Week 3: Getting Fancy with Regression

DSAN 5300: Statistical Learning

Spring 2026, Georgetown University

Monday, January 26, 2026

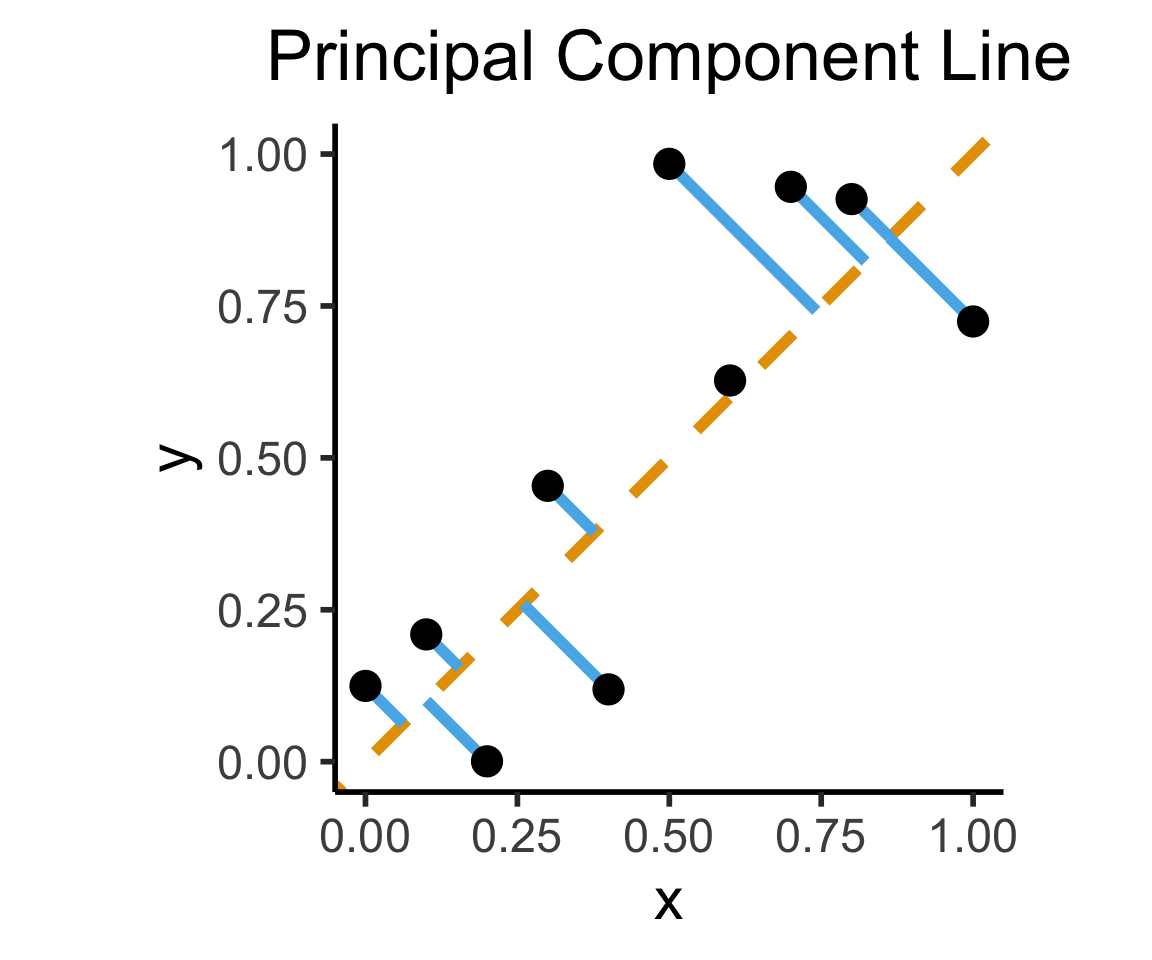

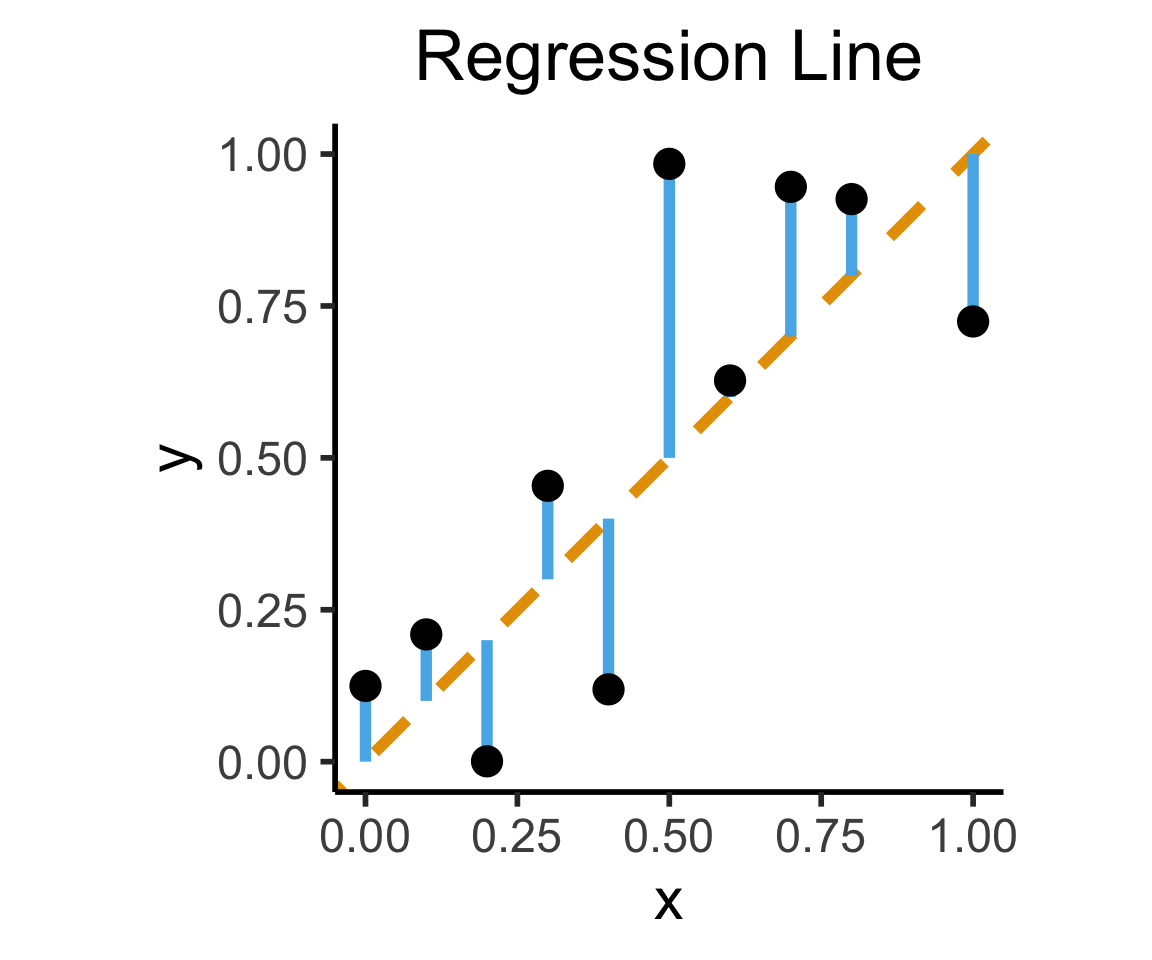

How Do We Define “Best”?

- Intuitively, two different ways to measure how well a line fits the data:

Code

library(tidyverse)

set.seed(5321)

N <- 11

x <- seq(from = 0, to = 1, by = 1 / (N - 1))

y <- x + rnorm(N, 0, 0.2)

mean_y <- mean(y)

spread <- y - mean_y

df <- tibble(x = x, y = y, spread = spread)

ggplot(df, aes(x=x, y=y)) +

geom_abline(slope=1, intercept=0, linetype="dashed", color=cbPalette[1], linewidth=g_linewidth*2) +

geom_segment(xend=(x+y)/2, yend=(x+y)/2, linewidth=g_linewidth*2, color=cbPalette[2]) +

geom_point(size=g_pointsize) +

coord_equal() +

xlim(0, 1) + ylim(0, 1) +

dsan_theme("half") +

labs(

title = "Principal Component Line"

)

ggplot(df, aes(x=x, y=y)) +

geom_abline(slope=1, intercept=0, linetype="dashed", color=cbPalette[1], linewidth=g_linewidth*2) +

geom_segment(xend=x, yend=x, linewidth=g_linewidth*2, color=cbPalette[2]) +

geom_point(size=g_pointsize) +

coord_equal() +

xlim(0, 1) + ylim(0, 1) +

dsan_theme("half") +

labs(

title = "Regression Line"

)

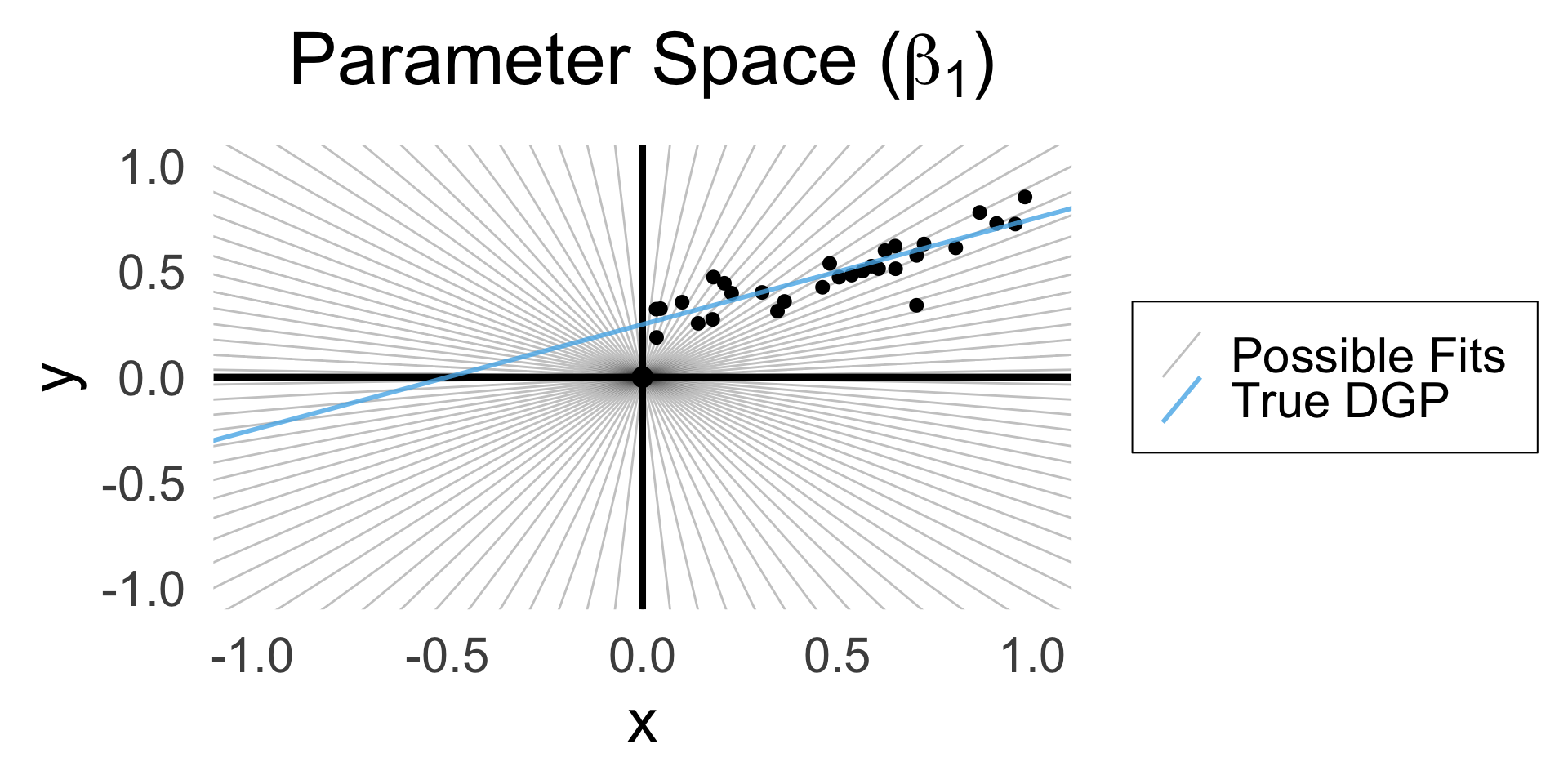

A Sketch

- OLS for regression without intercept: Which line through origin best predicts \(Y\)?

- (Good practice + reminder of how restricted linear models are!)

\[ Y = \beta_1 X + \varepsilon \]

Code

library(latex2exp)

set.seed(5300)

# rand_slope <- log(runif(80, min=0, max=1))

# rand_slope[41:80] <- -rand_slope[41:80]

# rand_lines <- tibble::tibble(

# id=1:80, slope=rand_slope, intercept=0

# )

# angles <- runif(100, -pi/2, pi/2)

angles <- seq(from=-pi/2, to=pi/2, length.out=50)

possible_lines <- tibble::tibble(

slope=tan(angles), intercept=0

)

num_points <- 30

x_vals <- runif(num_points, 0, 1)

y0_vals <- 0.5 * x_vals + 0.25

y_noise <- rnorm(num_points, 0, 0.07)

y_vals <- y0_vals + y_noise

rand_df <- tibble::tibble(x=x_vals, y=y_vals)

title_exp <- TeX("Parameter Space ($\\beta_1$)")

# Main plot object

gen_lines_plot <- function(point_size=2.5) {

lines_plot <- rand_df |> ggplot(aes(x=x, y=y)) +

geom_point(size=point_size) +

geom_hline(yintercept=0, linewidth=1.5) +

geom_vline(xintercept=0, linewidth=1.5) +

# Point at origin

geom_point(data=data.frame(x=0, y=0), aes(x=x, y=y), size=4) +

xlim(-1,1) +

ylim(-1,1) +

# coord_fixed() +

theme_dsan_min(base_size=28)

return(lines_plot)

}

main_lines_plot <- gen_lines_plot()

main_lines_plot +

# Parameter space of possible lines

geom_abline(

data=possible_lines,

aes(slope=slope, intercept=intercept, color='possible'),

# linetype="dotted",

# linewidth=0.75,

alpha=0.25

) +

# True DGP

geom_abline(

aes(

slope=0.5,

intercept=0.25,

color='true'

), linewidth=1, alpha=0.8

) +

scale_color_manual(

element_blank(),

values=c('possible'="black", 'true'=cb_palette[2]),

labels=c('possible'="Possible Fits", 'true'="True DGP")

) +

remove_legend_title() +

labs(

title=title_exp

)

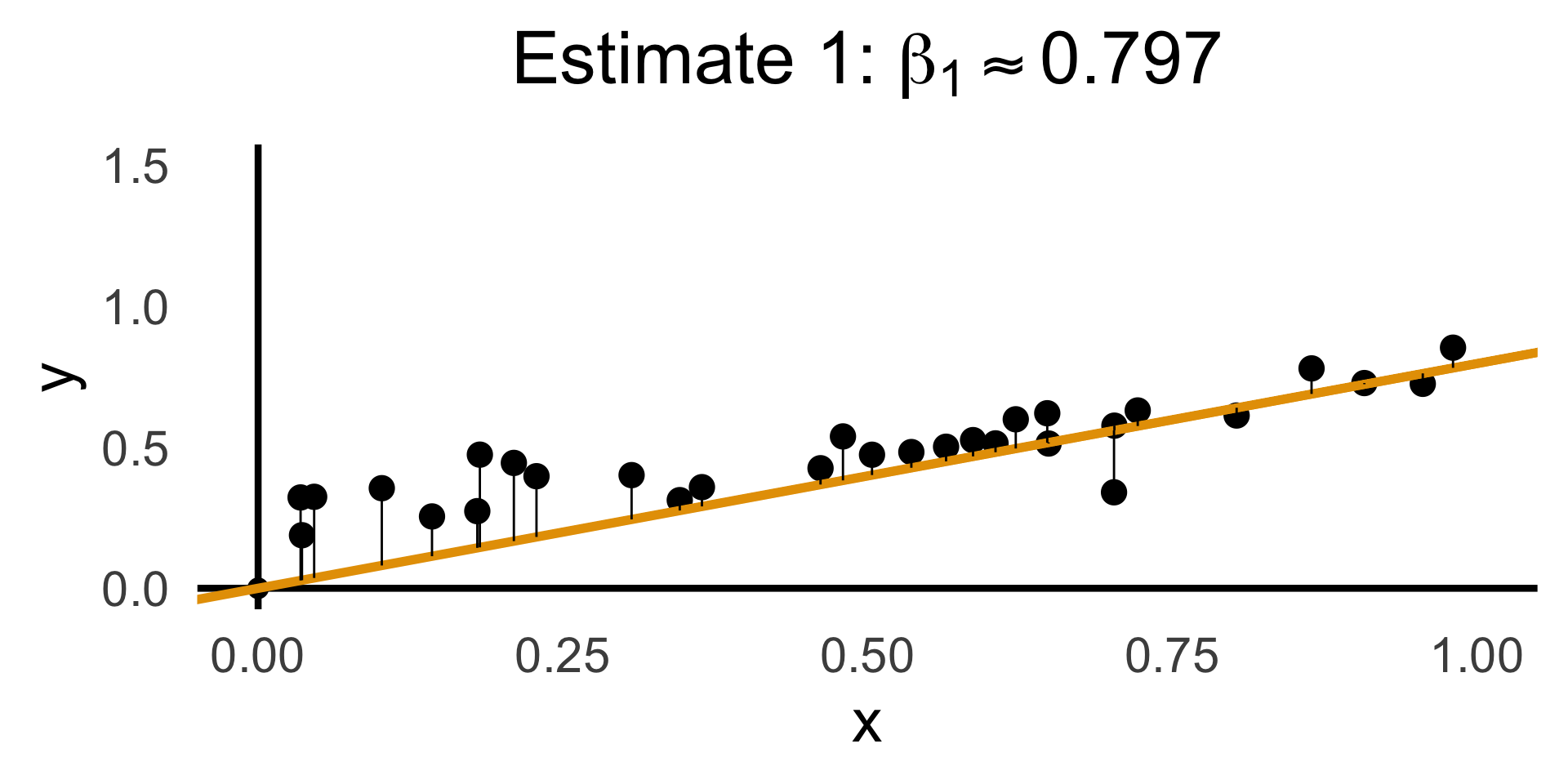

Evaluating with Residuals

Code

rc1_df <- possible_lines |> slice(n() - 14)

# Predictions for this choice

rc1_pred_df <- rand_df |> mutate(

y_pred = rc1_df$slope * x,

resid = y - y_pred

)

rc1_label <- TeX(paste0("Estimate 1: $\\beta_1 \\approx ",round(rc1_df$slope, 3),"$"))

rc1_lines_plot <- gen_lines_plot(point_size=5)

rc1_lines_plot +

geom_abline(

data=rc1_df,

aes(intercept=intercept, slope=slope),

linewidth=2,

color=cb_palette[1]

) +

geom_segment(

data=rc1_pred_df,

aes(x=x, y=y, xend=x, yend=y_pred),

# color=cb_palette[1]

) +

xlim(0, 1) + ylim(0, 1.5) +

labs(

title = rc1_label

)

Code

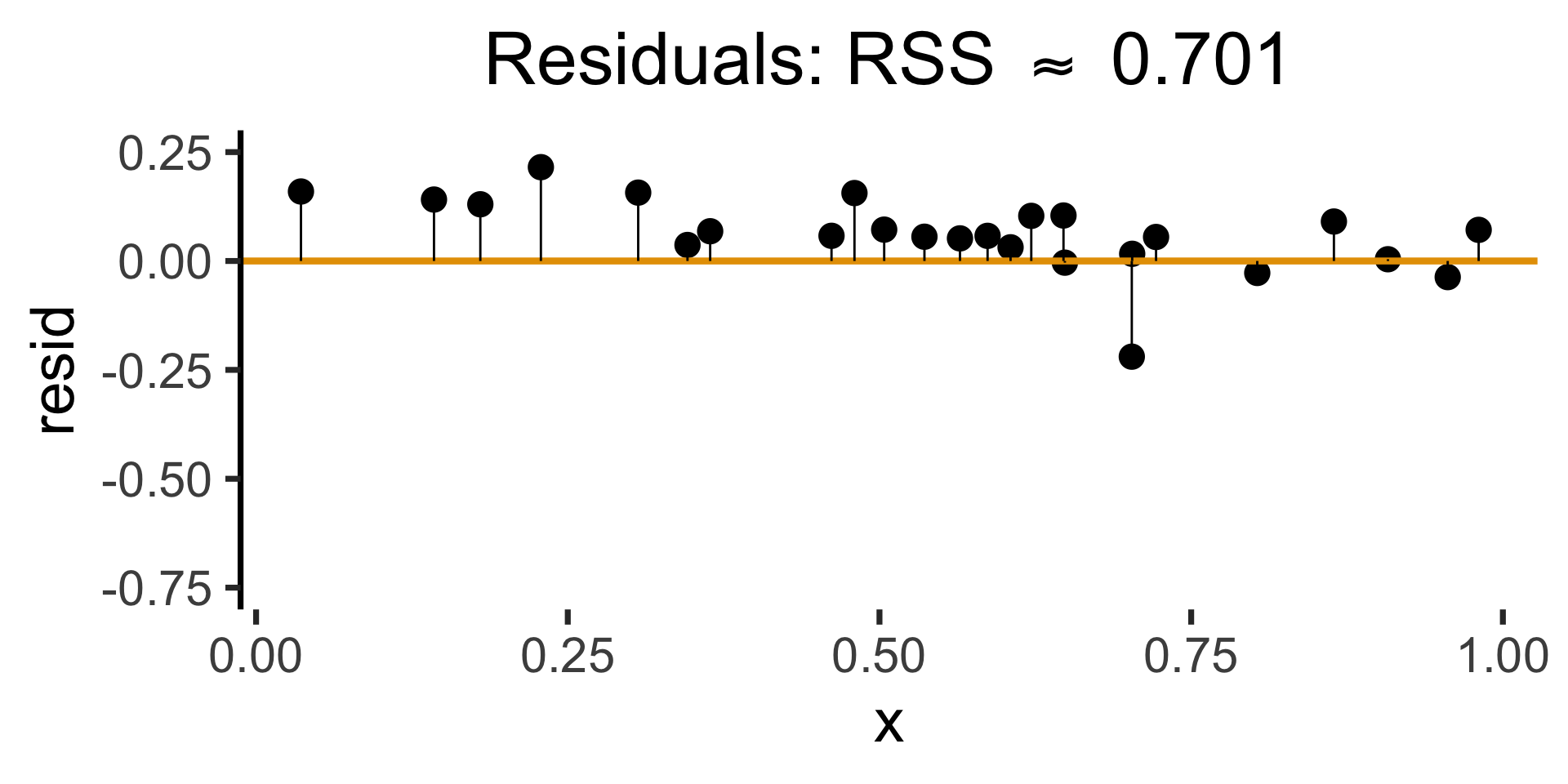

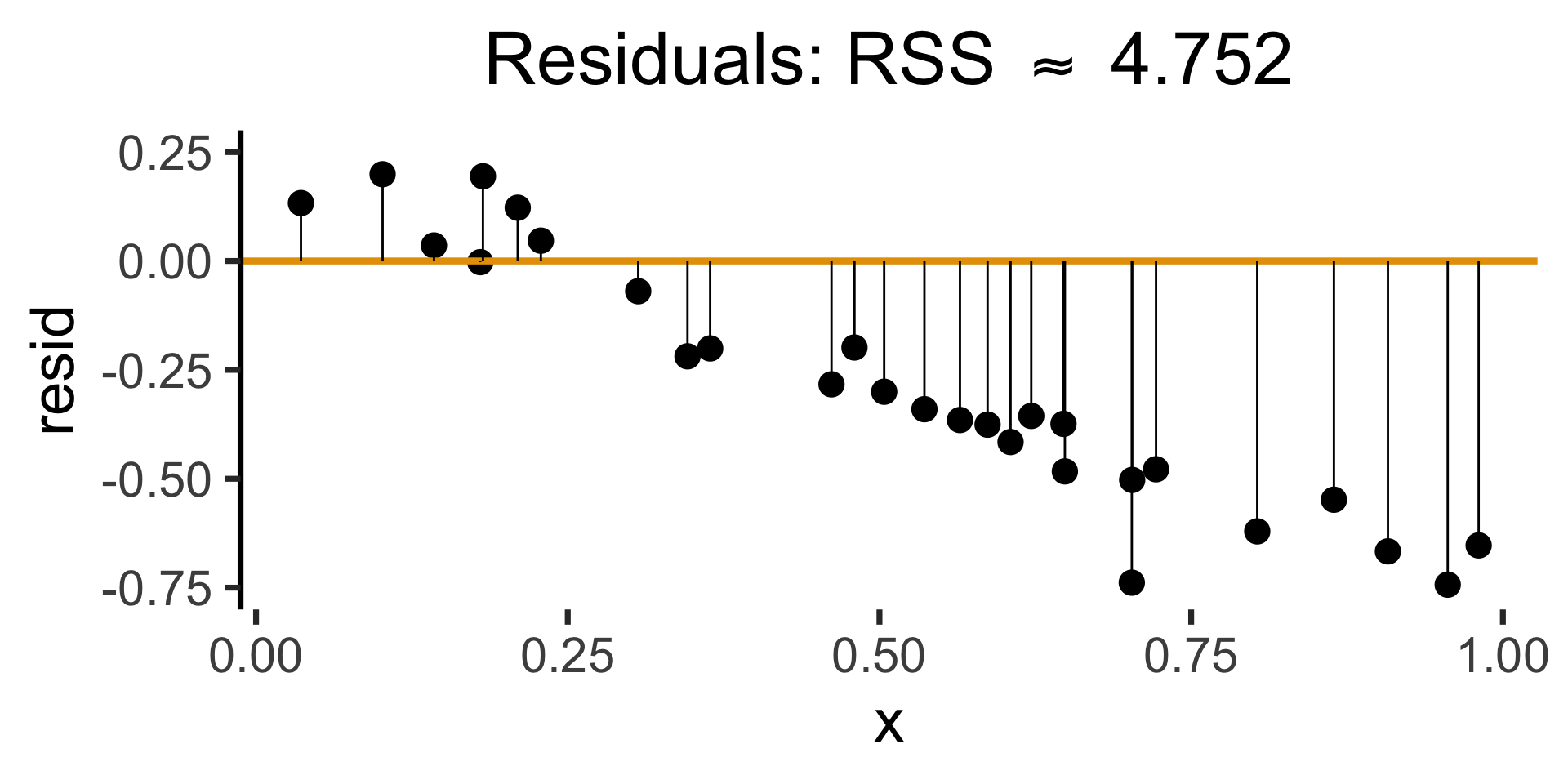

gen_resid_plot <- function(pred_df) {

rc_rss <- sum((pred_df$resid)^2)

rc_resid_label <- TeX(paste0("Residuals: RSS $\\approx$ ",round(rc_rss,3)))

rc_resid_plot <- pred_df |> ggplot(aes(x=x, y=resid)) +

geom_point(size=5) +

geom_hline(

yintercept=0,

color=cb_palette[1],

linewidth=1.5

) +

geom_segment(

aes(xend=x, yend=0)

) +

theme_dsan(base_size=28) +

theme(axis.line.x = element_blank()) +

ylim(-0.75, 0.25) +

labs(

title=rc_resid_label

)

return(rc_resid_plot)

}

rc1_resid_plot <- gen_resid_plot(rc1_pred_df)

rc1_resid_plot

Code

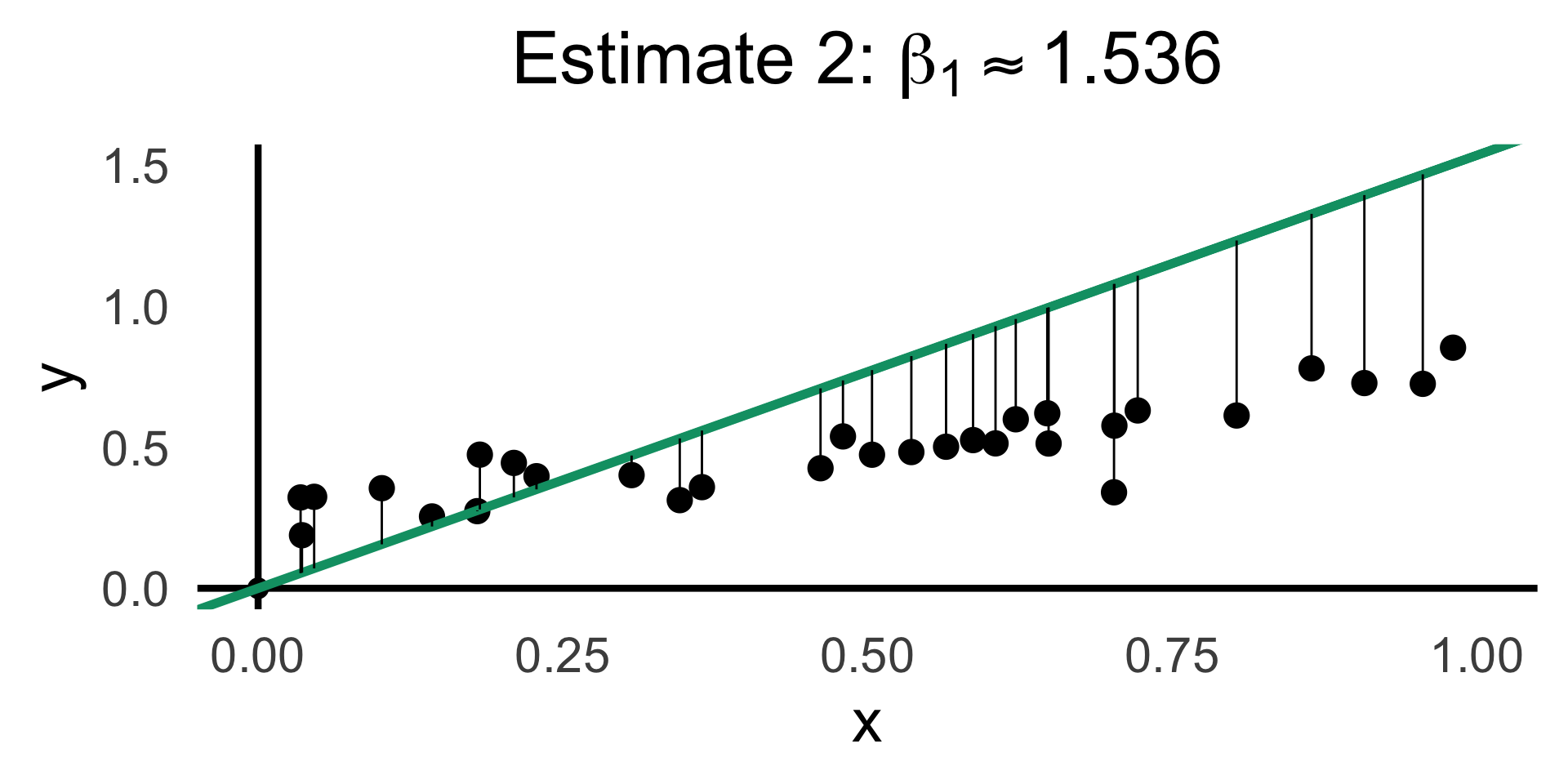

rc2_df <- possible_lines |> slice(n() - 9)

# Predictions for this choice

rc2_pred_df <- rand_df |> mutate(

y_pred = rc2_df$slope * x,

resid = y - y_pred

)

rc2_label <- TeX(paste0("Estimate 2: $\\beta_1 \\approx ",round(rc2_df$slope,3),"$"))

rc2_lines_plot <- gen_lines_plot(point_size=5)

rc2_lines_plot +

geom_abline(

data=rc2_df,

aes(intercept=intercept, slope=slope),

linewidth=2,

color=cb_palette[3]

) +

geom_segment(

data=rc2_pred_df,

aes(

x=x, y=y, xend=x,

# yend=ifelse(y_pred <= 1, y_pred, Inf)

yend=y_pred

)

# color=cb_palette[1]

) +

xlim(0, 1) + ylim(0, 1.5) +

labs(

title=rc2_label

)

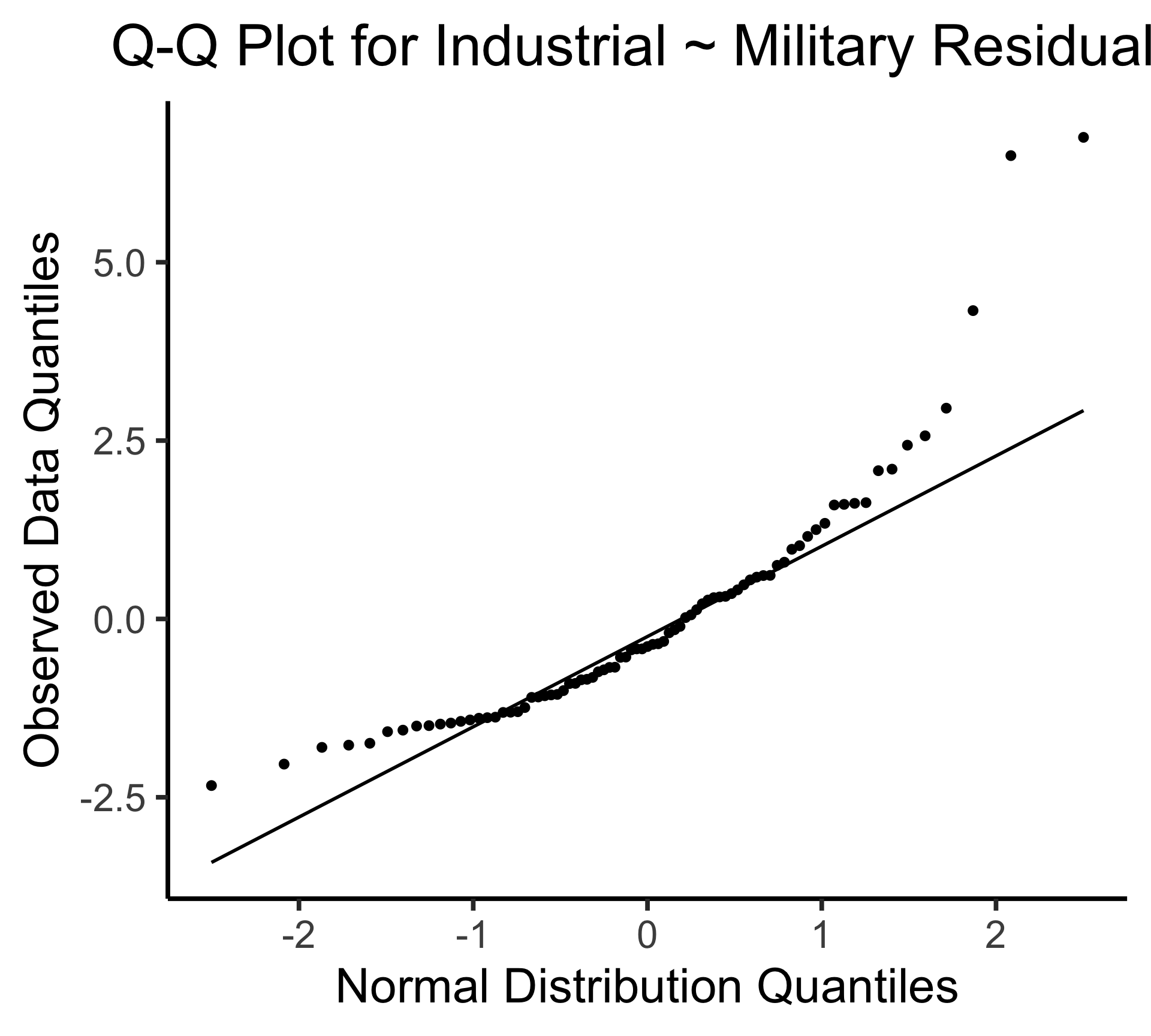

Interpreting Output

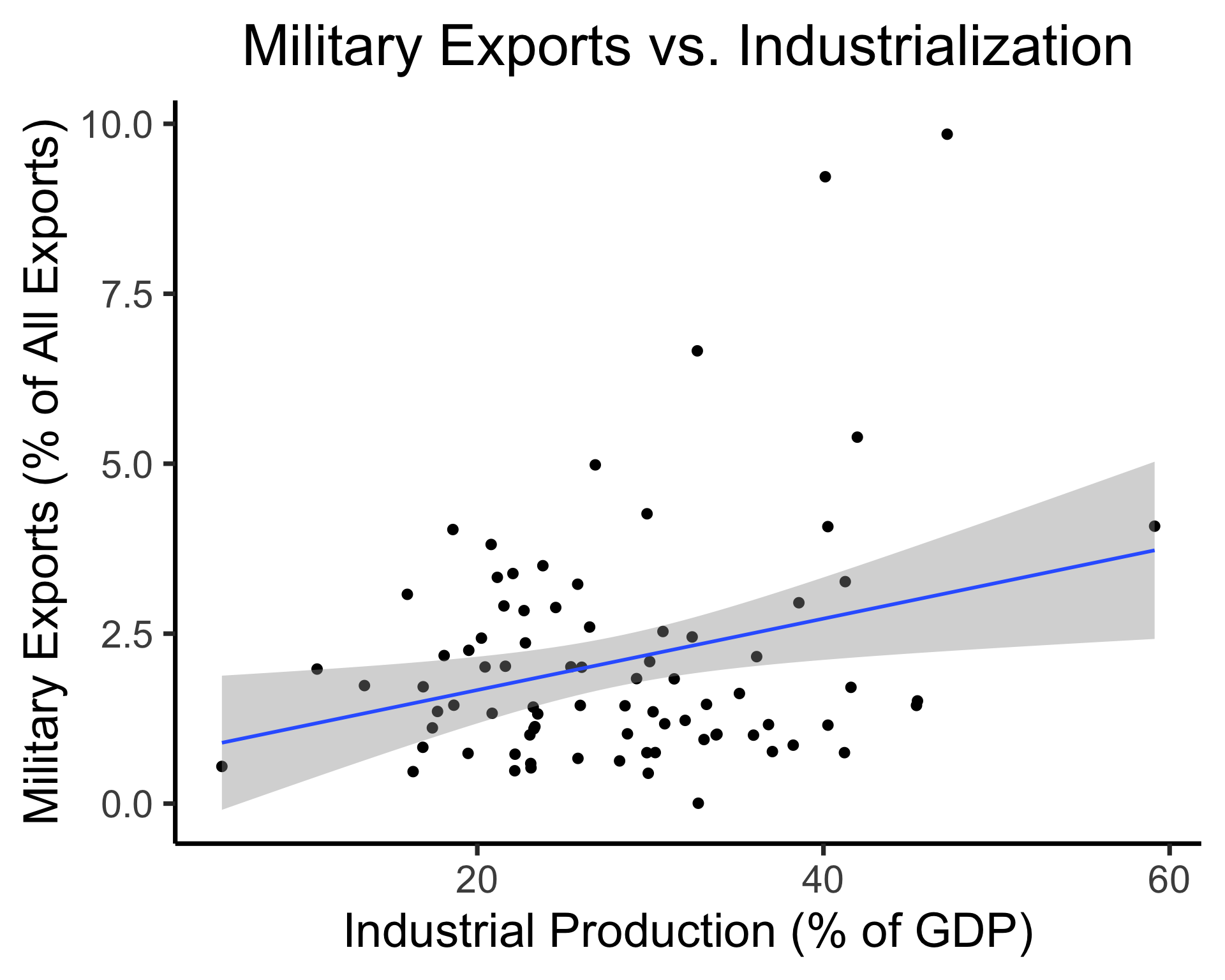

Code

library(tidyverse)

gdp_df <- read_csv("assets/gdp_pca.csv")

mil_plot <- gdp_df |> ggplot(aes(x=industrial, y=military)) +

geom_point(size=0.5*g_pointsize) +

geom_smooth(method='lm', formula="y ~ x", linewidth=1) +

theme_dsan() +

labs(

title="Military Exports vs. Industrialization",

x="Industrial Production (% of GDP)",

y="Military Exports (% of All Exports)"

)

Call:

lm(formula = military ~ industrial, data = gdp_df)

Residuals:

Min 1Q Median 3Q Max

-2.3354 -1.0997 -0.3870 0.6081 6.7508

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 0.61969 0.59526 1.041 0.3010

industrial 0.05253 0.02019 2.602 0.0111 *

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 1.671 on 79 degrees of freedom

(8 observations deleted due to missingness)

Multiple R-squared: 0.07895, Adjusted R-squared: 0.06729

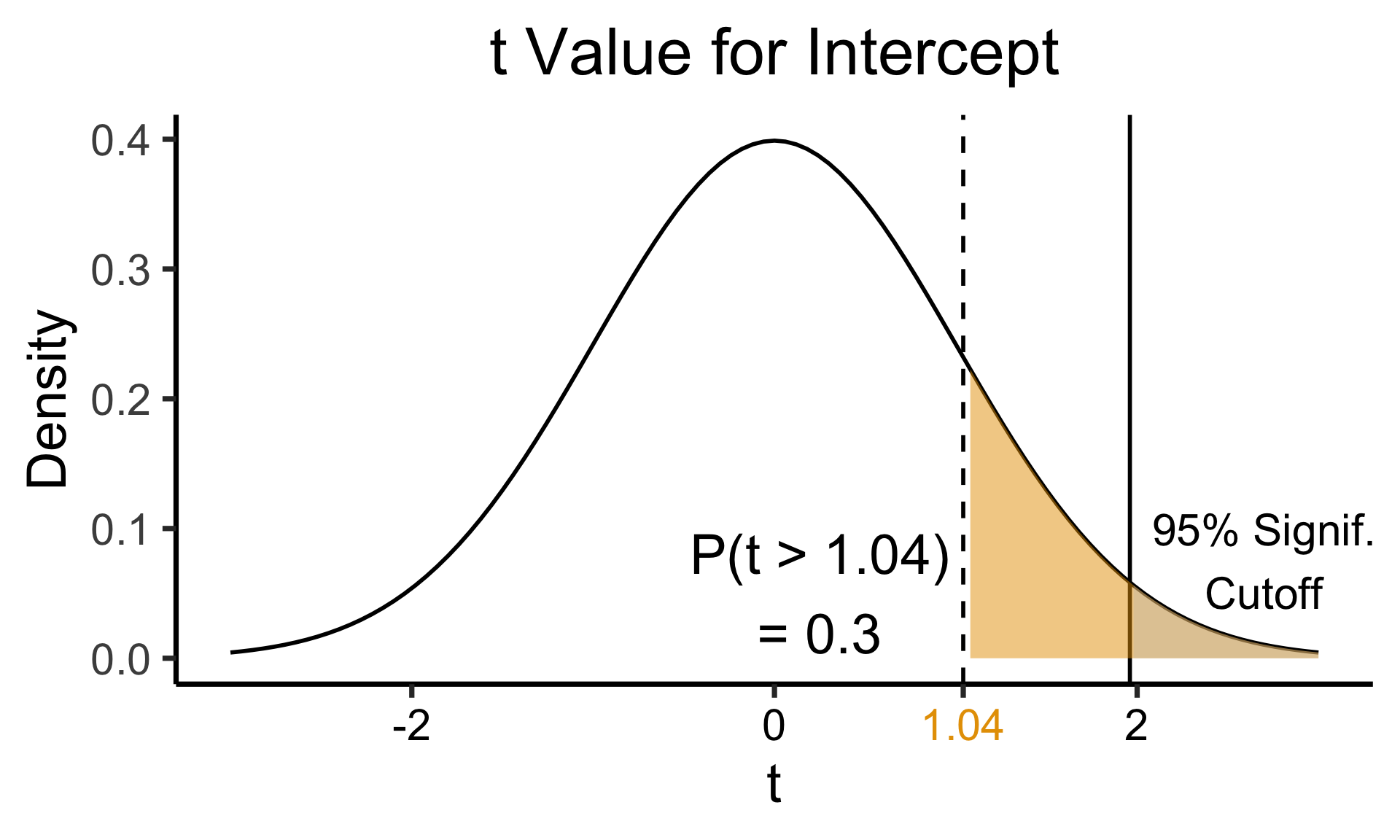

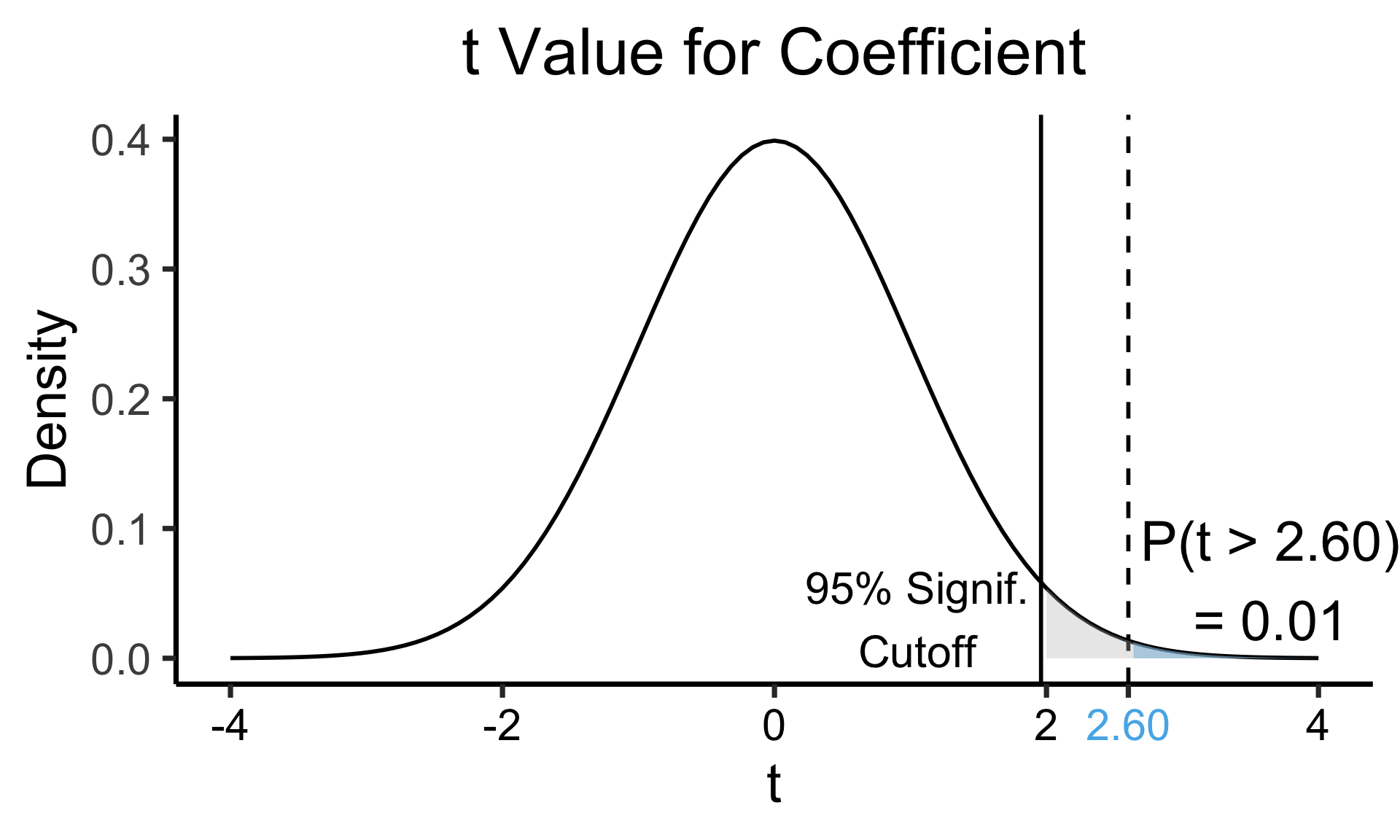

F-statistic: 6.771 on 1 and 79 DF, p-value: 0.01106Zooming In: Significance

| Estimate | Std. Error | t value | Pr(>|t|) | ||

|---|---|---|---|---|---|

| (Intercept) | 0.61969 | 0.59526 | 1.041 | 0.3010 | |

| industrial | 0.05253 | 0.02019 | 2.602 | 0.0111 | * |

| \(\widehat{\beta}\) | Uncertainty | Test stat \(t\) | How extreme is \(t\)? | Signif. Level |

Code

library(ggplot2)

int_tstat <- 1.041

int_tstat_str <- sprintf("%.02f", int_tstat)

label_df_int <- tribble(

~x, ~y, ~label,

0.25, 0.05, paste0("P(t > ",int_tstat_str,")\n= 0.3")

)

label_df_signif_int <- tribble(

~x, ~y, ~label,

2.7, 0.075, "95% Signif.\nCutoff"

)

funcShaded <- function(x, lower_bound, upper_bound){

y <- dnorm(x)

y[x < lower_bound | x > upper_bound] <- NA

return(y)

}

funcShadedIntercept <- function(x) funcShaded(x, int_tstat, Inf)

funcShadedSignif <- function(x) funcShaded(x, 1.96, Inf)

ggplot(data=data.frame(x=c(-3,3)), aes(x=x)) +

stat_function(fun=dnorm, linewidth=g_linewidth) +

geom_vline(aes(xintercept=int_tstat), linewidth=g_linewidth, linetype="dashed") +

geom_vline(aes(xintercept = 1.96), linewidth=g_linewidth, linetype="solid") +

stat_function(fun = funcShadedIntercept, geom = "area", fill = cbPalette[1], alpha = 0.5) +

stat_function(fun = funcShadedSignif, geom = "area", fill = "grey", alpha = 0.333) +

geom_text(label_df_int, mapping = aes(x = x, y = y, label = label), size = 10) +

geom_text(label_df_signif_int, mapping = aes(x = x, y = y, label = label), size = 8) +

# Add single additional tick

scale_x_continuous(breaks=c(-2, 0, int_tstat, 2), labels=c("-2","0",int_tstat_str,"2")) +

dsan_theme("quarter") +

labs(

title = "t Value for Intercept",

x = "t",

y = "Density"

) +

theme(axis.text.x = element_text(colour = c("black", "black", cbPalette[1], "black")))

Code

library(ggplot2)

coef_tstat <- 2.602

coef_tstat_str <- sprintf("%.02f", coef_tstat)

label_df_coef <- tribble(

~x, ~y, ~label,

3.65, 0.06, paste0("P(t > ",coef_tstat_str,")\n= 0.01")

)

label_df_signif_coef <- tribble(

~x, ~y, ~label,

1.05, 0.03, "95% Signif.\nCutoff"

)

funcShadedCoef <- function(x) funcShaded(x, coef_tstat, Inf)

ggplot(data=data.frame(x=c(-4,4)), aes(x=x)) +

stat_function(fun=dnorm, linewidth=g_linewidth) +

geom_vline(aes(xintercept=coef_tstat), linetype="dashed", linewidth=g_linewidth) +

geom_vline(aes(xintercept=1.96), linetype="solid", linewidth=g_linewidth) +

stat_function(fun = funcShadedCoef, geom = "area", fill = cbPalette[2], alpha = 0.5) +

stat_function(fun = funcShadedSignif, geom = "area", fill = "grey", alpha = 0.333) +

# Label shaded area

geom_text(label_df_coef, mapping = aes(x = x, y = y, label = label), size = 10) +

# Label significance cutoff

geom_text(label_df_signif_coef, mapping = aes(x = x, y = y, label = label), size = 8) +

coord_cartesian(clip = "off") +

# Add single additional tick

scale_x_continuous(breaks=c(-4, -2, 0, 2, coef_tstat, 4), labels=c("-4", "-2","0", "2", coef_tstat_str,"4")) +

dsan_theme("quarter") +

labs(

title = "t Value for Coefficient",

x = "t",

y = "Density"

) +

theme(axis.text.x = element_text(colour = c("black", "black", "black", "black", cbPalette[2], "black")))

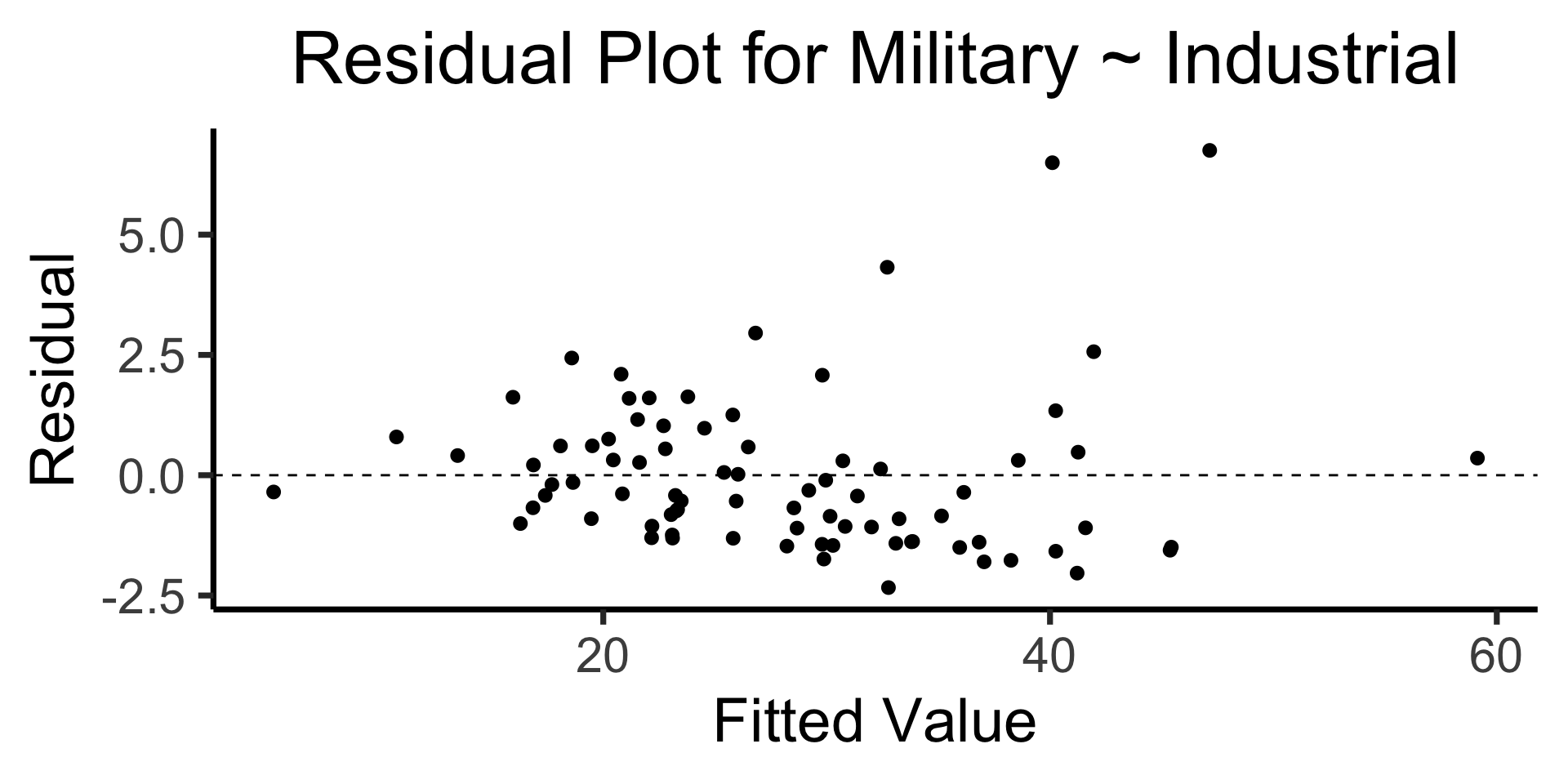

The Residual Plot

Recall homoskedasticity assumption: Given our model

\[ y_i = \beta_0 + \beta_1x_i + \varepsilon_i \]

the errors \(\varepsilon_i\) should not vary systematically with \(i\)

Formally: \(\forall i \left[ \Var{\varepsilon_i} = \sigma^2 \right]\)

Code

library(broom)

gdp_resid_df <- augment(gdp_model)

ggplot(gdp_resid_df, aes(x = industrial, y = .resid)) +

geom_point(size = g_pointsize/2) +

geom_hline(yintercept=0, linetype="dashed") +

dsan_theme("quarter") +

labs(

title = "Residual Plot for Military ~ Industrial",

x = "Fitted Value",

y = "Residual"

)

Code

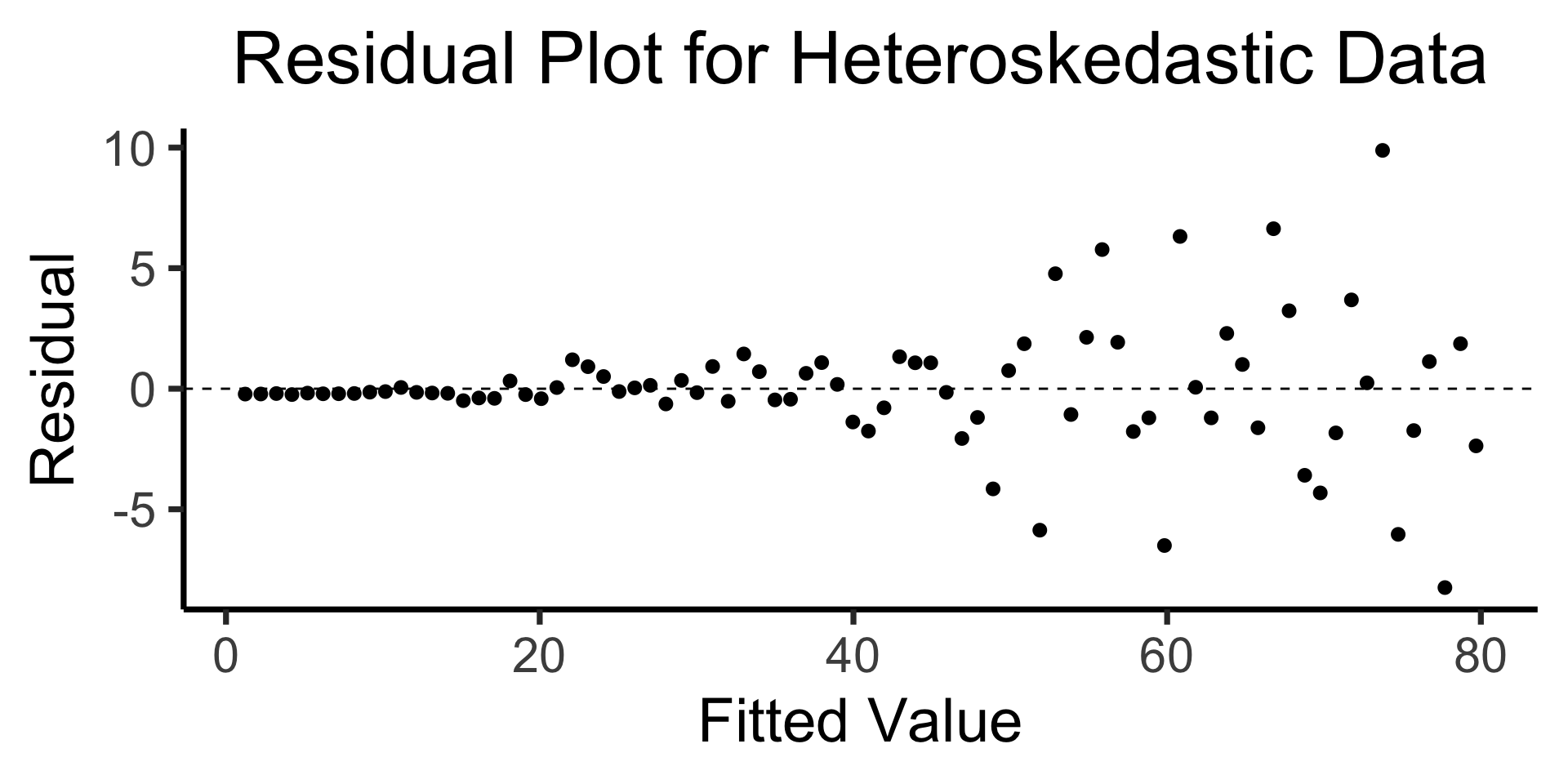

x <- 1:80

errors <- rnorm(length(x), 0, x^2/1000)

y <- x + errors

het_model <- lm(y ~ x)

df_het <- augment(het_model)

ggplot(df_het, aes(x = .fitted, y = .resid)) +

geom_point(size = g_pointsize / 2) +

geom_hline(yintercept = 0, linetype = "dashed") +

dsan_theme("quarter") +

labs(

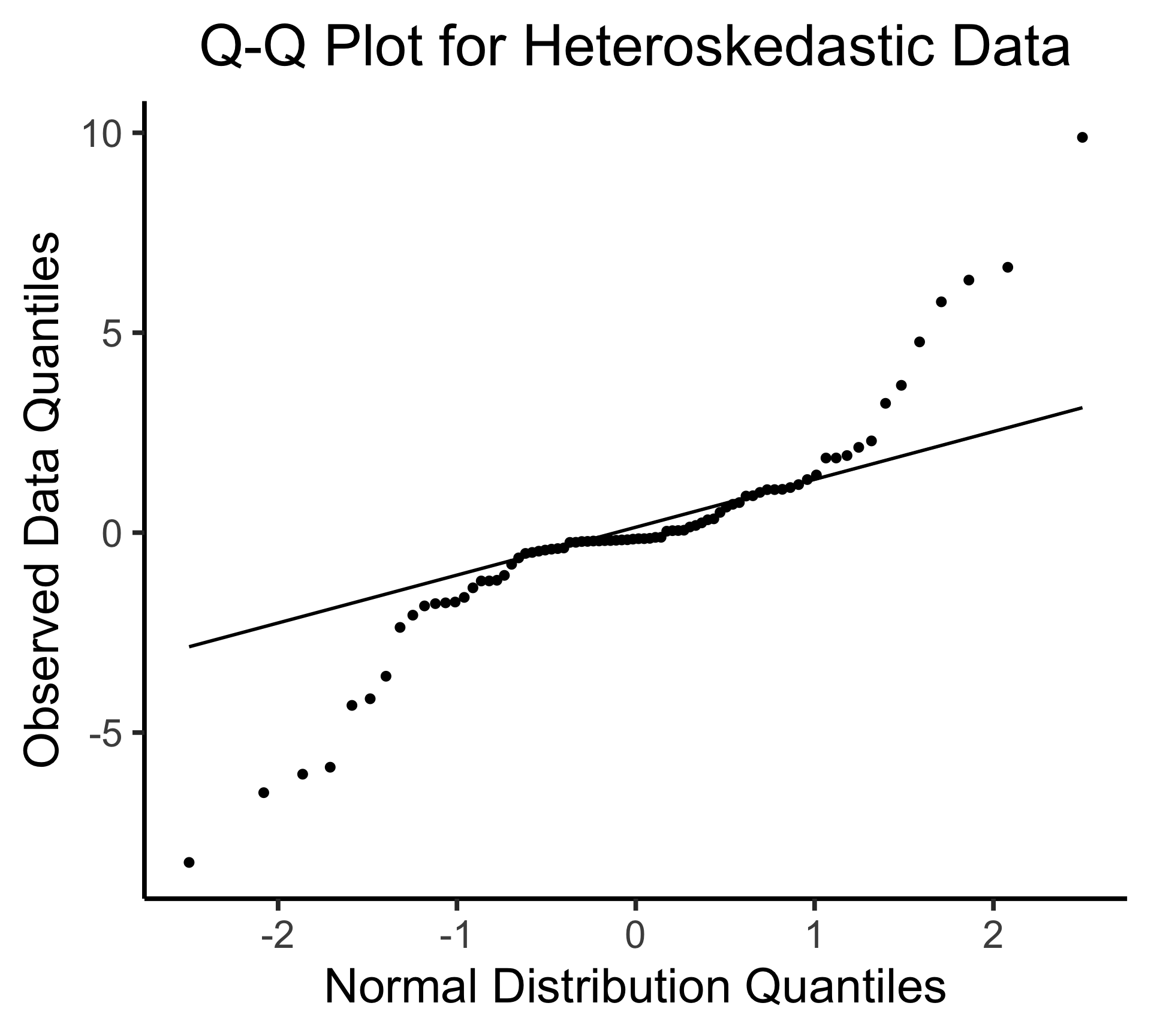

title = "Residual Plot for Heteroskedastic Data",

x = "Fitted Value",

y = "Residual"

)

Q-Q Plot

- If \((\widehat{y} - y) \sim \mathcal{N}(0, \sigma^2)\), points would lie on 45° line:

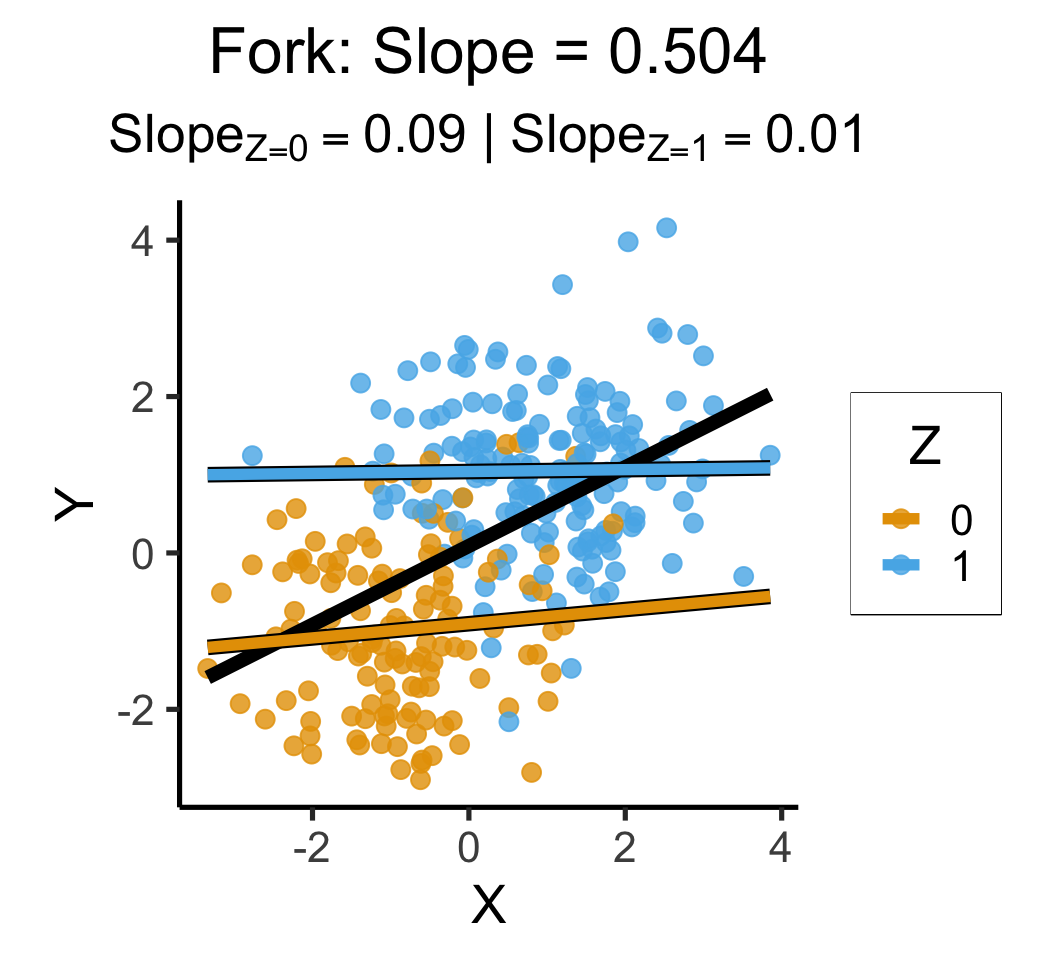

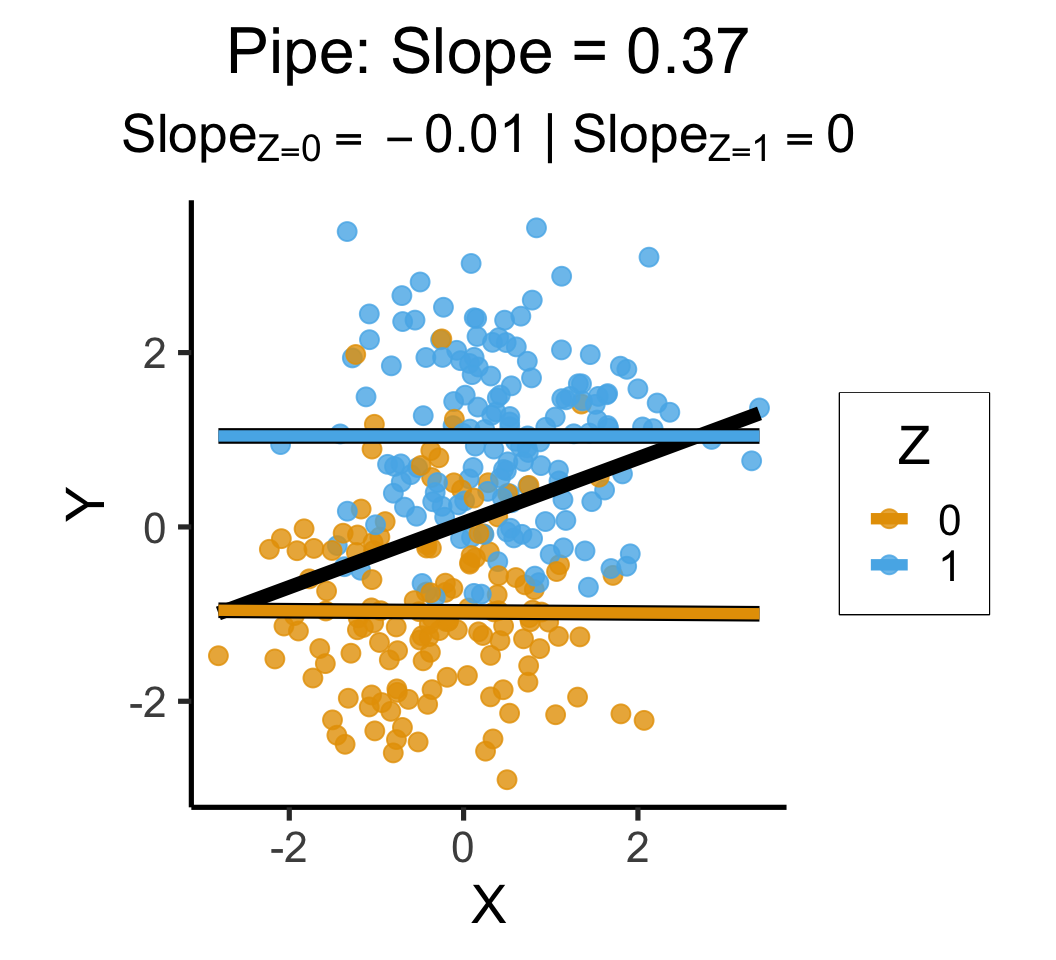

“Holding” Things “Constant”?

- One of the more confusing ideas in all of statistics…

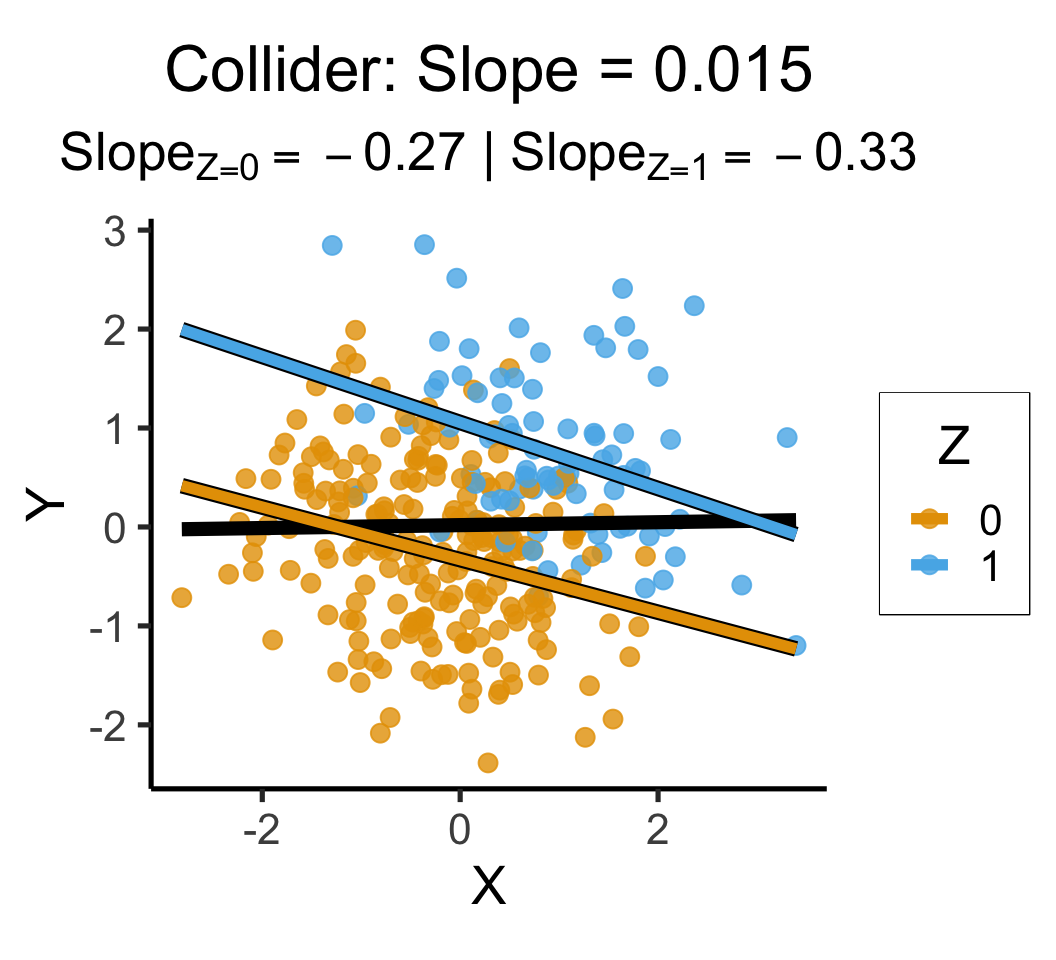

- “Controlling for” some types of variables (forks, pipes) removes spurious correlation, but “controlling for” other types (colliders) introduces more spurious correlation

- Opinionated “what you should really do”: center independent variables

- \(Y = \beta_0 + \beta_1 (X - \mu)\) \(\Rightarrow\) “When other variables are at their mean values, 1 unit increase in \(X_i\) associated with \(\beta_i\) unit increase in \(y\)”

Code

library(extraDistr)

set.seed(5650)

n_c <- 300

cfork_df <- tibble(

Z = rbern(n_c),

X = rnorm(n_c, 2 * Z - 1),

Y = rnorm(n_c, 2 * Z - 1)

)

library(latex2exp)

overall_lm <- lm(Y ~ X, data=cfork_df)

overall_slope <- round(overall_lm$coef['X'], 3)

z0_lm <- lm(Y ~ X, data=cfork_df |> filter(Z == 0))

z0_slope <- round(z0_lm$coef['X'], 2)

z0_label <- paste0("$Slope_{Z=0} = ",z0_slope,"$")

z0_leg_label <- TeX(paste0("0 $(m=",z0_slope,")$"))

z1_lm <- lm(Y ~ X, data=cfork_df |> filter(Z == 1))

z1_slope <- round(z1_lm$coef['X'], 2)

z1_label <- paste0("$Slope_{Z=1} = ",z1_slope,"$")

z_texlabel <- TeX(paste0(z0_label, " | ", z1_label))

cfork_xmin <- min(cfork_df$X)

cfork_xmax <- max(cfork_df$X)

ggplot() +

# Points

geom_point(

data=cfork_df,

aes(x=X, y=Y, color=factor(Z)),

size=0.6*g_pointsize,

alpha=0.8

) +

# Overall lm

geom_smooth(

data=cfork_df, aes(x=X, y=Y),

method = lm, se = FALSE,

linewidth = 2.5, color='black'

) +

# Stratified lm

# (slightly larger black lines)

geom_smooth(

data=cfork_df,

aes(x=X, y=Y, group=factor(Z)),

method=lm, se=FALSE, fullrange=TRUE,

linewidth=2.75, color='black'

) +

# (Colored lines)

geom_smooth(

data=cfork_df,

aes(x=X, y=Y, color=factor(Z)),

method=lm, se=FALSE, fullrange=TRUE,

linewidth=2

) +

theme_dsan(base_size=20) +

theme(

plot.title = element_text(size=24),

plot.subtitle = element_text(size=20)

) +

coord_equal() +

labs(

title = paste0(

"Fork: Slope = ",overall_slope

),

subtitle=z_texlabel,

x = "X", y = "Y", color = "Z"

)

set.seed(5650)

cpipe_df <- tibble(

X = rnorm(n_c),

Z = rbern(n_c, plogis(X)),

Y = rnorm(n_c, 2 * Z - 1)

)

cpipe_lm <- lm(Y ~ X, data=cpipe_df)

cpipe_slope <- round(cpipe_lm$coef['X'], 3)

cpipe_z0_lm <- lm(Y ~ X, data=cpipe_df |> filter(Z == 0))

cpipe_z0_slope <- round(cpipe_z0_lm$coef['X'], 2)

cpipe_z0_label <- paste0("$Slope_{Z=0} = ",cpipe_z0_slope,"$")

cpipe_z1_lm <- lm(Y ~ X, data=cpipe_df |> filter(Z == 1))

cpipe_z1_slope <- round(cpipe_z1_lm$coef['X'], 2)

cpipe_z1_label <- paste0("$Slope_{Z=1} = ",cpipe_z1_slope,"$")

cpipe_z_texlabel <- TeX(paste0(cpipe_z0_label, " | ", cpipe_z1_label))

cpipe_xmin <- min(cpipe_df$X)

cpipe_xmax <- max(cpipe_df$X)

ggplot() +

# Points

geom_point(

data=cpipe_df |> filter(Y > -3),

aes(x=X, y=Y, color=factor(Z)),

size=0.6*g_pointsize,

alpha=0.8

) +

# Overall lm

geom_smooth(

data=cpipe_df, aes(x=X, y=Y),

method = lm, se = FALSE,

linewidth = 2.5, color='black'

) +

# Stratified lm

# (slightly larger black lines)

geom_smooth(

data=cpipe_df,

aes(x=X, y=Y, group=factor(Z)),

method=lm, se=FALSE, fullrange=TRUE,

linewidth=2.75, color='black'

) +

# (Colored lines)

geom_smooth(

data=cpipe_df,

aes(x=X, y=Y, color=factor(Z)),

method=lm, se=FALSE, fullrange=TRUE,

linewidth=2

) +

theme_dsan(base_size=20) +

theme(

plot.title = element_text(size=24),

plot.subtitle = element_text(size=20)

) +

coord_equal() +

labs(

title = paste0(

"Pipe: Slope = ",cpipe_slope

),

subtitle=cpipe_z_texlabel,

x = "X", y = "Y", color = "Z"

)

set.seed(5650)

ccoll_df <- tibble(

X = rnorm(n_c),

Y = rnorm(n_c),

Z = rbern(n_c, plogis(2 * (X + Y - 1)))

)

ccoll_lm <- lm(Y ~ X, data=ccoll_df)

ccoll_slope <- round(ccoll_lm$coef['X'], 3)

ccoll_z0_lm <- lm(Y ~ X, data=ccoll_df |> filter(Z == 0))

ccoll_z0_slope <- round(ccoll_z0_lm$coef['X'], 2)

ccoll_z0_label <- paste0("$Slope_{Z=0} = ",ccoll_z0_slope,"$")

ccoll_z1_lm <- lm(Y ~ X, data=ccoll_df |> filter(Z == 1))

ccoll_z1_slope <- round(ccoll_z1_lm$coef['X'], 2)

ccoll_z1_label <- paste0("$Slope_{Z=1} = ",ccoll_z1_slope,"$")

ccoll_z_texlabel <- TeX(paste0(ccoll_z0_label, " | ", ccoll_z1_label))

ccoll_xmin <- min(ccoll_df$X)

ccoll_xmax <- max(ccoll_df$X)

ggplot() +

# Points

geom_point(

data=ccoll_df |> filter(Y > -3),

aes(x=X, y=Y, color=factor(Z)),

size=0.6*g_pointsize,

alpha=0.8

) +

# Overall lm

geom_smooth(

data=ccoll_df, aes(x=X, y=Y),

method = lm, se = FALSE,

linewidth = 2.5, color='black'

) +

# Stratified lm

# (slightly larger black lines)

geom_smooth(

data=ccoll_df,

aes(x=X, y=Y, group=factor(Z)),

method=lm, se=FALSE, fullrange=TRUE,

linewidth=2.75, color='black'

) +

# (Colored lines)

geom_smooth(

data=ccoll_df,

aes(x=X, y=Y, color=factor(Z)),

method=lm, se=FALSE, fullrange=TRUE,

linewidth=2

) +

theme_dsan(base_size=20) +

theme(

plot.title = element_text(size=24),

plot.subtitle = element_text(size=20)

) +

coord_equal() +

labs(

title = paste0(

"Collider: Slope = ",ccoll_slope

),

subtitle=ccoll_z_texlabel,

x = "X", y = "Y", color = "Z"

)

Visualizing MLR

(ISLR, Fig 3.5): A pronounced non-linear relationship. Positive residuals (visible above the surface) tend to lie along the 45-degree line, where budgets are split evenly. Negative residuals (most not visible) tend to be away from this line, where budgets are more lopsided.

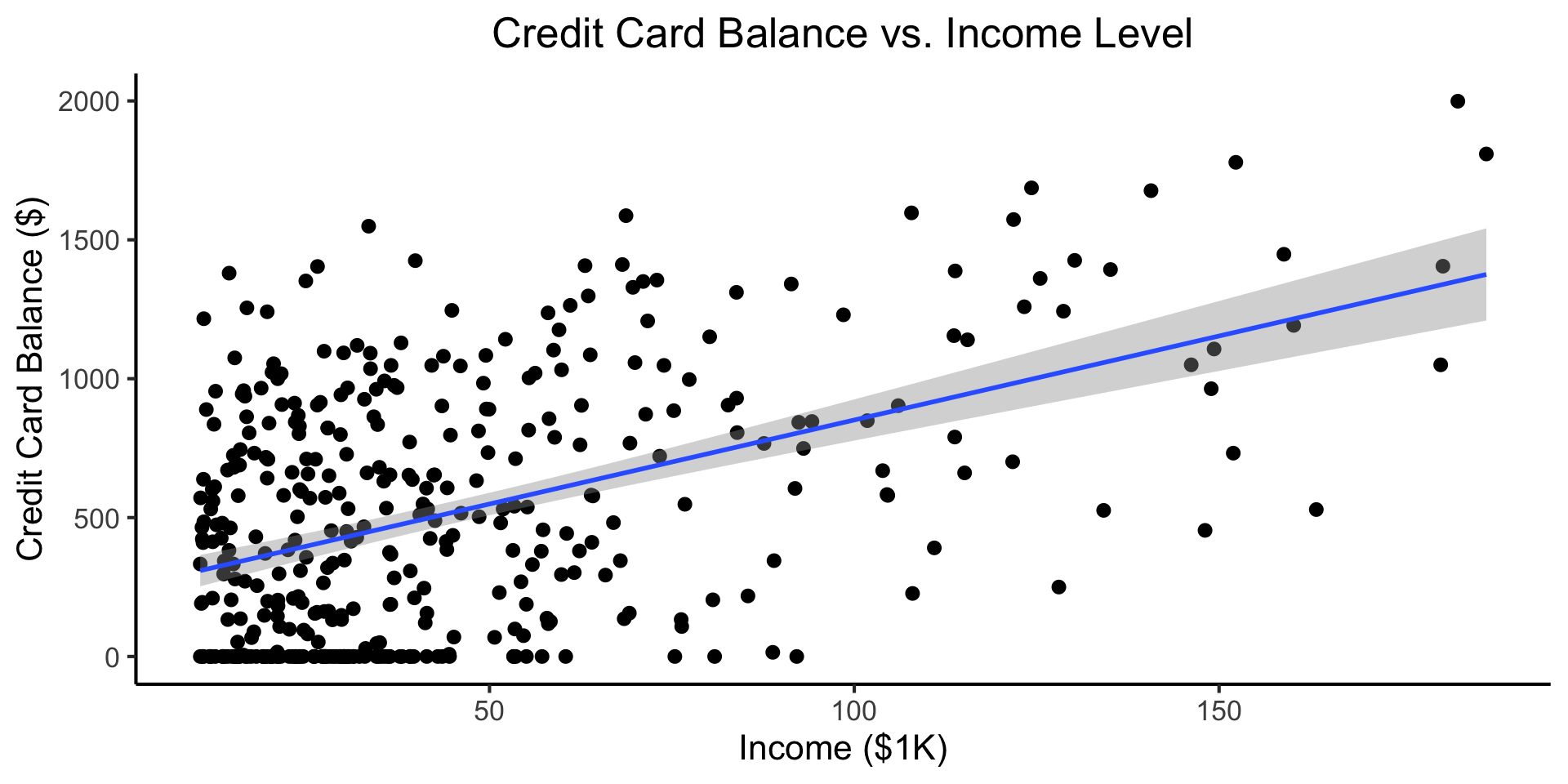

MLR Superpower: Handling Categorical Vars

\[ \begin{align*} Y &= \beta_0 + \beta_1 \times \texttt{income} \\ &\phantom{Y} \end{align*} \]

Code

credit_df <- read_csv("assets/Credit.csv")

credit_plot <- credit_df |> ggplot(aes(x=Income, y=Balance)) +

geom_point(size=0.5*g_pointsize) +

geom_smooth(

method='lm', formula="y ~ x", linewidth=1,

fullrange=TRUE

) +

theme_dsan() +

labs(

title="Credit Card Balance vs. Income Level",

x="Income ($1K)",

y="Credit Card Balance ($)"

)

credit_plot

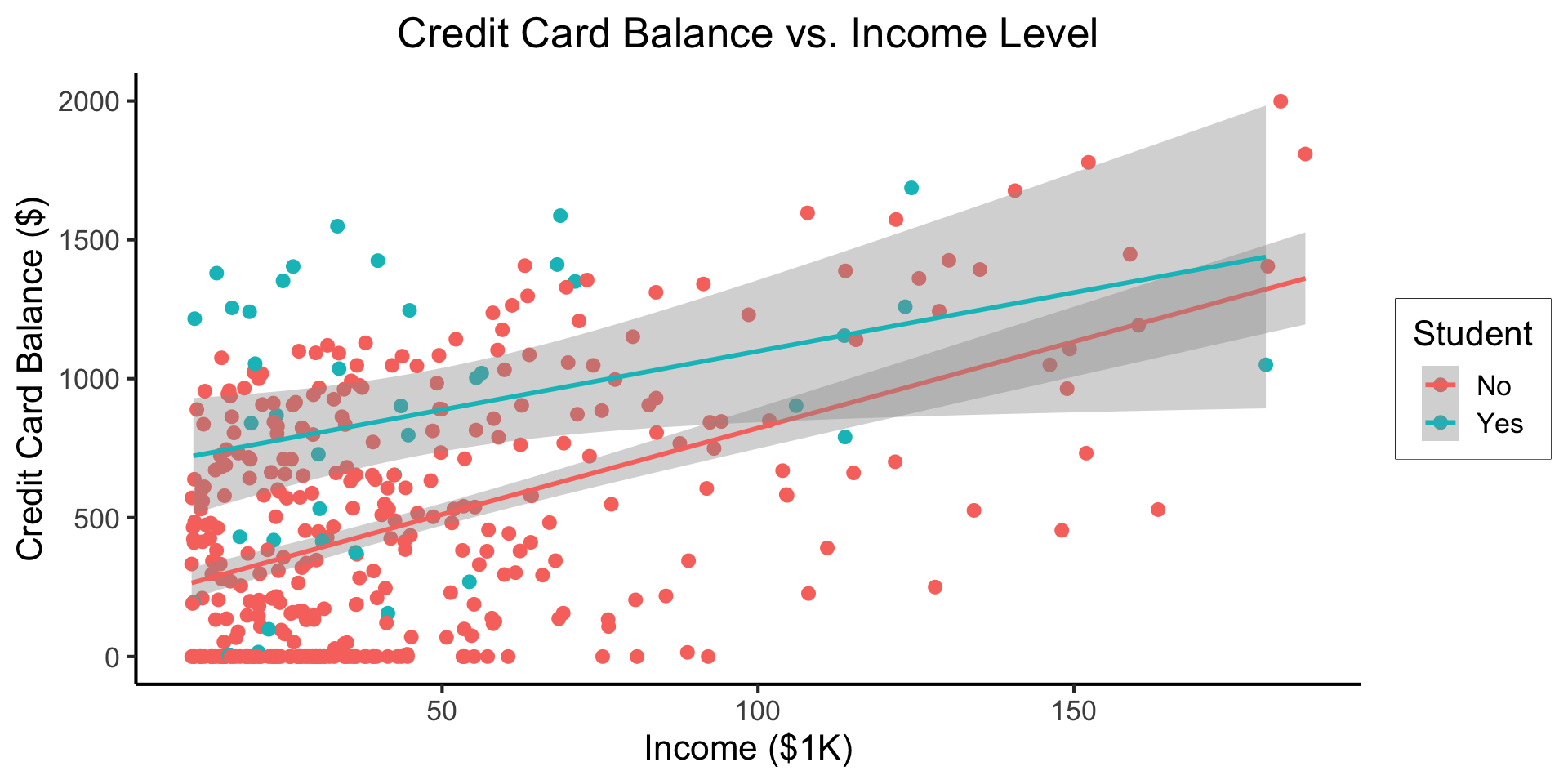

\[ \begin{align*} Y = &\beta_0 + \beta_1 \times \texttt{income} + \beta_2 \times \texttt{Student} \\ &+ \beta_3 \times (\texttt{Student} \times \texttt{Income}) \end{align*} \]

Code

student_plot <- credit_df |> ggplot(aes(x=Income, y=Balance, color=Student)) +

geom_point(size=0.5*g_pointsize) +

geom_smooth(

method='lm', formula="y ~ x", linewidth=1,

fullrange=TRUE

) +

theme_dsan() +

labs(

title="Credit Card Balance vs. Income Level",

x="Income ($1K)",

y="Credit Card Balance ($)"

)

student_plot

- Why do we need the \(\texttt{Student} \times \texttt{Income}\) term?

- Understanding this setup will open up a vast array of possibilities for regression 😎

- (Dear future Jeff, let’s go through this on the board! Sincerely, past Jeff)

From MLR to Logistic Regression

- As DSAN students, you know that we’re still sweeping classification under the rug!

- We saw how to include binary/multiclass covariates, but what if the actual thing we’re trying to predict is binary?

- The wrong approach is the “Linear Probability Model”:

\[ \Pr(Y \mid X) = \beta_0 + \beta_1 X + \varepsilon \]

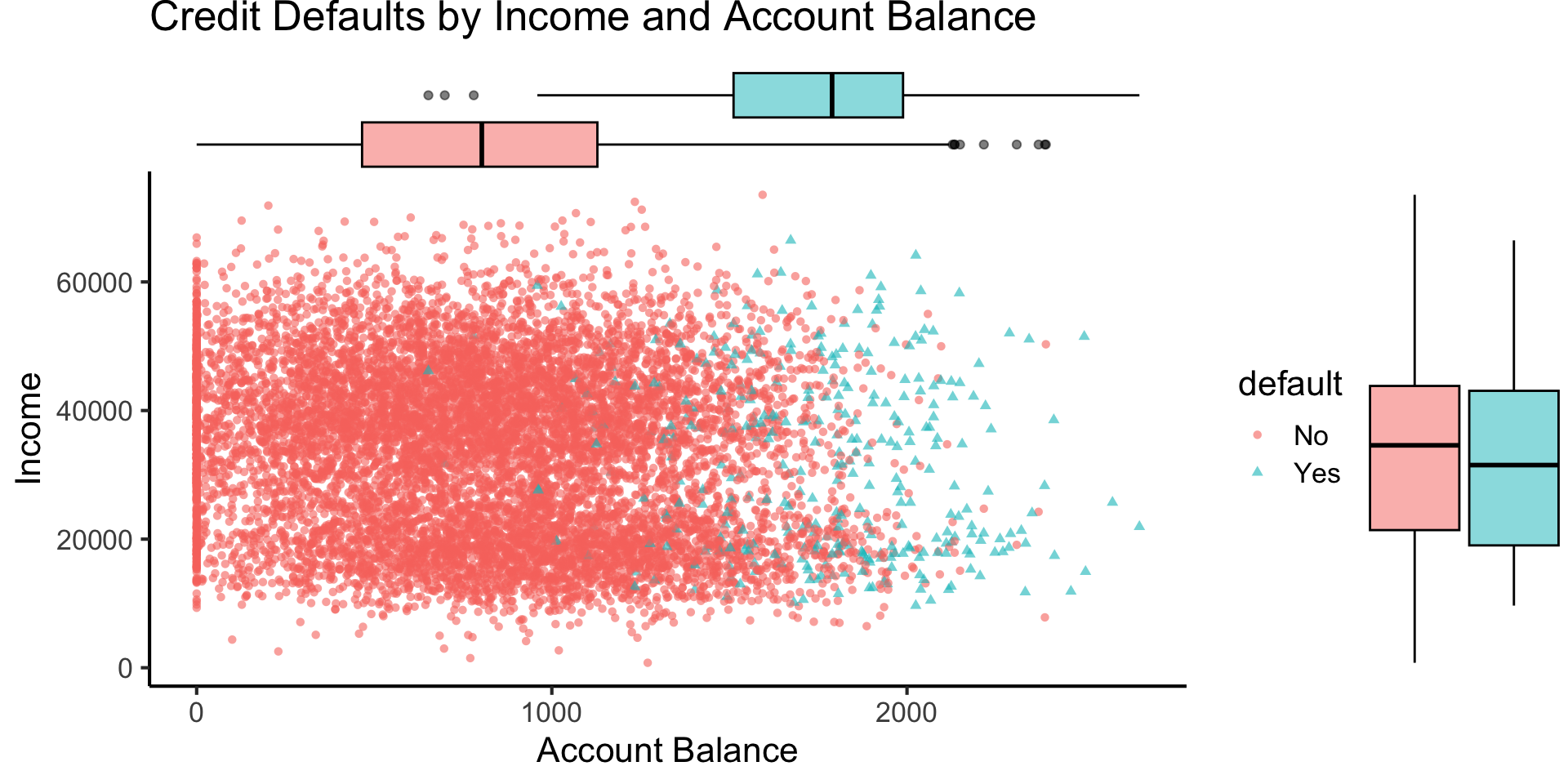

Credit Default

Code

library(tidyverse)

library(ggExtra)

default_df <- read_csv("assets/Default.csv") |>

mutate(default_num = ifelse(default=="Yes",1,0))

default_plot <- default_df |> ggplot(aes(x=balance, y=income, color=default, shape=default)) +

geom_point(alpha=0.6) +

theme_classic(base_size=16) +

labs(

title="Credit Defaults by Income and Account Balance",

x = "Account Balance",

y = "Income"

)

default_mplot <- default_plot |> ggMarginal(type="boxplot", groupColour=FALSE, groupFill=TRUE)

default_mplot

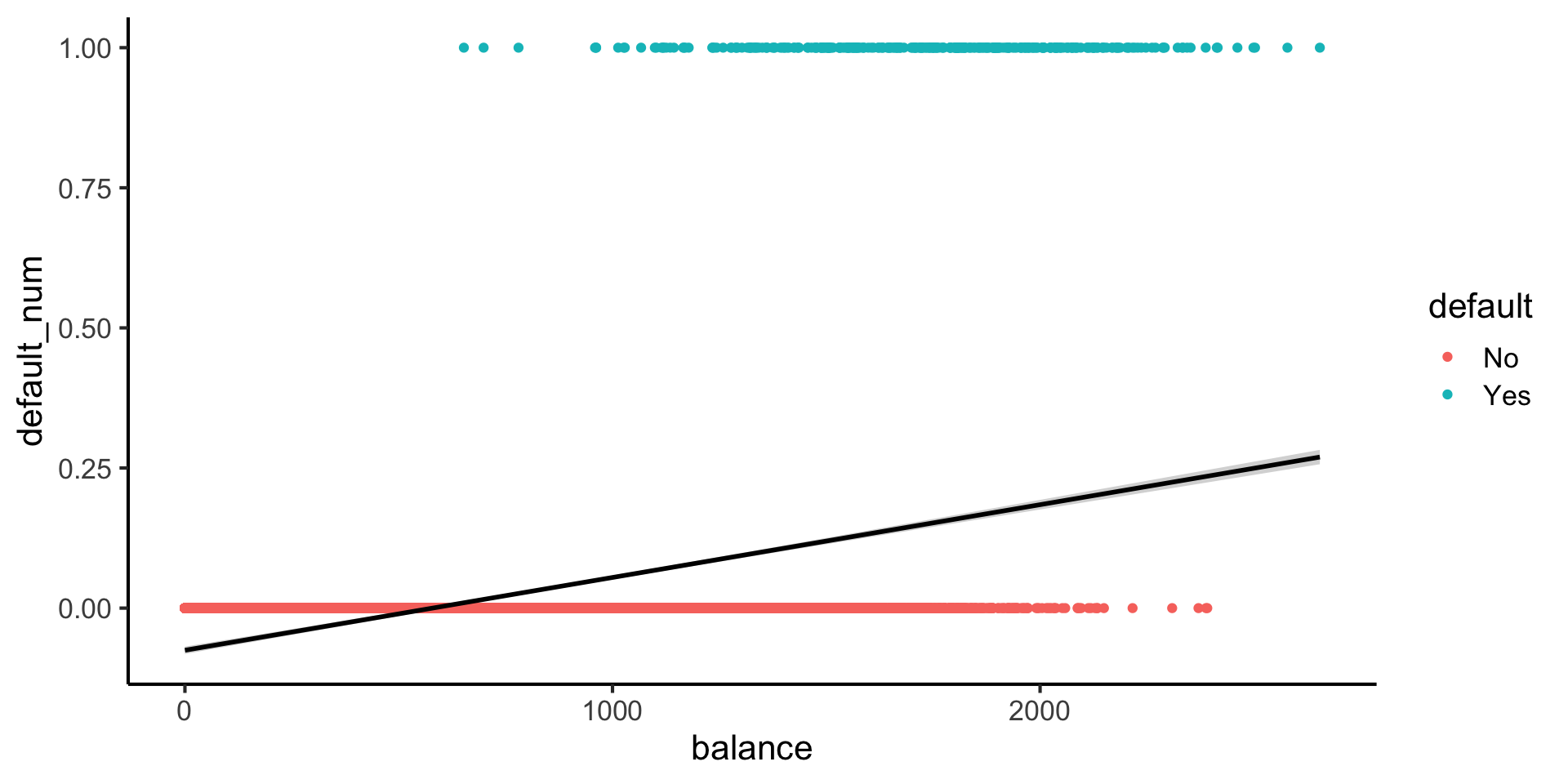

Lines vs. Sigmoids(!)

Here’s what lines look like for this dataset:

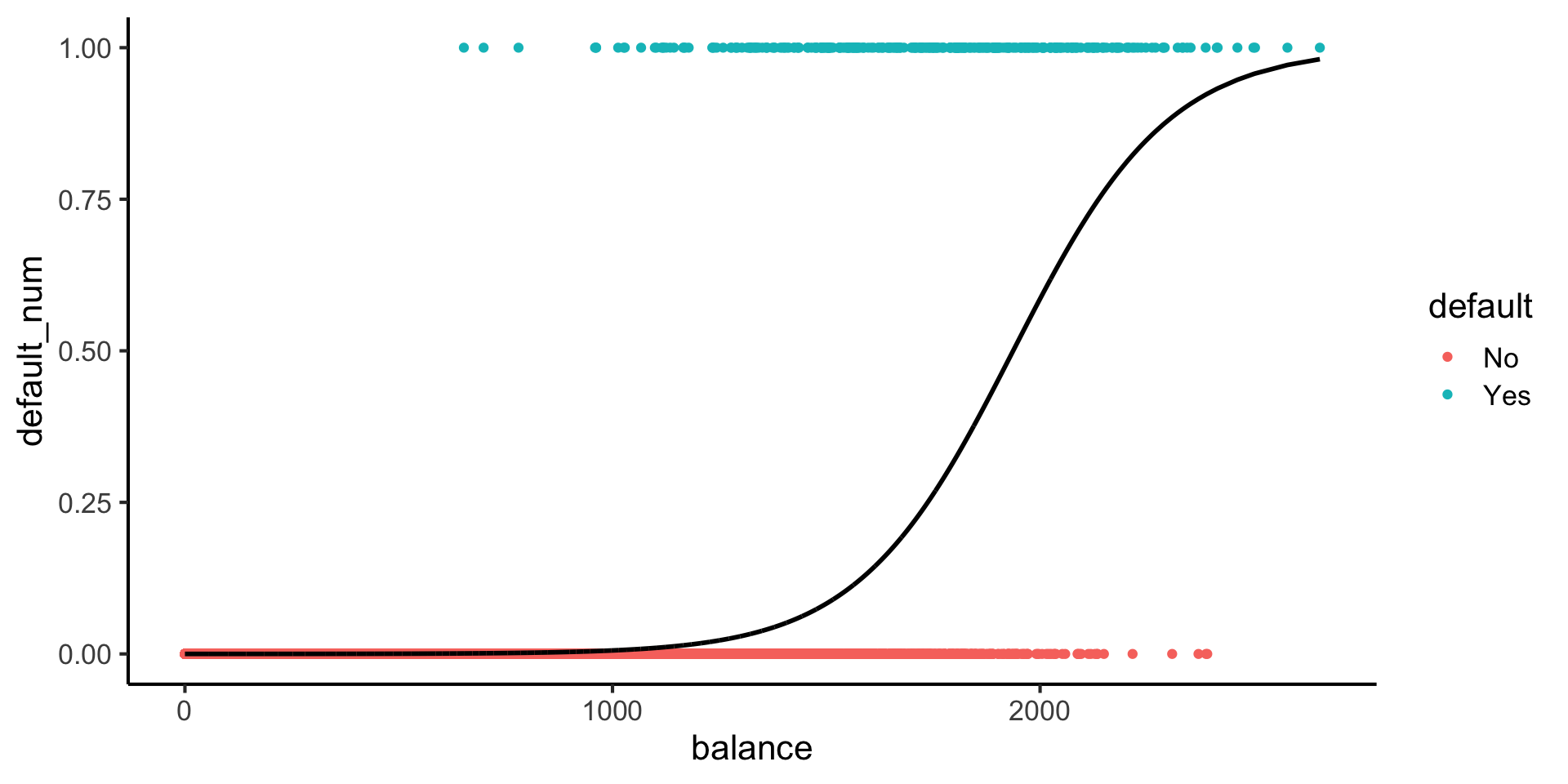

Here’s what sigmoids look like:

Code

library(tidyverse)

logistic_model <- glm(default_num ~ balance, family=binomial(link='logit'),data=default_df)

default_df$predictions <- predict(logistic_model, newdata = default_df, type = "response")

my_sigmoid <- function(x) 1 / (1+exp(-x))

default_df |> ggplot(aes(x=balance, y=default_num)) +

#stat_function(fun=my_sigmoid) +

geom_point(aes(color=default)) +

geom_line(

data=default_df,

aes(x=balance, y=predictions),

linewidth=1

) +

theme_classic(base_size=16)

\[ \Pr(Y \mid X) = \beta_0 + \beta_1 X + \varepsilon \]

\[ \log\underbrace{\left[ \frac{\Pr(Y \mid X)}{1 - \Pr(Y \mid X)} \right]}_{\mathclap{\smash{\text{Odds Ratio}}}} = \beta_0 + \beta_1 X + \varepsilon \]