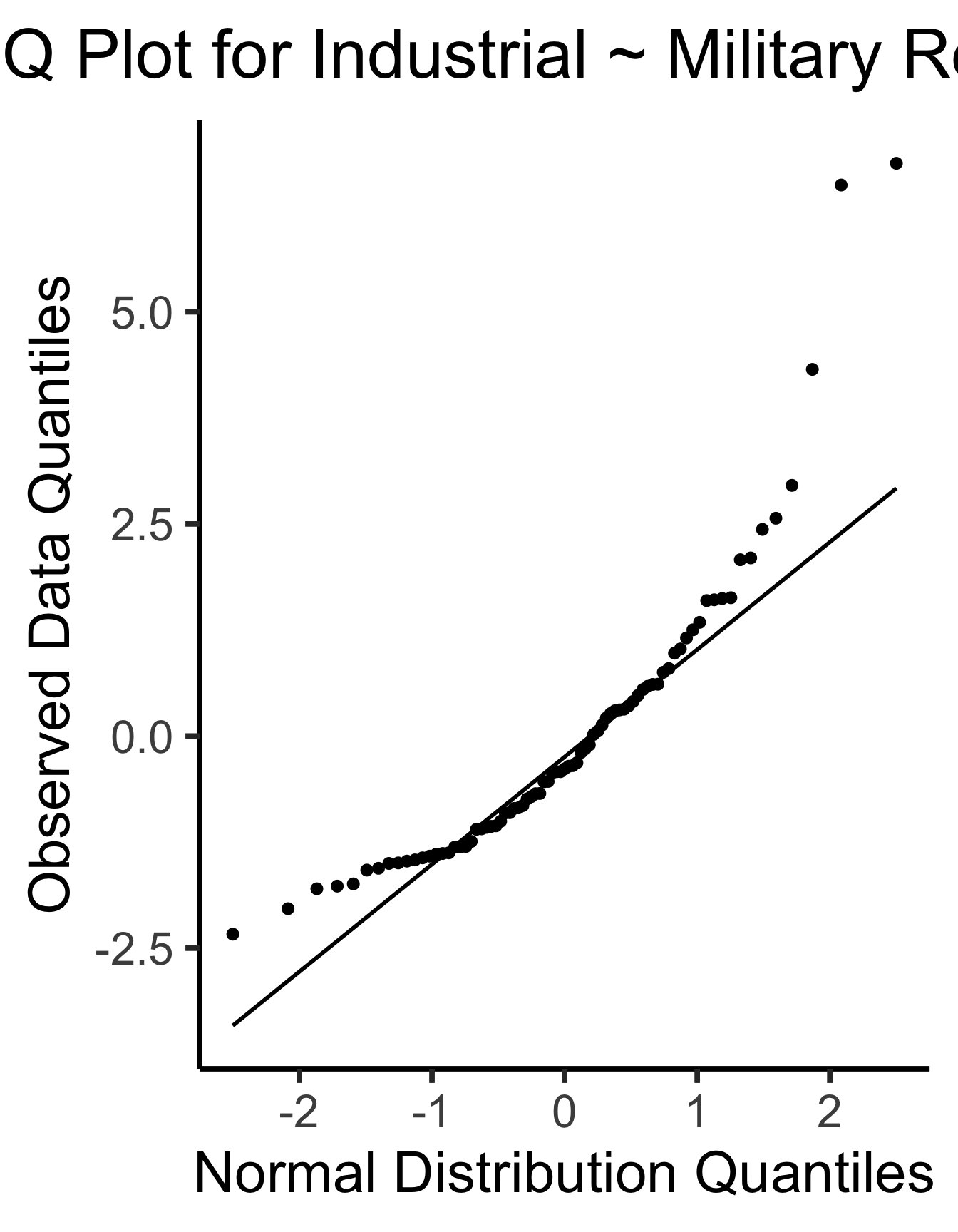

Recall homoskedasticity assumption: Given our model

\[ y_i = \beta_0 + \beta_1x_i + \varepsilon_i \]

the errors \(\varepsilon_i\) should not vary systematically with \(i\)

Formally: \(\forall i \left[ \Var{\varepsilon_i} = \sigma^2 \right]\)

library(broom)

gdp_resid_df <- augment(gdp_model)

ggplot(gdp_resid_df, aes(x = industrial, y = .resid)) +

geom_point(size = g_pointsize/2) +

geom_hline(yintercept=0, linetype="dashed") +

dsan_theme("quarter") +

labs(

title = "Residual Plot for Military ~ Industrial",

x = "Fitted Value",

y = "Residual"

)

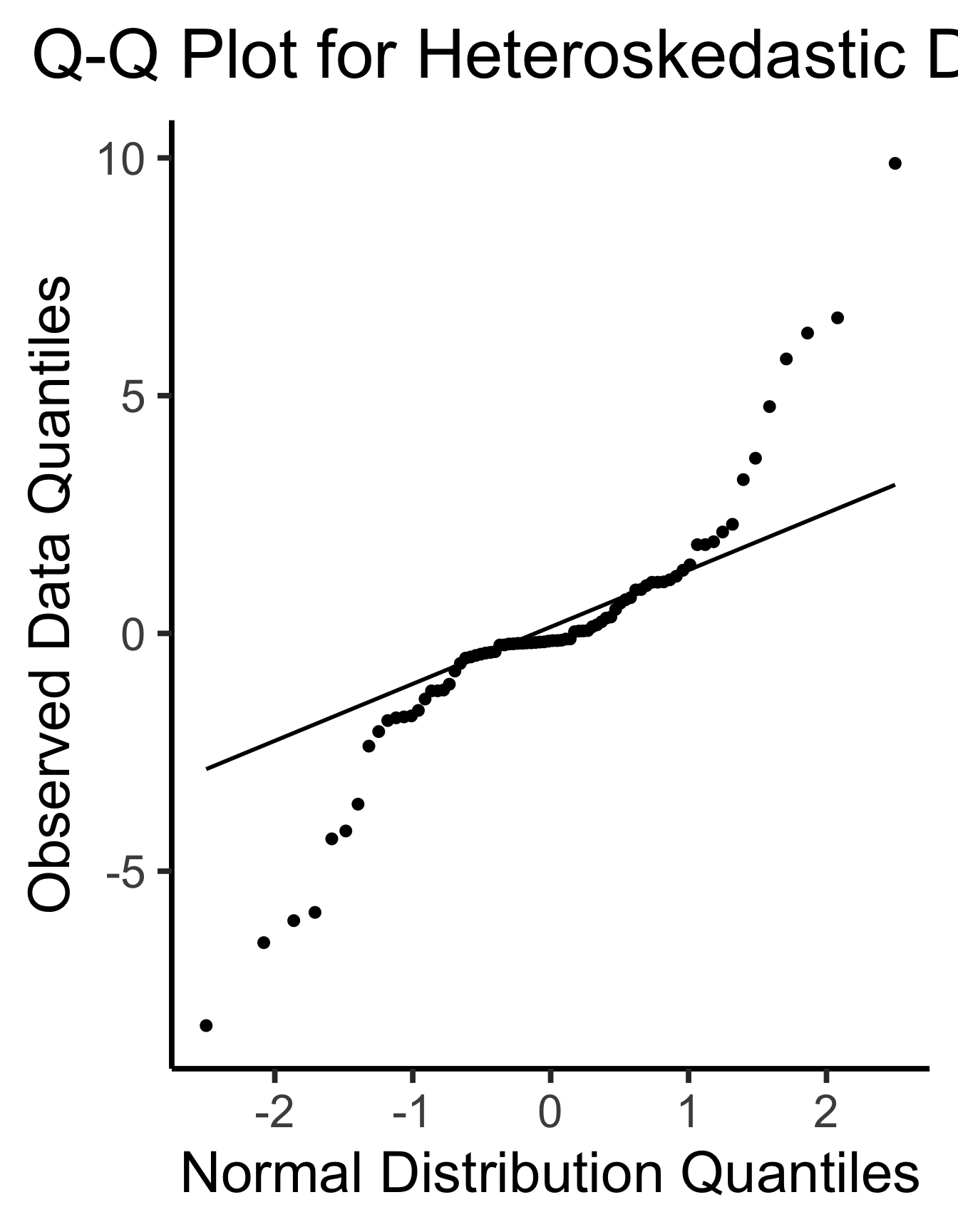

x <- 1:80

errors <- rnorm(length(x), 0, x^2/1000)

y <- x + errors

het_model <- lm(y ~ x)

df_het <- augment(het_model)

ggplot(df_het, aes(x = .fitted, y = .resid)) +

geom_point(size = g_pointsize / 2) +

geom_hline(yintercept = 0, linetype = "dashed") +

dsan_theme("quarter") +

labs(

title = "Residual Plot for Heteroskedastic Data",

x = "Fitted Value",

y = "Residual"

)

ggplot(df_het, aes(sample=.resid)) +

stat_qq(size = g_pointsize/2) + stat_qq_line(linewidth = g_linewidth) +

dsan_theme(base_size=30) +

labs(

title = "Q-Q Plot for Heteroskedastic Data",

x = "Normal Distribution Quantiles",

y = "Observed Data Quantiles"

)

ggplot(gdp_resid_df, aes(sample=.resid)) +

stat_qq(size = g_pointsize/2) + stat_qq_line(linewidth = g_linewidth) +

dsan_theme(base_size=30) +

labs(

title = "Q-Q Plot for Industrial ~ Military Residuals",

x = "Normal Distribution Quantiles",

y = "Observed Data Quantiles"

)

\[ \widehat{y}_i = \beta_0 + \beta_1x_{i,1} + \beta_2x_{i,2} + \cdots + \beta_M x_{i,M} \]

library(extraDistr)

set.seed(5650)

n_c <- 300

cfork_df <- tibble(

Z = rbern(n_c),

X = rnorm(n_c, 2 * Z - 1),

Y = rnorm(n_c, 2 * Z - 1)

)

library(latex2exp)

overall_lm <- lm(Y ~ X, data=cfork_df)

overall_slope <- round(overall_lm$coef['X'], 3)

z0_lm <- lm(Y ~ X, data=cfork_df |> filter(Z == 0))

z0_slope <- round(z0_lm$coef['X'], 2)

z0_label <- paste0("$Slope_{Z=0} = ",z0_slope,"$")

z0_leg_label <- TeX(paste0("0 $(m=",z0_slope,")$"))

z1_lm <- lm(Y ~ X, data=cfork_df |> filter(Z == 1))

z1_slope <- round(z1_lm$coef['X'], 2)

z1_label <- paste0("$Slope_{Z=1} = ",z1_slope,"$")

z_texlabel <- TeX(paste0(z0_label, " | ", z1_label))

cfork_xmin <- min(cfork_df$X)

cfork_xmax <- max(cfork_df$X)

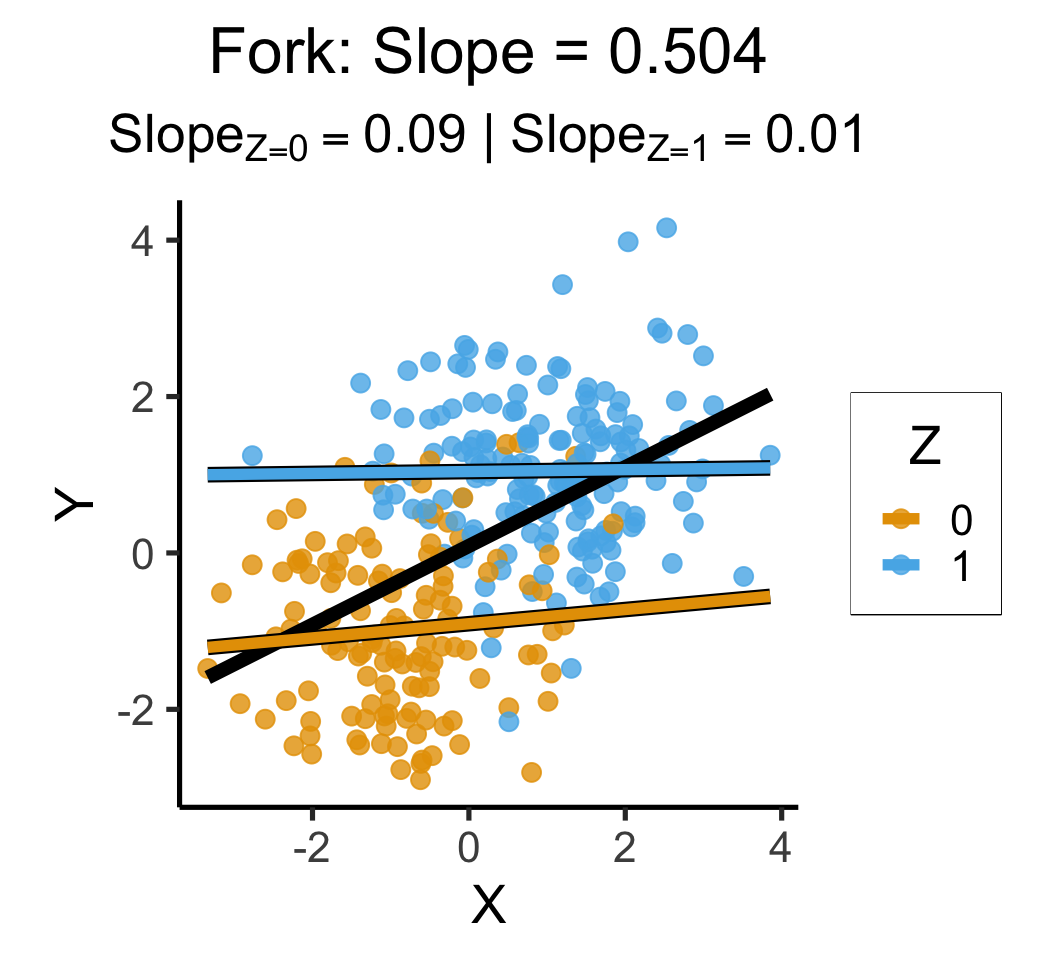

ggplot() +

# Points

geom_point(

data=cfork_df,

aes(x=X, y=Y, color=factor(Z)),

size=0.6*g_pointsize,

alpha=0.8

) +

# Overall lm

geom_smooth(

data=cfork_df, aes(x=X, y=Y),

method = lm, se = FALSE,

linewidth = 2.5, color='black'

) +

# Stratified lm

# (slightly larger black lines)

geom_smooth(

data=cfork_df,

aes(x=X, y=Y, group=factor(Z)),

method=lm, se=FALSE, fullrange=TRUE,

linewidth=2.75, color='black'

) +

# (Colored lines)

geom_smooth(

data=cfork_df,

aes(x=X, y=Y, color=factor(Z)),

method=lm, se=FALSE, fullrange=TRUE,

linewidth=2

) +

theme_dsan(base_size=20) +

theme(

plot.title = element_text(size=24),

plot.subtitle = element_text(size=20)

) +

coord_equal() +

labs(

title = paste0(

"Fork: Slope = ",overall_slope

),

subtitle=z_texlabel,

x = "X", y = "Y", color = "Z"

)

set.seed(5650)

cpipe_df <- tibble(

X = rnorm(n_c),

Z = rbern(n_c, plogis(X)),

Y = rnorm(n_c, 2 * Z - 1)

)

cpipe_lm <- lm(Y ~ X, data=cpipe_df)

cpipe_slope <- round(cpipe_lm$coef['X'], 3)

cpipe_z0_lm <- lm(Y ~ X, data=cpipe_df |> filter(Z == 0))

cpipe_z0_slope <- round(cpipe_z0_lm$coef['X'], 2)

cpipe_z0_label <- paste0("$Slope_{Z=0} = ",cpipe_z0_slope,"$")

cpipe_z1_lm <- lm(Y ~ X, data=cpipe_df |> filter(Z == 1))

cpipe_z1_slope <- round(cpipe_z1_lm$coef['X'], 2)

cpipe_z1_label <- paste0("$Slope_{Z=1} = ",cpipe_z1_slope,"$")

cpipe_z_texlabel <- TeX(paste0(cpipe_z0_label, " | ", cpipe_z1_label))

cpipe_xmin <- min(cpipe_df$X)

cpipe_xmax <- max(cpipe_df$X)

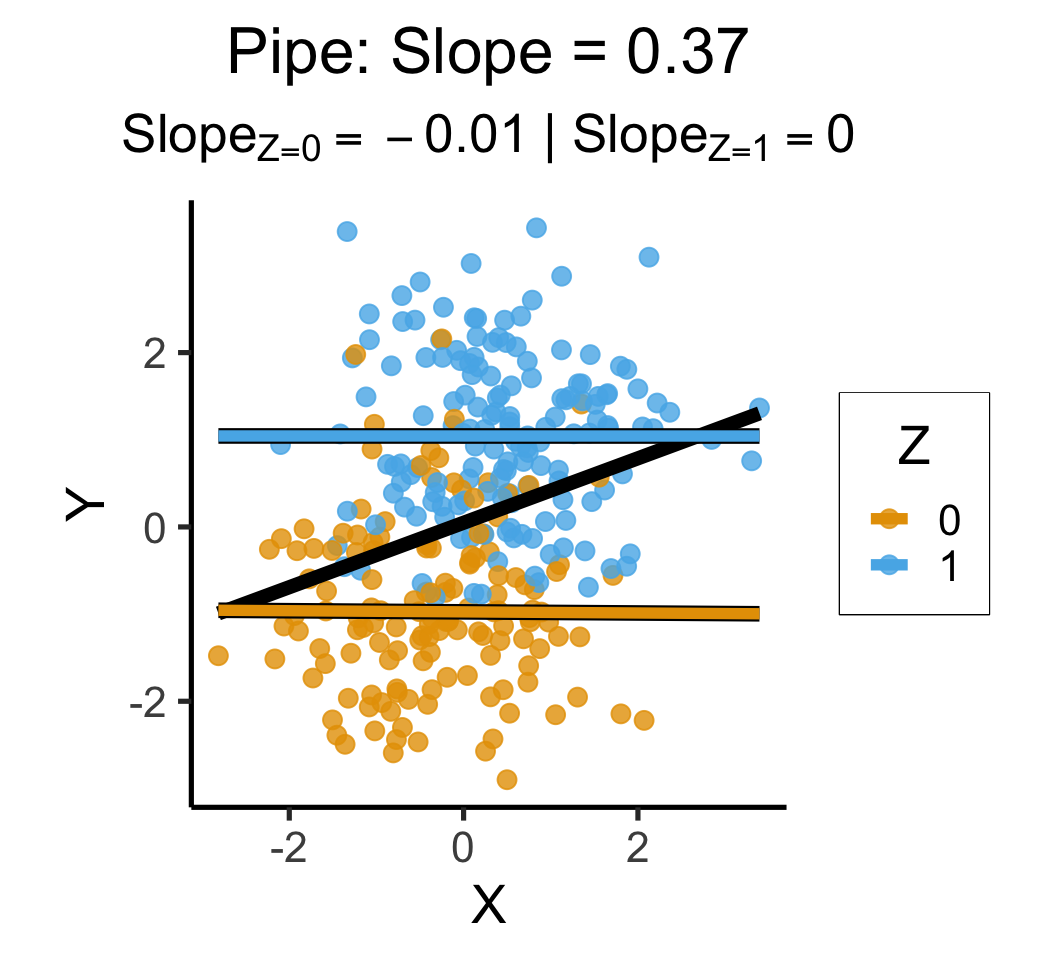

ggplot() +

# Points

geom_point(

data=cpipe_df |> filter(Y > -3),

aes(x=X, y=Y, color=factor(Z)),

size=0.6*g_pointsize,

alpha=0.8

) +

# Overall lm

geom_smooth(

data=cpipe_df, aes(x=X, y=Y),

method = lm, se = FALSE,

linewidth = 2.5, color='black'

) +

# Stratified lm

# (slightly larger black lines)

geom_smooth(

data=cpipe_df,

aes(x=X, y=Y, group=factor(Z)),

method=lm, se=FALSE, fullrange=TRUE,

linewidth=2.75, color='black'

) +

# (Colored lines)

geom_smooth(

data=cpipe_df,

aes(x=X, y=Y, color=factor(Z)),

method=lm, se=FALSE, fullrange=TRUE,

linewidth=2

) +

theme_dsan(base_size=20) +

theme(

plot.title = element_text(size=24),

plot.subtitle = element_text(size=20)

) +

coord_equal() +

labs(

title = paste0(

"Pipe: Slope = ",cpipe_slope

),

subtitle=cpipe_z_texlabel,

x = "X", y = "Y", color = "Z"

)

set.seed(5650)

ccoll_df <- tibble(

X = rnorm(n_c),

Y = rnorm(n_c),

Z = rbern(n_c, plogis(2 * (X + Y - 1)))

)

ccoll_lm <- lm(Y ~ X, data=ccoll_df)

ccoll_slope <- round(ccoll_lm$coef['X'], 3)

ccoll_z0_lm <- lm(Y ~ X, data=ccoll_df |> filter(Z == 0))

ccoll_z0_slope <- round(ccoll_z0_lm$coef['X'], 2)

ccoll_z0_label <- paste0("$Slope_{Z=0} = ",ccoll_z0_slope,"$")

ccoll_z1_lm <- lm(Y ~ X, data=ccoll_df |> filter(Z == 1))

ccoll_z1_slope <- round(ccoll_z1_lm$coef['X'], 2)

ccoll_z1_label <- paste0("$Slope_{Z=1} = ",ccoll_z1_slope,"$")

ccoll_z_texlabel <- TeX(paste0(ccoll_z0_label, " | ", ccoll_z1_label))

ccoll_xmin <- min(ccoll_df$X)

ccoll_xmax <- max(ccoll_df$X)

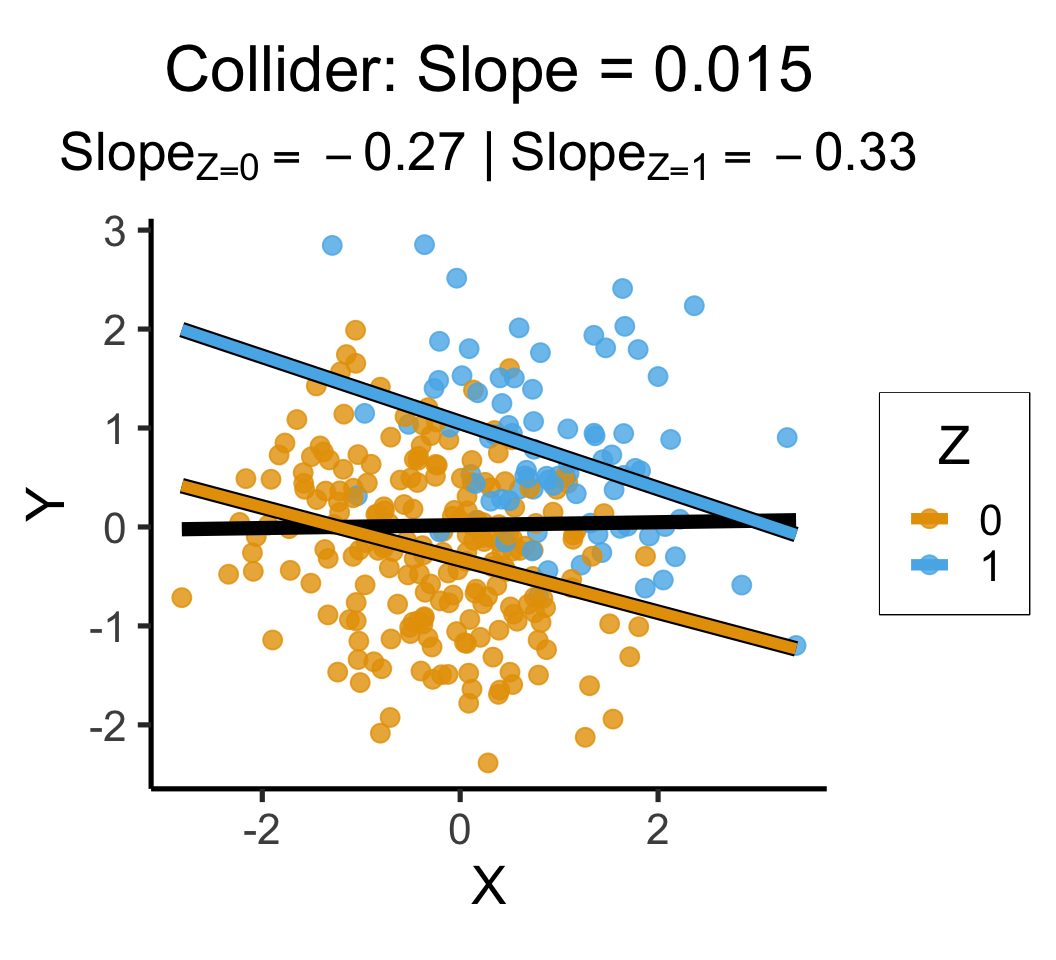

ggplot() +

# Points

geom_point(

data=ccoll_df |> filter(Y > -3),

aes(x=X, y=Y, color=factor(Z)),

size=0.6*g_pointsize,

alpha=0.8

) +

# Overall lm

geom_smooth(

data=ccoll_df, aes(x=X, y=Y),

method = lm, se = FALSE,

linewidth = 2.5, color='black'

) +

# Stratified lm

# (slightly larger black lines)

geom_smooth(

data=ccoll_df,

aes(x=X, y=Y, group=factor(Z)),

method=lm, se=FALSE, fullrange=TRUE,

linewidth=2.75, color='black'

) +

# (Colored lines)

geom_smooth(

data=ccoll_df,

aes(x=X, y=Y, color=factor(Z)),

method=lm, se=FALSE, fullrange=TRUE,

linewidth=2

) +

theme_dsan(base_size=20) +

theme(

plot.title = element_text(size=24),

plot.subtitle = element_text(size=20)

) +

coord_equal() +

labs(

title = paste0(

"Collider: Slope = ",ccoll_slope

),

subtitle=ccoll_z_texlabel,

x = "X", y = "Y", color = "Z"

)

Attaching package: 'extraDistr'The following object is masked from 'package:purrr':

rdunif`geom_smooth()` using formula = 'y ~ x'`geom_smooth()` using formula = 'y ~ x'

`geom_smooth()` using formula = 'y ~ x'

`geom_smooth()` using formula = 'y ~ x'

`geom_smooth()` using formula = 'y ~ x'

`geom_smooth()` using formula = 'y ~ x'

`geom_smooth()` using formula = 'y ~ x'

`geom_smooth()` using formula = 'y ~ x'

`geom_smooth()` using formula = 'y ~ x'

mlr_model = smf.ols(

formula="sales ~ TV + radio + newspaper",

data=ad_df

)

mlr_result = mlr_model.fit()

print(mlr_result.summary().tables[1])==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept 2.9389 0.312 9.422 0.000 2.324 3.554

TV 0.0458 0.001 32.809 0.000 0.043 0.049

radio 0.1885 0.009 21.893 0.000 0.172 0.206

newspaper -0.0010 0.006 -0.177 0.860 -0.013 0.011

==============================================================================radio and newspaper spending constant…

TV advertising is associated withTV and newspaper spending constant…

radio advertising is associated with# print(mlr_result.summary2(float_format='%.3f'))

print(mlr_result.summary2()) Results: Ordinary least squares

=================================================================

Model: OLS Adj. R-squared: 0.896

Dependent Variable: sales AIC: 780.3622

Date: 2026-04-20 18:22 BIC: 793.5555

No. Observations: 200 Log-Likelihood: -386.18

Df Model: 3 F-statistic: 570.3

Df Residuals: 196 Prob (F-statistic): 1.58e-96

R-squared: 0.897 Scale: 2.8409

------------------------------------------------------------------

Coef. Std.Err. t P>|t| [0.025 0.975]

------------------------------------------------------------------

Intercept 2.9389 0.3119 9.4223 0.0000 2.3238 3.5540

TV 0.0458 0.0014 32.8086 0.0000 0.0430 0.0485

radio 0.1885 0.0086 21.8935 0.0000 0.1715 0.2055

newspaper -0.0010 0.0059 -0.1767 0.8599 -0.0126 0.0105

-----------------------------------------------------------------

Omnibus: 60.414 Durbin-Watson: 2.084

Prob(Omnibus): 0.000 Jarque-Bera (JB): 151.241

Skew: -1.327 Prob(JB): 0.000

Kurtosis: 6.332 Condition No.: 454

=================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the

errors is correctly specified.slr_model = smf.ols(

formula="sales ~ newspaper",

data=ad_df

)

slr_result = slr_model.fit()

print(slr_result.summary2()) Results: Ordinary least squares

==================================================================

Model: OLS Adj. R-squared: 0.047

Dependent Variable: sales AIC: 1220.6714

Date: 2026-04-20 18:22 BIC: 1227.2680

No. Observations: 200 Log-Likelihood: -608.34

Df Model: 1 F-statistic: 10.89

Df Residuals: 198 Prob (F-statistic): 0.00115

R-squared: 0.052 Scale: 25.933

-------------------------------------------------------------------

Coef. Std.Err. t P>|t| [0.025 0.975]

-------------------------------------------------------------------

Intercept 12.3514 0.6214 19.8761 0.0000 11.1260 13.5769

newspaper 0.0547 0.0166 3.2996 0.0011 0.0220 0.0874

------------------------------------------------------------------

Omnibus: 6.231 Durbin-Watson: 1.983

Prob(Omnibus): 0.044 Jarque-Bera (JB): 5.483

Skew: 0.330 Prob(JB): 0.064

Kurtosis: 2.527 Condition No.: 65

==================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the

errors is correctly specified.ad_df.drop(columns="id").corr() TV radio newspaper sales

TV 1.000000 0.054809 0.056648 0.782224

radio 0.054809 1.000000 0.354104 0.576223

newspaper 0.056648 0.354104 1.000000 0.228299

sales 0.782224 0.576223 0.228299 1.000000radio our sales will tend to be higher…newspaper in those same markets…sales vs. newspaper, we (correctly!) observe that higher values of newspaper are associated with higher values of sales…newspaper advertising is a surrogate for radio advertising \(\implies\) in our SLR, newspaper “gets credit” for the association between radio and sales\[ \begin{align*} Y &= \beta_0 + \beta_1 \times \texttt{income} \\ &\phantom{Y} \end{align*} \]

credit_df <- read_csv("assets/Credit.csv")Rows: 400 Columns: 11

── Column specification ────────────────────────────────────────────────────────

Delimiter: ","

chr (4): Own, Student, Married, Region

dbl (7): Income, Limit, Rating, Cards, Age, Education, Balance

ℹ Use `spec()` to retrieve the full column specification for this data.

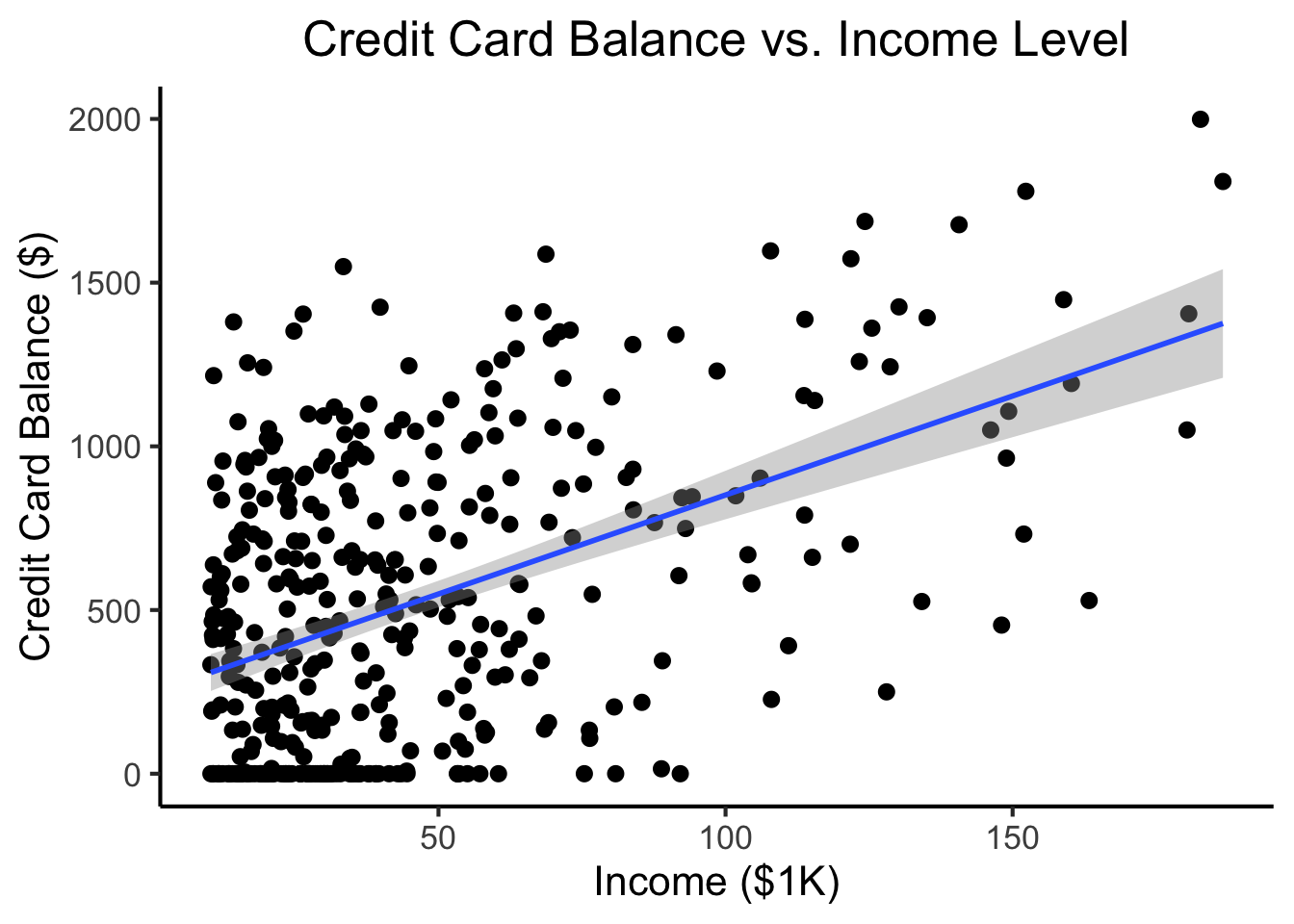

ℹ Specify the column types or set `show_col_types = FALSE` to quiet this message.credit_plot <- credit_df |> ggplot(aes(x=Income, y=Balance)) +

geom_point(size=0.5*g_pointsize) +

geom_smooth(

method='lm', formula="y ~ x", linewidth=1,

fullrange=TRUE

) +

theme_dsan() +

labs(

title="Credit Card Balance vs. Income Level",

x="Income ($1K)",

y="Credit Card Balance ($)"

)

credit_plot

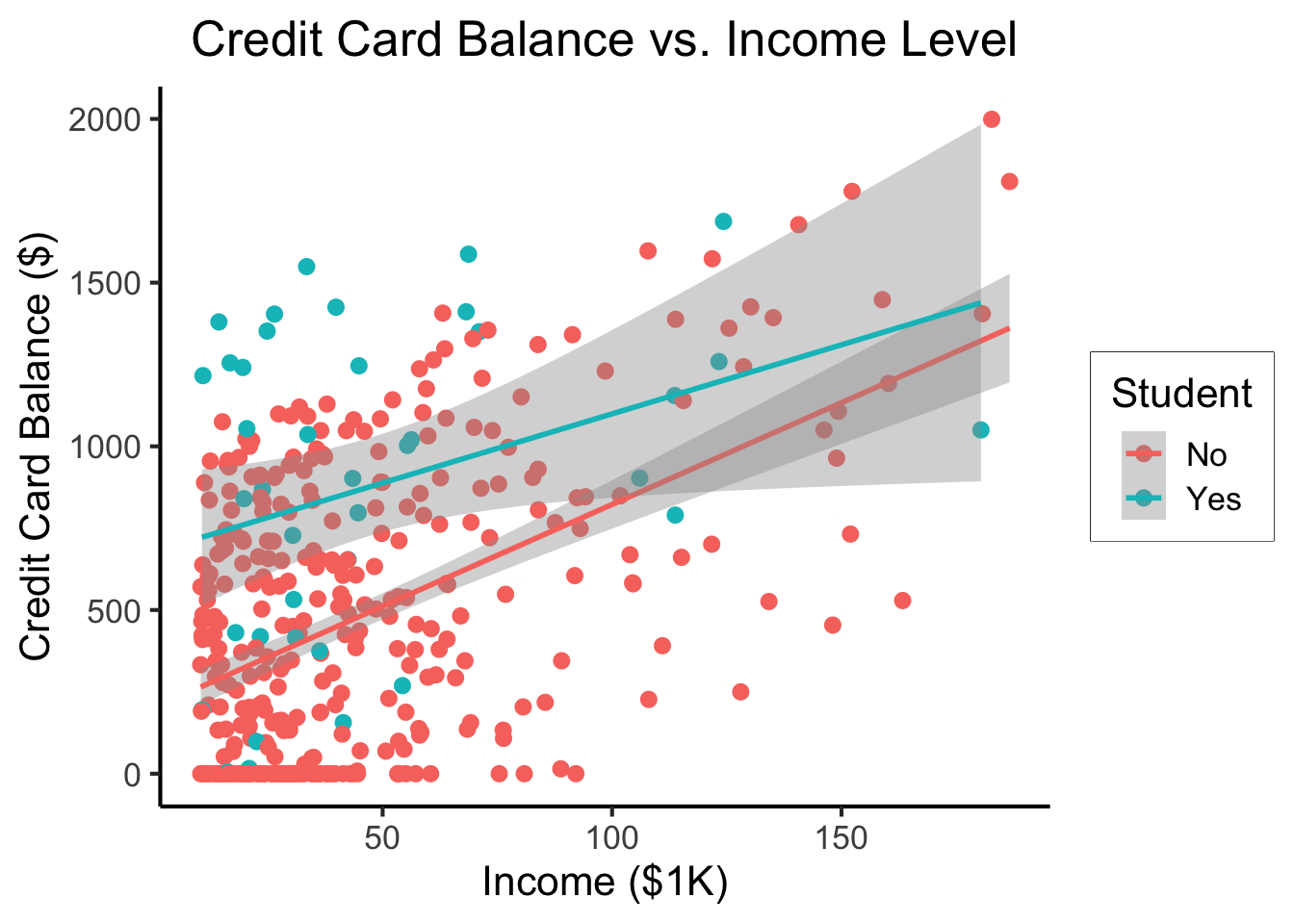

\[ \begin{align*} Y = &\beta_0 + \beta_1 \times \texttt{income} + \beta_2 \times \texttt{Student} \\ &+ \beta_3 \times (\texttt{Student} \times \texttt{Income}) \end{align*} \]

student_plot <- credit_df |> ggplot(aes(x=Income, y=Balance, color=Student)) +

geom_point(size=0.5*g_pointsize) +

geom_smooth(

method='lm', formula="y ~ x", linewidth=1,

fullrange=TRUE

) +

theme_dsan() +

labs(

title="Credit Card Balance vs. Income Level",

x="Income ($1K)",

y="Credit Card Balance ($)"

)

student_plot

\[ \Pr(Y \mid X) = \beta_0 + \beta_1 X + \varepsilon \]

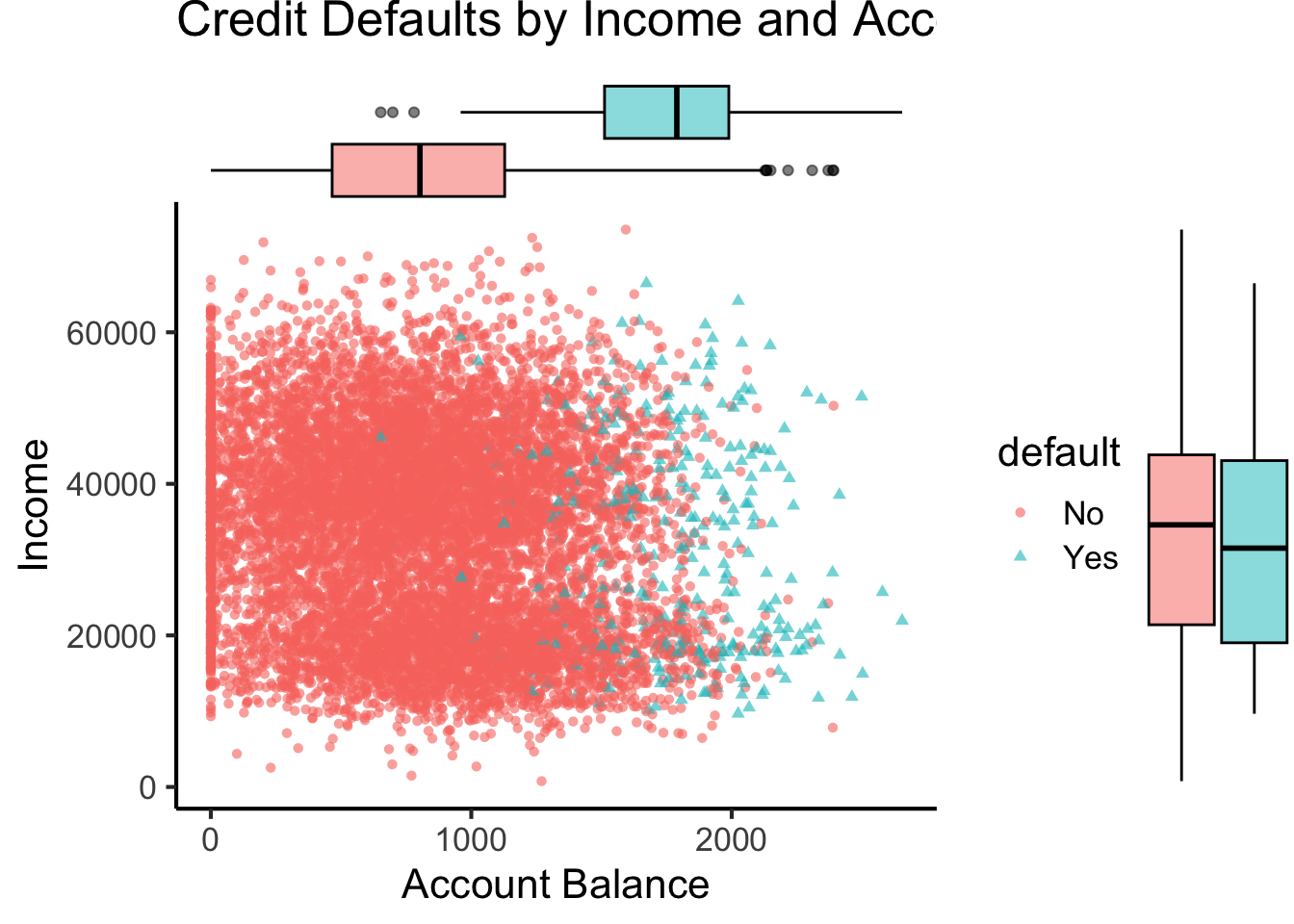

library(tidyverse)

library(ggExtra)

default_df <- read_csv("assets/Default.csv") |>

mutate(default_num = ifelse(default=="Yes",1,0))Rows: 10000 Columns: 4

── Column specification ────────────────────────────────────────────────────────

Delimiter: ","

chr (2): default, student

dbl (2): balance, income

ℹ Use `spec()` to retrieve the full column specification for this data.

ℹ Specify the column types or set `show_col_types = FALSE` to quiet this message.default_plot <- default_df |> ggplot(aes(x=balance, y=income, color=default, shape=default)) +

geom_point(alpha=0.6) +

theme_classic(base_size=16) +

labs(

title="Credit Defaults by Income and Account Balance",

x = "Account Balance",

y = "Income"

)

default_mplot <- default_plot |> ggMarginal(type="boxplot", groupColour=FALSE, groupFill=TRUE)

default_mplot

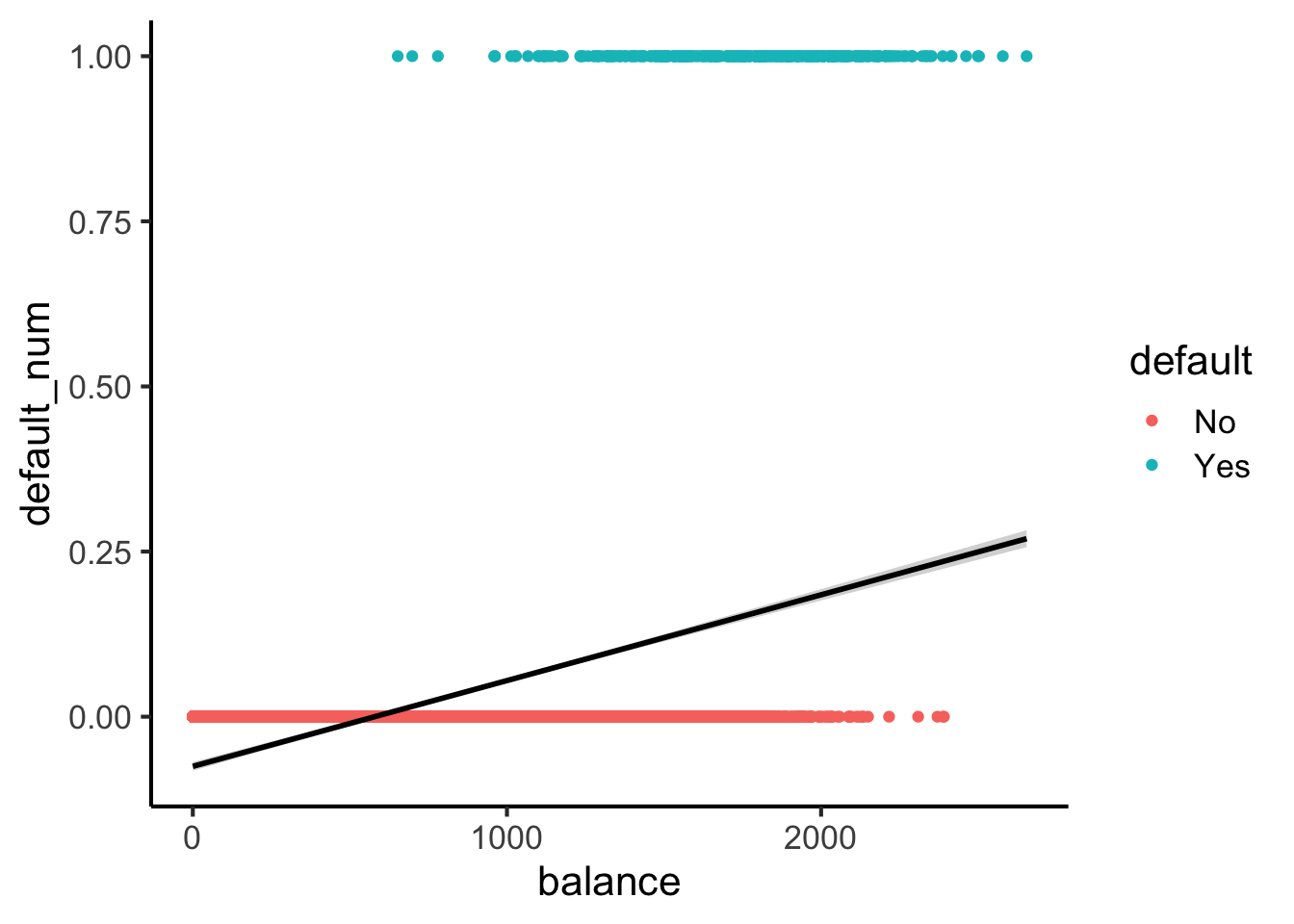

Here’s what lines look like for this dataset:

#lpm_model <- lm(default ~ balance, data=default_df)

default_df |> ggplot(

aes(

x=balance, y=default_num

)

) +

geom_point(aes(color=default)) +

stat_smooth(method="lm", formula=y~x, color='black') +

theme_classic(base_size=16)

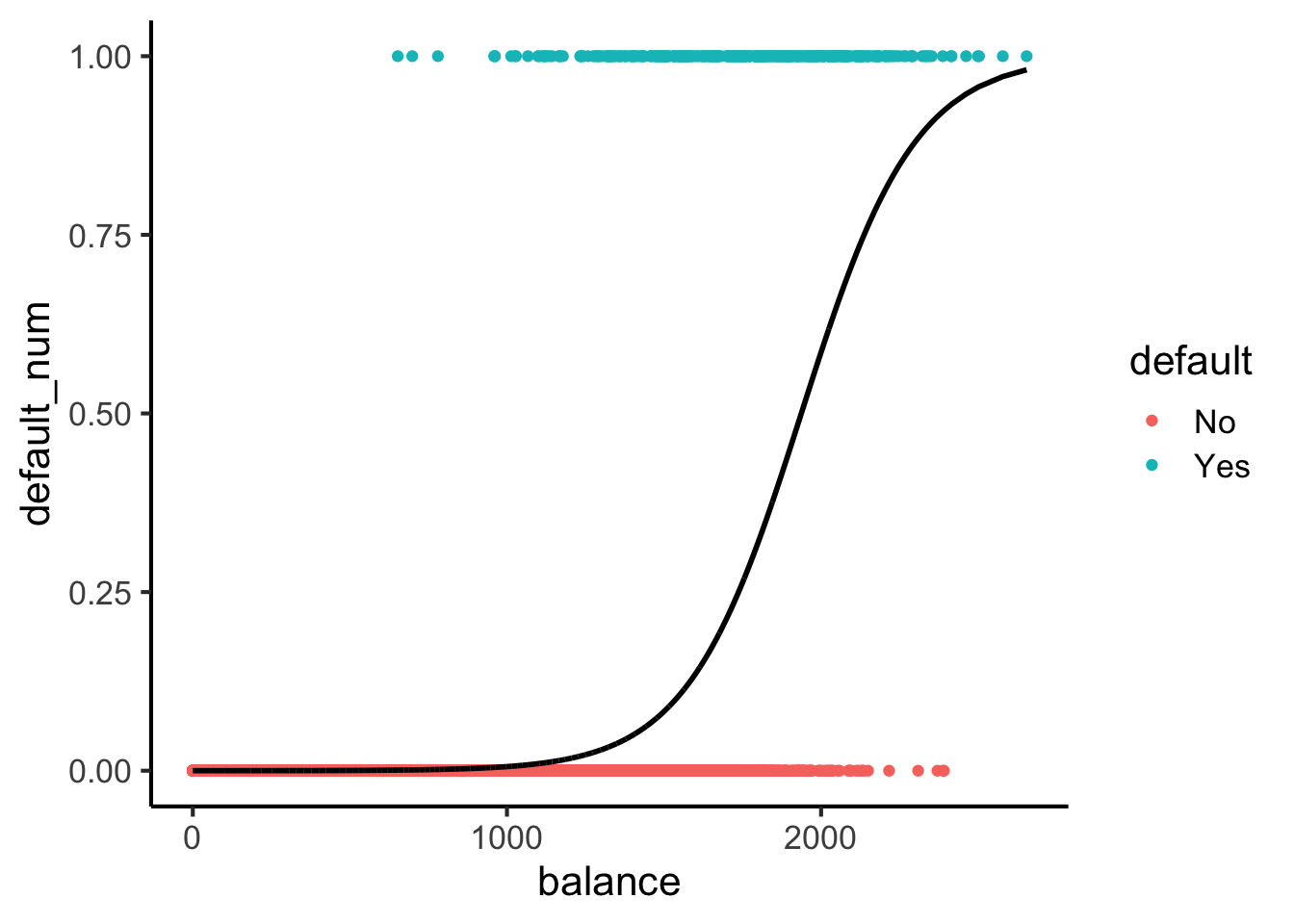

Here’s what sigmoids look like:

library(tidyverse)

logistic_model <- glm(default_num ~ balance, family=binomial(link='logit'),data=default_df)

default_df$predictions <- predict(logistic_model, newdata = default_df, type = "response")

my_sigmoid <- function(x) 1 / (1+exp(-x))

default_df |> ggplot(aes(x=balance, y=default_num)) +

#stat_function(fun=my_sigmoid) +

geom_point(aes(color=default)) +

geom_line(

data=default_df,

aes(x=balance, y=predictions),

linewidth=1

) +

theme_classic(base_size=16)

\[ \Pr(Y \mid X) = \beta_0 + \beta_1 X + \varepsilon \]

\[ \log\underbrace{\left[ \frac{\Pr(Y \mid X)}{1 - \Pr(Y \mid X)} \right]}_{\mathclap{\smash{\text{Odds Ratio}}}} = \beta_0 + \beta_1 X + \varepsilon \]

\[ \begin{align*} \Pr(Y \mid X) &= \frac{e^{\beta_0 + \beta_1X}}{1 + e^{\beta_0 + \beta_1X}} \\ \iff \underbrace{\frac{\Pr(Y \mid X)}{1 - \Pr(Y \mid X)}}_{\text{Odds Ratio}} &= e^{\beta_0 + \beta_1X} \\ \iff \underbrace{\log\left[ \frac{\Pr(Y \mid X)}{1 - \Pr(Y \mid X)} \right]}_{\text{Log-Odds Ratio}} &= \beta_0 + \beta_1X \end{align*} \]

\[ L(\beta_0, \beta_1) = \prod_{\{i \mid y_i = 1\}}\Pr(Y = 1 \mid X) \prod_{\{i \mid y_i = 0\}}(1-\Pr(Y = 1 \mid X)) \]

options(scipen = 9)

print(summary(logistic_model))

Call:

glm(formula = default_num ~ balance, family = binomial(link = "logit"),

data = default_df)

Coefficients:

Estimate Std. Error z value Pr(>|z|)

(Intercept) -10.6513306 0.3611574 -29.49 <2e-16 ***

balance 0.0054989 0.0002204 24.95 <2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

(Dispersion parameter for binomial family taken to be 1)

Null deviance: 2920.6 on 9999 degrees of freedom

Residual deviance: 1596.5 on 9998 degrees of freedom

AIC: 1600.5

Number of Fisher Scoring iterations: 8\[ \begin{align*} &\log\left[ \frac{\Pr(Y = 1 \mid X)}{1 - \Pr(Y = 1 \mid X)} \right] = \beta_0 + \beta_1 X \\ \iff &\Pr(Y = 1 \mid X) = \frac{\exp[\beta_0 + \beta_1X]}{1 + \exp[\beta_0 + \beta_1X]} = \frac{1}{1 + \exp\left[ -(\beta_0 + \beta_1X) \right] } \end{align*} \]

library(tidyverse)

ad_df <- read_csv("assets/Advertising.csv") |> rename(id=`...1`)New names:

Rows: 200 Columns: 5

── Column specification

──────────────────────────────────────────────────────── Delimiter: "," dbl

(5): ...1, TV, radio, newspaper, sales

ℹ Use `spec()` to retrieve the full column specification for this data. ℹ

Specify the column types or set `show_col_types = FALSE` to quiet this message.

• `` -> `...1`mlr_model <- lm(

sales ~ TV + radio + newspaper,

data=ad_df

)

print(summary(mlr_model))

Call:

lm(formula = sales ~ TV + radio + newspaper, data = ad_df)

Residuals:

Min 1Q Median 3Q Max

-8.8277 -0.8908 0.2418 1.1893 2.8292

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 2.938889 0.311908 9.422 <2e-16 ***

TV 0.045765 0.001395 32.809 <2e-16 ***

radio 0.188530 0.008611 21.893 <2e-16 ***

newspaper -0.001037 0.005871 -0.177 0.86

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 1.686 on 196 degrees of freedom

Multiple R-squared: 0.8972, Adjusted R-squared: 0.8956

F-statistic: 570.3 on 3 and 196 DF, p-value: < 2.2e-16radio and newspaper spending constant…

TV advertising is associated withTV and newspaper spending constant…

radio advertising is associated with