Code

source("../dsan-globals/_globals.r")

set.seed(5300)DSAN 5300: Statistical Learning

Spring 2026, Georgetown University

Today’s Planned Schedule:

| Start | End | Topic | |

|---|---|---|---|

| Lecture | 6:30pm | 7:10pm | Simple Linear Regression → |

| 7:10pm | 7:30pm | Deriving the OLS Solution → | |

| 7:30pm | 8:00pm | Interpreting OLS Output → | |

| Break! | 8:00pm | 8:10pm | |

| 8:10pm | 8:30pm | Quiz Review → | |

| 8:30pm | 9:00pm | Quiz 2! |

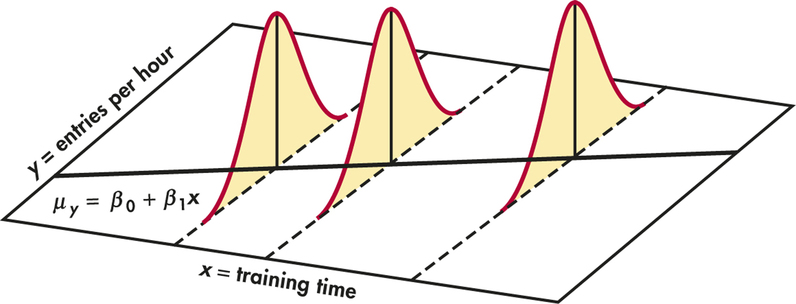

What happens to my dependent variable \(Y\) when my independent variable \(X\) increases by 1 unit?

Keep the goal in front of your mind:

source("../dsan-globals/_globals.r")

set.seed(5300)\[ \DeclareMathOperator*{\argmax}{argmax} \DeclareMathOperator*{\argmin}{argmin} \newcommand{\bigexp}[1]{\exp\mkern-4mu\left[ #1 \right]} \newcommand{\bigexpect}[1]{\mathbb{E}\mkern-4mu \left[ #1 \right]} \newcommand{\definedas}{\overset{\small\text{def}}{=}} \newcommand{\definedalign}{\overset{\phantom{\text{defn}}}{=}} \newcommand{\eqeventual}{\overset{\text{eventually}}{=}} \newcommand{\Err}{\text{Err}} \newcommand{\expect}[1]{\mathbb{E}[#1]} \newcommand{\expectsq}[1]{\mathbb{E}^2[#1]} \newcommand{\fw}[1]{\texttt{#1}} \newcommand{\given}{\mid} \newcommand{\green}[1]{\color{green}{#1}} \newcommand{\heads}{\outcome{heads}} \newcommand{\iid}{\overset{\text{\small{iid}}}{\sim}} \newcommand{\lik}{\mathcal{L}} \newcommand{\loglik}{\ell} \DeclareMathOperator*{\maximize}{maximize} \DeclareMathOperator*{\minimize}{minimize} \newcommand{\mle}{\textsf{ML}} \newcommand{\nimplies}{\;\not\!\!\!\!\implies} \newcommand{\orange}[1]{\color{orange}{#1}} \newcommand{\outcome}[1]{\textsf{#1}} \newcommand{\param}[1]{{\color{purple} #1}} \newcommand{\pgsamplespace}{\{\green{1},\green{2},\green{3},\purp{4},\purp{5},\purp{6}\}} \newcommand{\pedge}[2]{\require{enclose}\enclose{circle}{~{#1}~} \rightarrow \; \enclose{circle}{\kern.01em {#2}~\kern.01em}} \newcommand{\pnode}[1]{\require{enclose}\enclose{circle}{\kern.1em {#1} \kern.1em}} \newcommand{\ponode}[1]{\require{enclose}\enclose{box}[background=lightgray]{{#1}}} \newcommand{\pnodesp}[1]{\require{enclose}\enclose{circle}{~{#1}~}} \newcommand{\purp}[1]{\color{purple}{#1}} \newcommand{\sign}{\text{Sign}} \newcommand{\spacecap}{\; \cap \;} \newcommand{\spacewedge}{\; \wedge \;} \newcommand{\tails}{\outcome{tails}} \newcommand{\Var}[1]{\text{Var}[#1]} \newcommand{\bigVar}[1]{\text{Var}\mkern-4mu \left[ #1 \right]} \]

library(tidyverse)

set.seed(5321)

N <- 11

x <- seq(from = 0, to = 1, by = 1 / (N - 1))

y <- x + rnorm(N, 0, 0.2)

mean_y <- mean(y)

spread <- y - mean_y

df <- tibble(x = x, y = y, spread = spread)

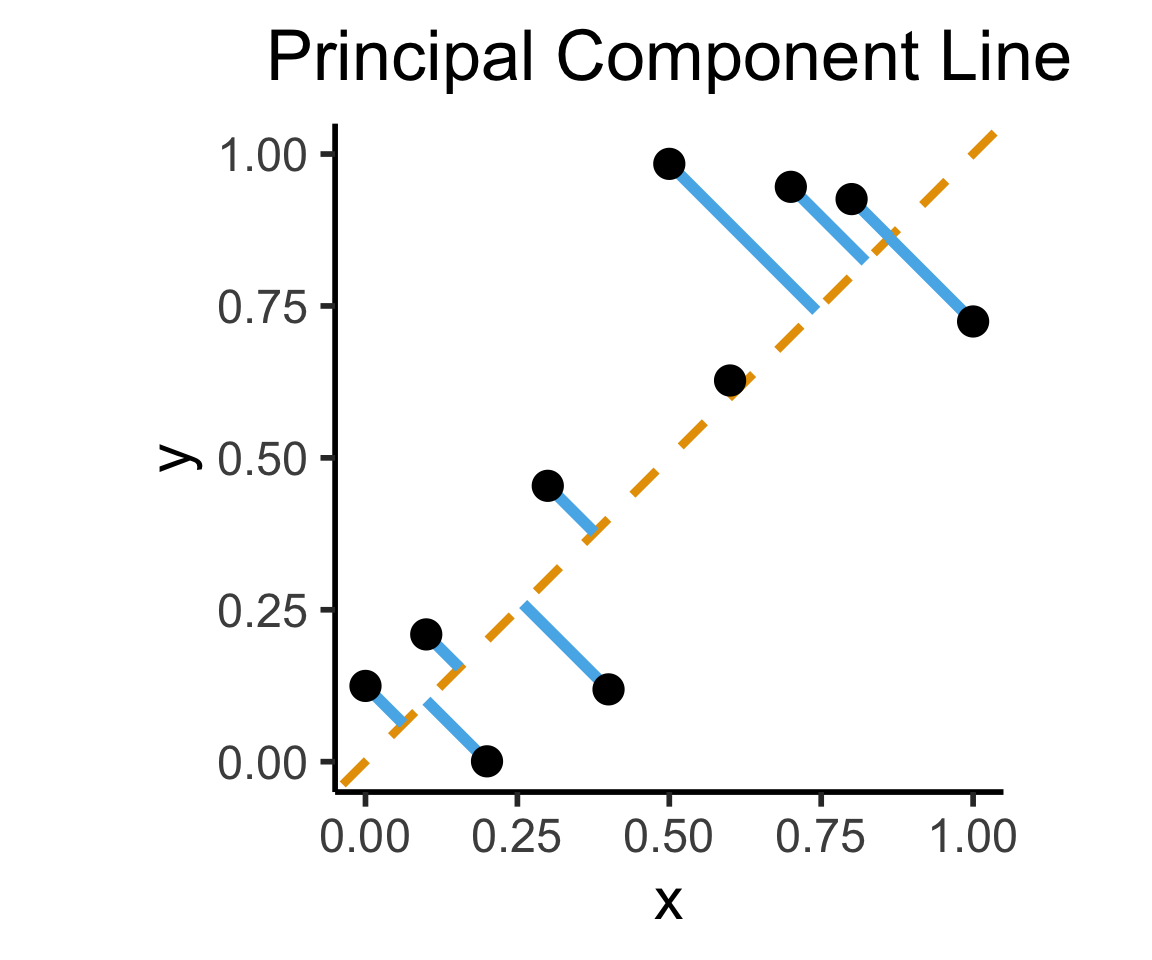

ggplot(df, aes(x=x, y=y)) +

geom_abline(slope=1, intercept=0, linetype="dashed", color=cbPalette[1], linewidth=g_linewidth*1.5) +

geom_segment(xend=(x+y)/2, yend=(x+y)/2, linewidth=g_linewidth*2, color=cbPalette[2]) +

geom_point(size=g_pointsize) +

coord_equal() +

xlim(0, 1) + ylim(0, 1) +

dsan_theme("half") +

labs(

title = "Principal Component Line"

)

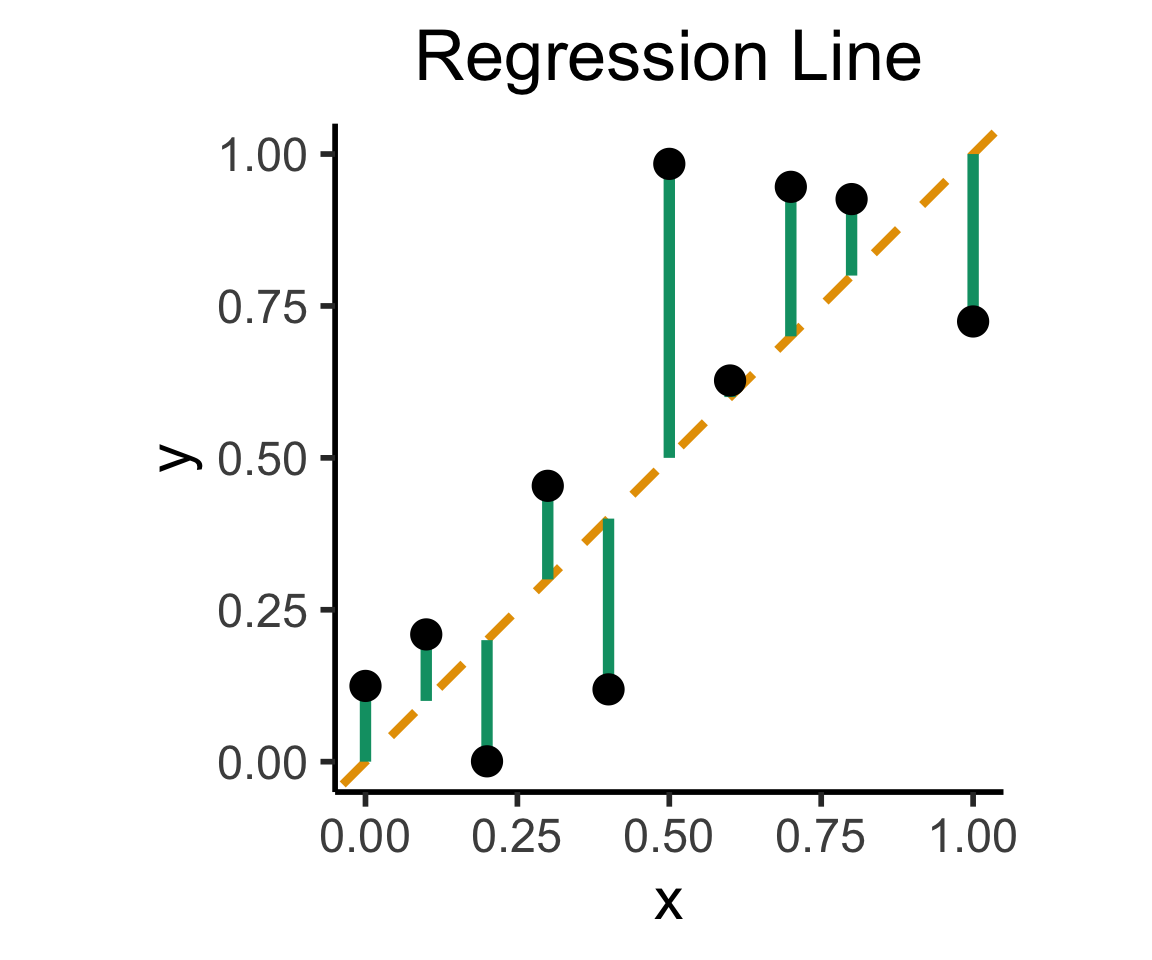

ggplot(df, aes(x=x, y=y)) +

geom_abline(slope=1, intercept=0, linetype="dashed", color=cbPalette[1], linewidth=g_linewidth*1.5) +

geom_segment(xend=x, yend=x, linewidth=g_linewidth*2, color=cb_palette[3]) +

geom_point(size=g_pointsize) +

coord_equal() +

xlim(0, 1) + ylim(0, 1) +

dsan_theme("half") +

labs(

title = "Regression Line"

)

On the difference between these two lines, and why it matters, I cannot recommend Gelman and Hill (2007) enough!

library(readr)

library(ggplot2)

gdp_df <- read_csv("assets/gdp_pca.csv")

dist_to_line <- function(x0, y0, a, c) {

numer <- abs(a * x0 - y0 + c)

denom <- sqrt(a * a + 1)

return(numer / denom)

}

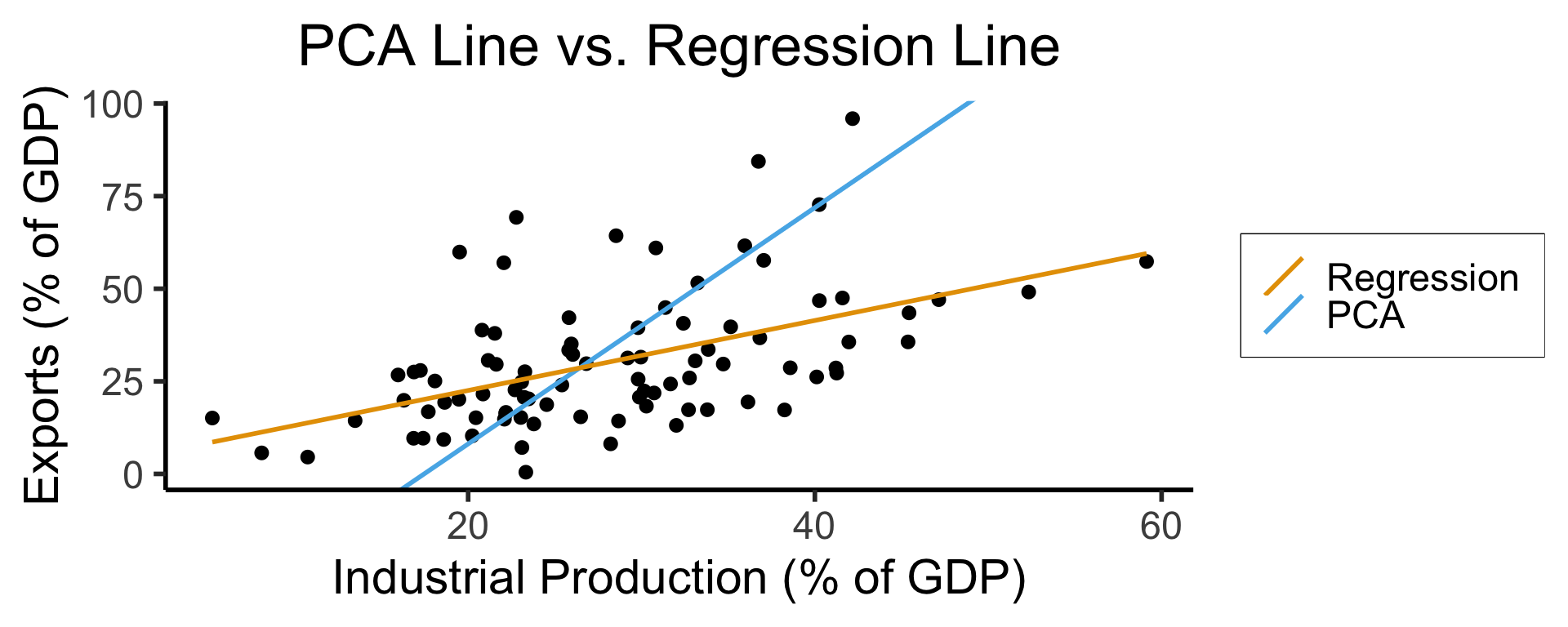

# Finding PCA line for industrial vs. exports

x <- gdp_df$industrial

y <- gdp_df$exports

lossFn <- function(lineParams, x0, y0) {

a <- lineParams[1]

c <- lineParams[2]

return(sum(dist_to_line(x0, y0, a, c)))

}

o <- optim(c(0, 0), lossFn, x0 = x, y0 = y)

ggplot(gdp_df, aes(x = industrial, y = exports)) +

geom_point(size=g_pointsize/2) +

geom_abline(aes(slope = o$par[1], intercept = o$par[2], color="pca"), linewidth=g_linewidth, show.legend = TRUE) +

geom_smooth(aes(color="lm"), method = "lm", se = FALSE, linewidth=g_linewidth, key_glyph = "blank") +

scale_color_manual(element_blank(), values=c("pca"=cbPalette[2],"lm"=cbPalette[1]), labels=c("Regression","PCA")) +

dsan_theme("half") +

remove_legend_title() +

labs(

title = "PCA Line vs. Regression Line",

x = "Industrial Production (% of GDP)",

y = "Exports (% of GDP)"

)

See this amazing blog post using PCA, with 2 dimensions, to explore UN voting patterns!

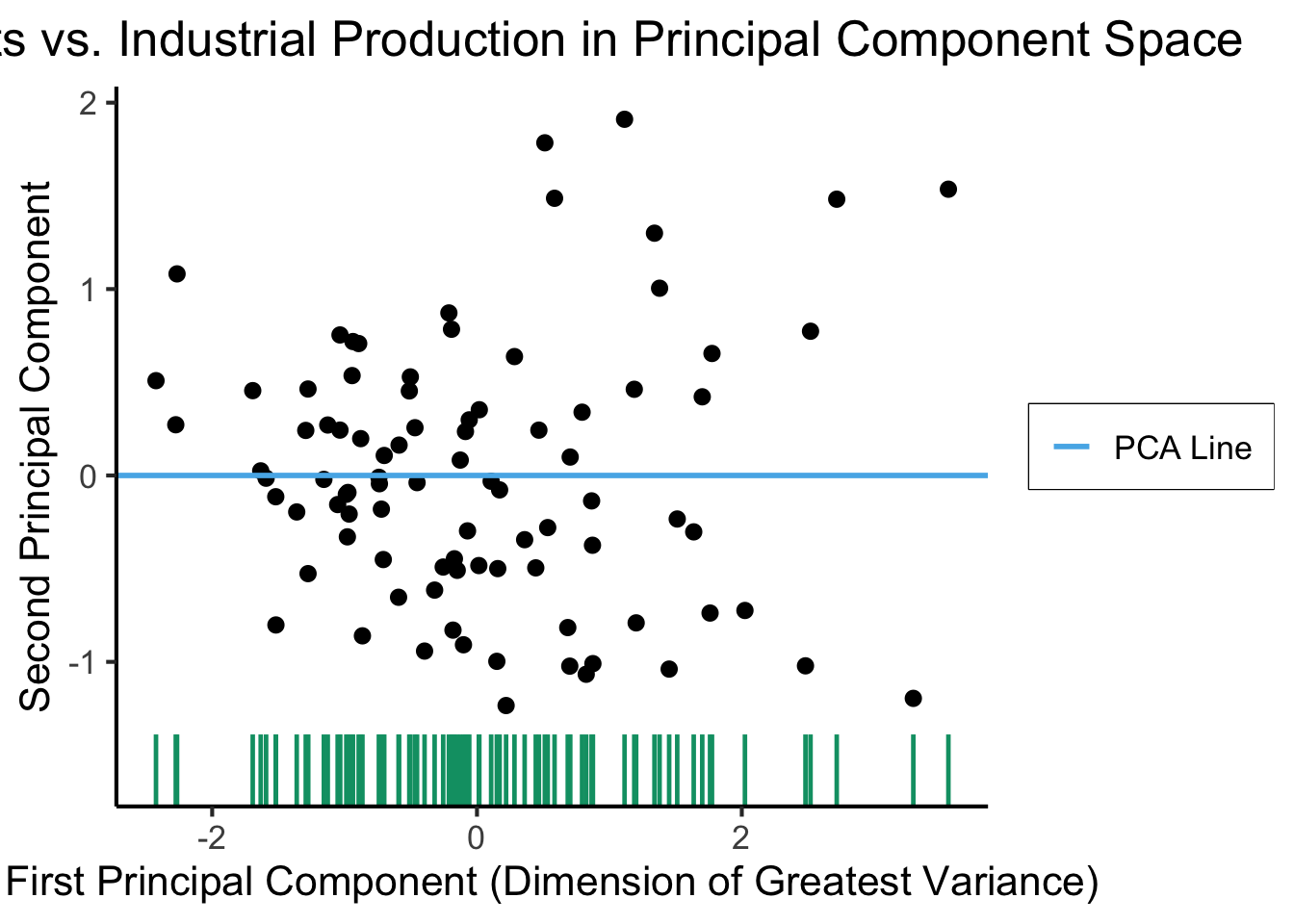

ggplot(gdp_df, aes(pc1, .fittedPC2)) +

geom_point(size = g_pointsize/2) +

geom_hline(aes(yintercept=0, color='PCA Line'), linetype='solid', size=g_linesize) +

geom_rug(sides = "b", linewidth=g_linewidth/1.2, length = unit(0.1, "npc"), color=cbPalette[3]) +

expand_limits(y=-1.6) +

scale_color_manual(element_blank(), values=c("PCA Line"=cbPalette[2])) +

dsan_theme("full") +

remove_legend_title() +

labs(

title = "Exports vs. Industrial Production in Principal Component Space",

x = "First Principal Component (Dimension of Greatest Variance)",

y = "Second Principal Component"

)

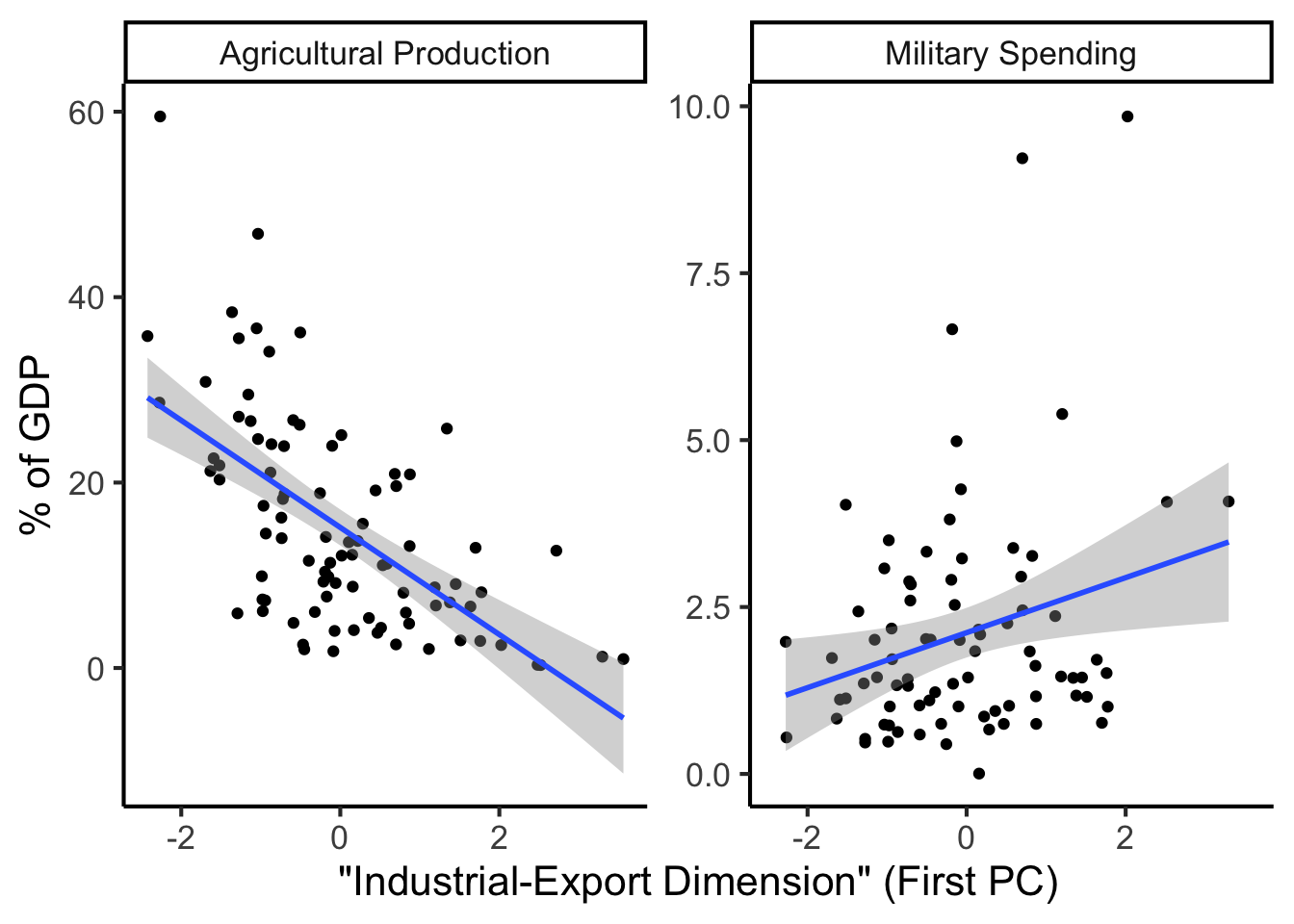

library(dplyr)

library(tidyr)

plot_df <- gdp_df %>% select(c(country_code, pc1, agriculture, military))

long_df <- plot_df %>% pivot_longer(!c(country_code, pc1), names_to = "var", values_to = "val")

long_df <- long_df |> mutate(

var = case_match(

var,

"agriculture" ~ "Agricultural Production",

"military" ~ "Military Spending"

)

)

ggplot(long_df, aes(x = pc1, y = val, facet = var)) +

geom_point() +

geom_smooth(method=lm, formula='y ~ x') +

facet_wrap(vars(var), scales = "free") +

dsan_theme("full") +

labs(

x = "\"Industrial-Export Dimension\" (First PC)",

y = "% of GDP"

)

Given data \((X, Y)\), we estimate \(\widehat{y} = \widehat{\beta}_0 + \widehat{\beta}_1x\), hypothesizing that:

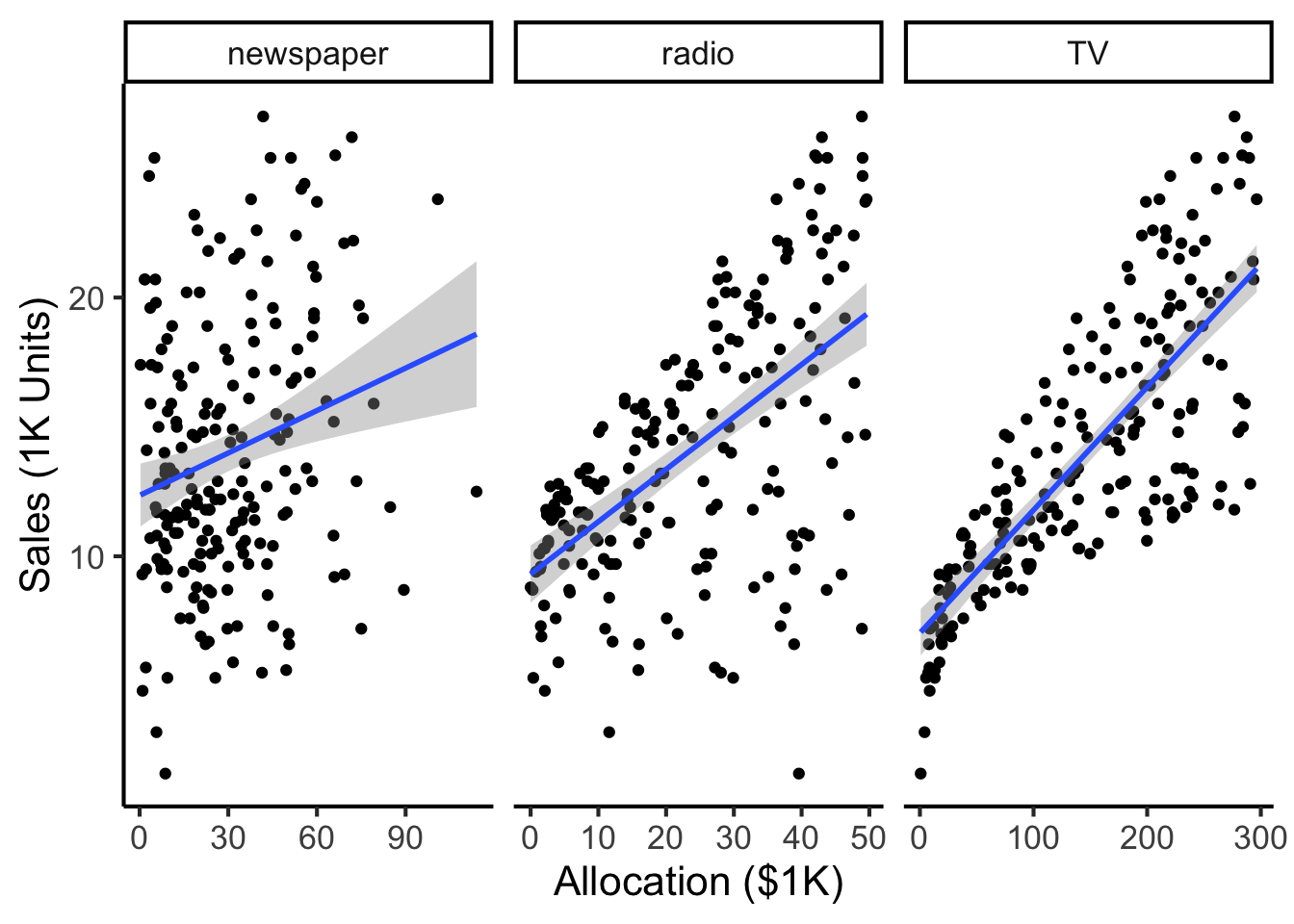

library(tidyverse)

ad_df <- read_csv("assets/Advertising.csv") |> rename(id=`...1`)

long_df <- ad_df |> pivot_longer(-c(id, sales), names_to="medium", values_to="allocation")

long_df |> ggplot(aes(x=allocation, y=sales)) +

geom_point() +

facet_wrap(vars(medium), scales="free_x") +

geom_smooth(method='lm', formula="y ~ x") +

theme_dsan() +

labs(

x = "Allocation ($1K)",

y = "Sales (1K Units)"

)

Our model:

\[ Y = \underbrace{\param{\beta_0}}_{\mathclap{\text{Intercept}}} + \underbrace{\param{\beta_1}}_{\mathclap{\text{Slope}}}X + \varepsilon \]

…Generates predictions via:

\[ \widehat{y} = \underbrace{\widehat{\beta}_0}_{\mathclap{\small\begin{array}{c}\text{Estimated} \\[-5mm] \text{intercept}\end{array}}} ~+~ \underbrace{\widehat{\beta}_1}_{\mathclap{\small\begin{array}{c}\text{Estimated} \\[-4mm] \text{slope}\end{array}}}\cdot x \]

\[ \widehat{\varepsilon}_i = \underbrace{y_i}_{\mathclap{\small\begin{array}{c}\text{Real} \\[-5mm] \text{label}\end{array}}} - \underbrace{\widehat{y}_i}_{\mathclap{\small\begin{array}{c}\text{Predicted} \\[-5mm] \text{label}\end{array}}} = \underbrace{y_i}_{\mathclap{\small\begin{array}{c}\text{Real} \\[-5mm] \text{label}\end{array}}} - \underbrace{ \left( \widehat{\beta}_0 + \widehat{\beta}_1 \cdot x \right) }_{\text{\small{Predicted label}}} \]

What can we optimize to ensure these residuals are as small as possible?

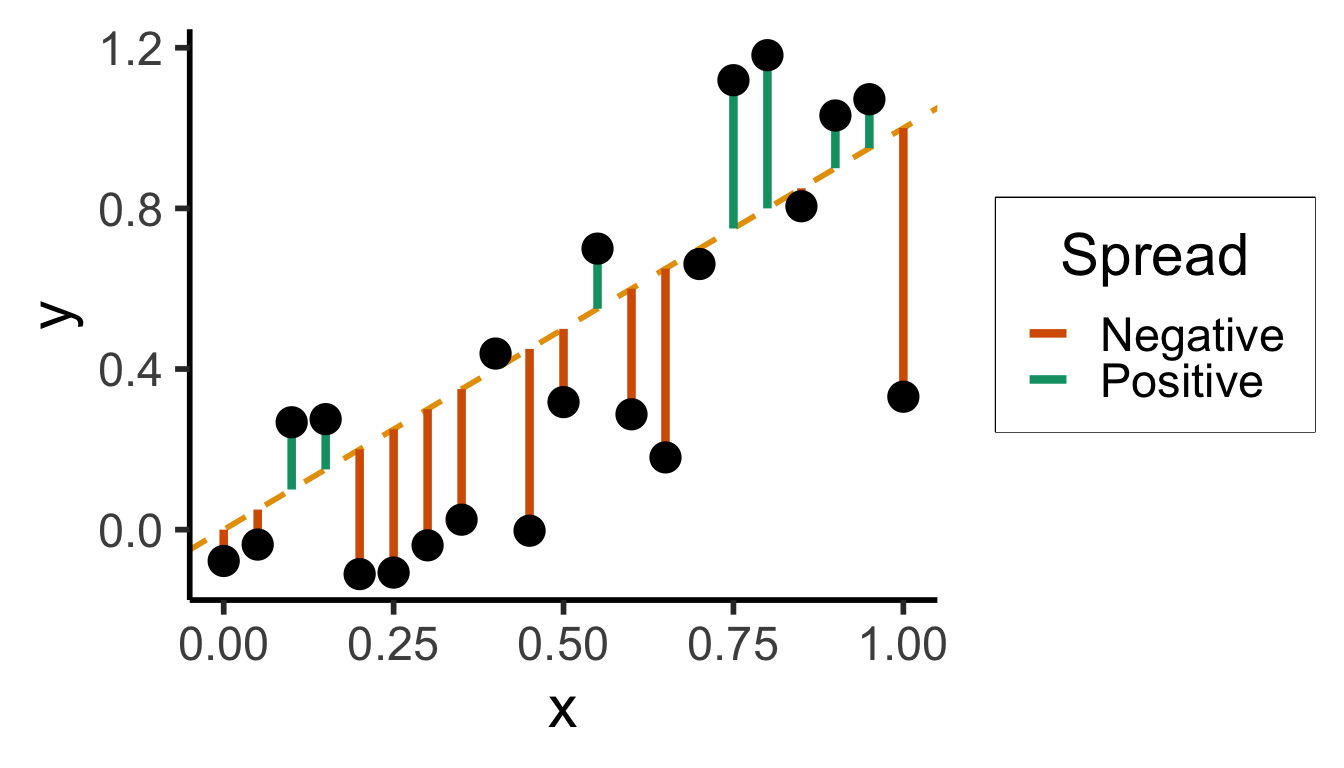

N <- 21

x <- seq(from = 0, to = 1, by = 1 / (N - 1))

y <- x + rnorm(N, 0, 0.25)

mean_y <- mean(y)

spread <- y - mean_y

sim_lg_df <- tibble(x = x, y = y, spread = spread)

sim_lg_df |> ggplot(aes(x=x, y=y)) +

geom_abline(slope=1, intercept=0, linetype="dashed", color=cbPalette[1], linewidth=g_linewidth) +

# geom_segment(xend=x, yend=x, linewidth=g_linewidth*2, color=cbPalette[2]) +

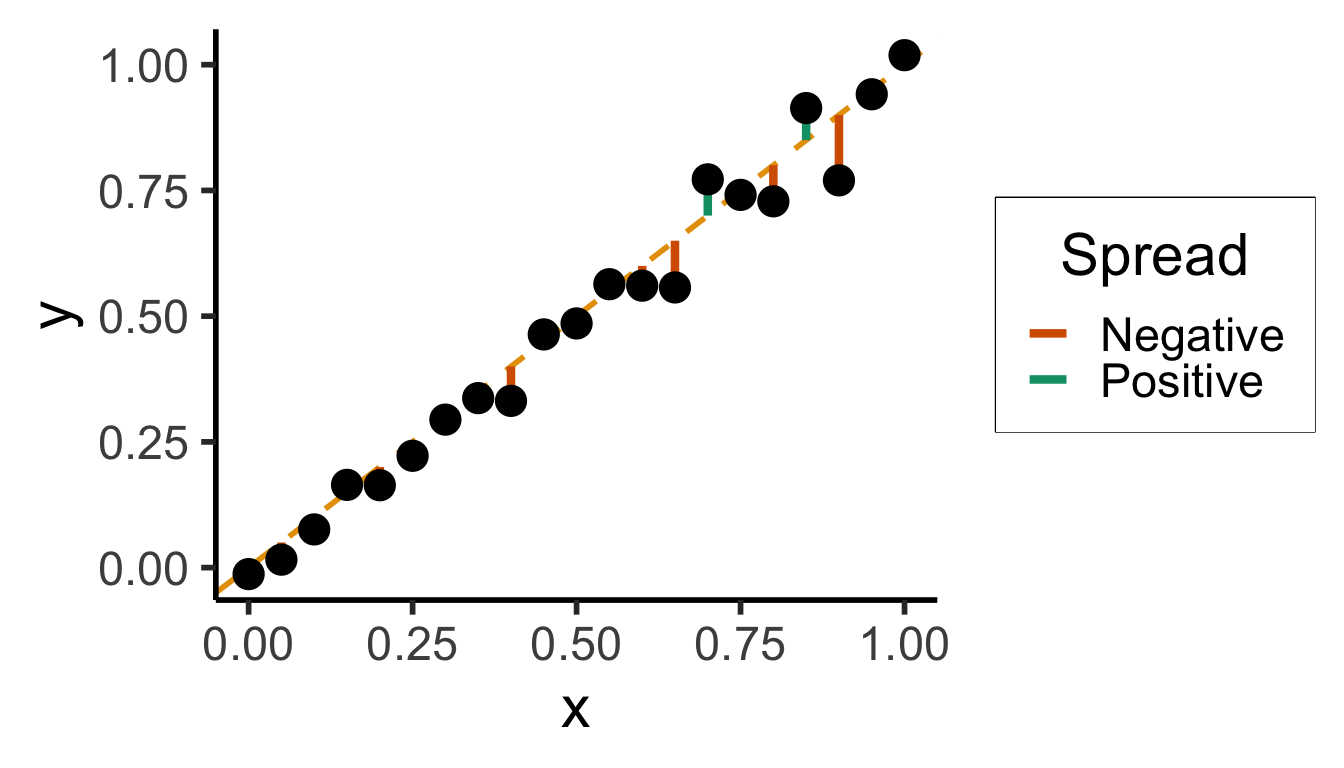

geom_segment(aes(xend=x, yend=x, color=ifelse(y>x,"Positive","Negative")), linewidth=1.5*g_linewidth) +

geom_point(size=g_pointsize) +

# coord_equal() +

theme_dsan("half") +

scale_color_manual("Spread", values=c("Positive"=cbPalette[3],"Negative"=cbPalette[6]), labels=c("Positive"="Positive","Negative"="Negative"))

large_sum <- sum(sim_lg_df$spread)

writeLines(fmt_decimal(large_sum))

large_sqsum <- sum((sim_lg_df$spread)^2)

writeLines(fmt_decimal(large_sqsum))

large_abssum <- sum(abs(sim_lg_df$spread))

writeLines(fmt_decimal(large_abssum))

Sum?

0.0000000000Sum of Squares?

3.8405017200Sum of absolute vals?

7.6806094387N <- 21

x <- seq(from = 0, to = 1, by = 1 / (N - 1))

y <- x + rnorm(N, 0, 0.05)

mean_y <- mean(y)

spread <- y - mean_y

sim_sm_df <- tibble(x = x, y = y, spread = spread)

sim_sm_df |> ggplot(aes(x=x, y=y)) +

geom_abline(slope=1, intercept=0, linetype="dashed", color=cbPalette[1], linewidth=g_linewidth) +

# geom_segment(xend=x, yend=x, linewidth=g_linewidth*2, color=cbPalette[2]) +

geom_segment(aes(xend=x, yend=x, color=ifelse(y>x,"Positive","Negative")), linewidth=1.5*g_linewidth) +

geom_point(size=g_pointsize) +

# coord_equal() +

theme_dsan("half") +

scale_color_manual("Spread", values=c("Positive"=cbPalette[3],"Negative"=cbPalette[6]), labels=c("Positive"="Positive","Negative"="Negative"))

small_rsum <- sum(sim_sm_df$spread)

writeLines(fmt_decimal(small_rsum))

small_sqrsum <- sum((sim_sm_df$spread)^2)

writeLines(fmt_decimal(small_sqrsum))

small_abssum <- sum(abs(sim_sm_df$spread))

writeLines(fmt_decimal(small_abssum))

Sum?

0.0000000000Sum of Squares?

1.9748635217Sum of absolute vals?

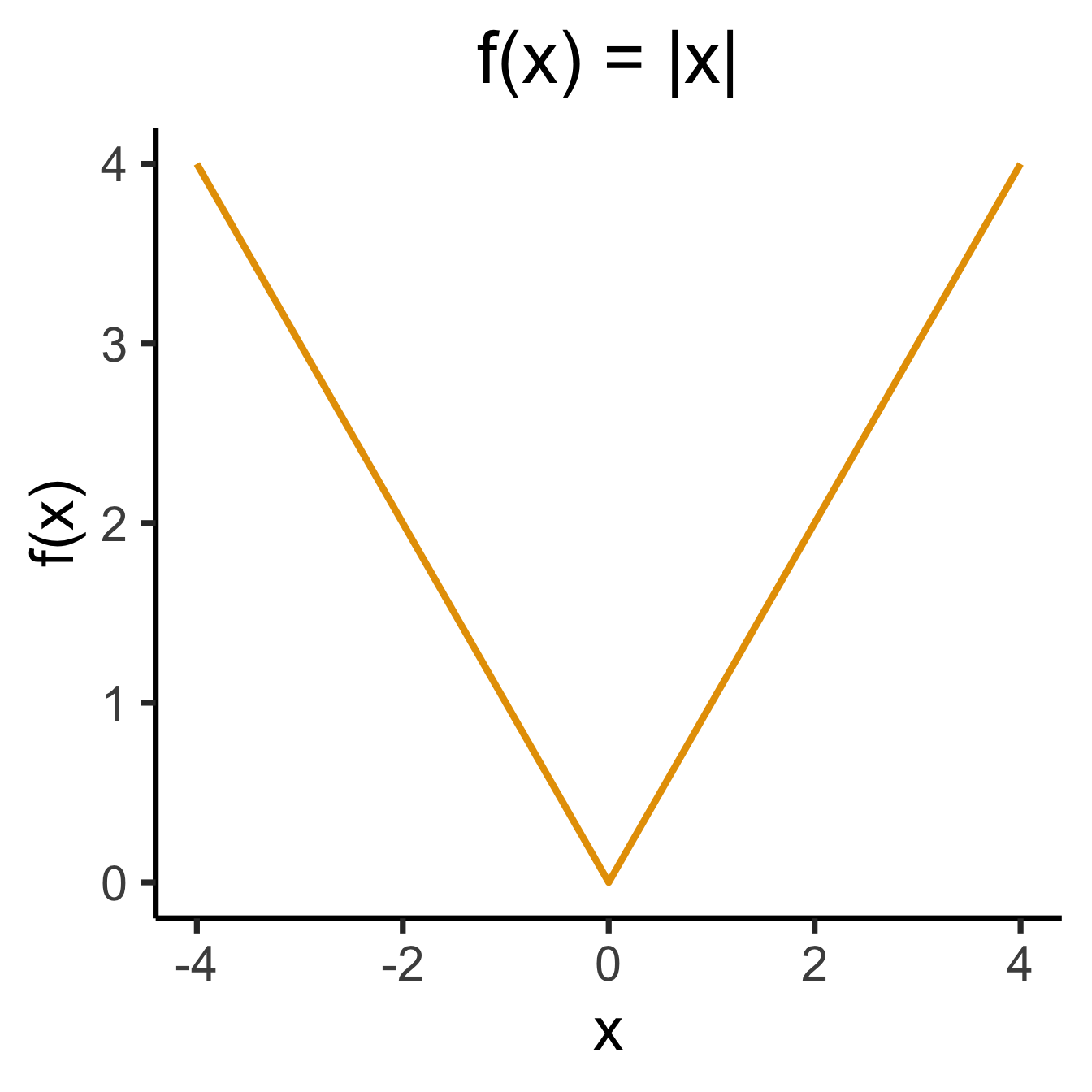

5.5149697440# Could use facet_grid() here, but it doesn't work too nicely with stat_function() :(

ggplot(data.frame(x=c(-4,4)), aes(x=x)) +

stat_function(

fun =~ abs(.x),

linewidth=g_linewidth * 1.5,

color=cb_palette[1],

) +

dsan_theme("quarter") +

labs(

title="f(x) = |x|",

y="f(x)"

)

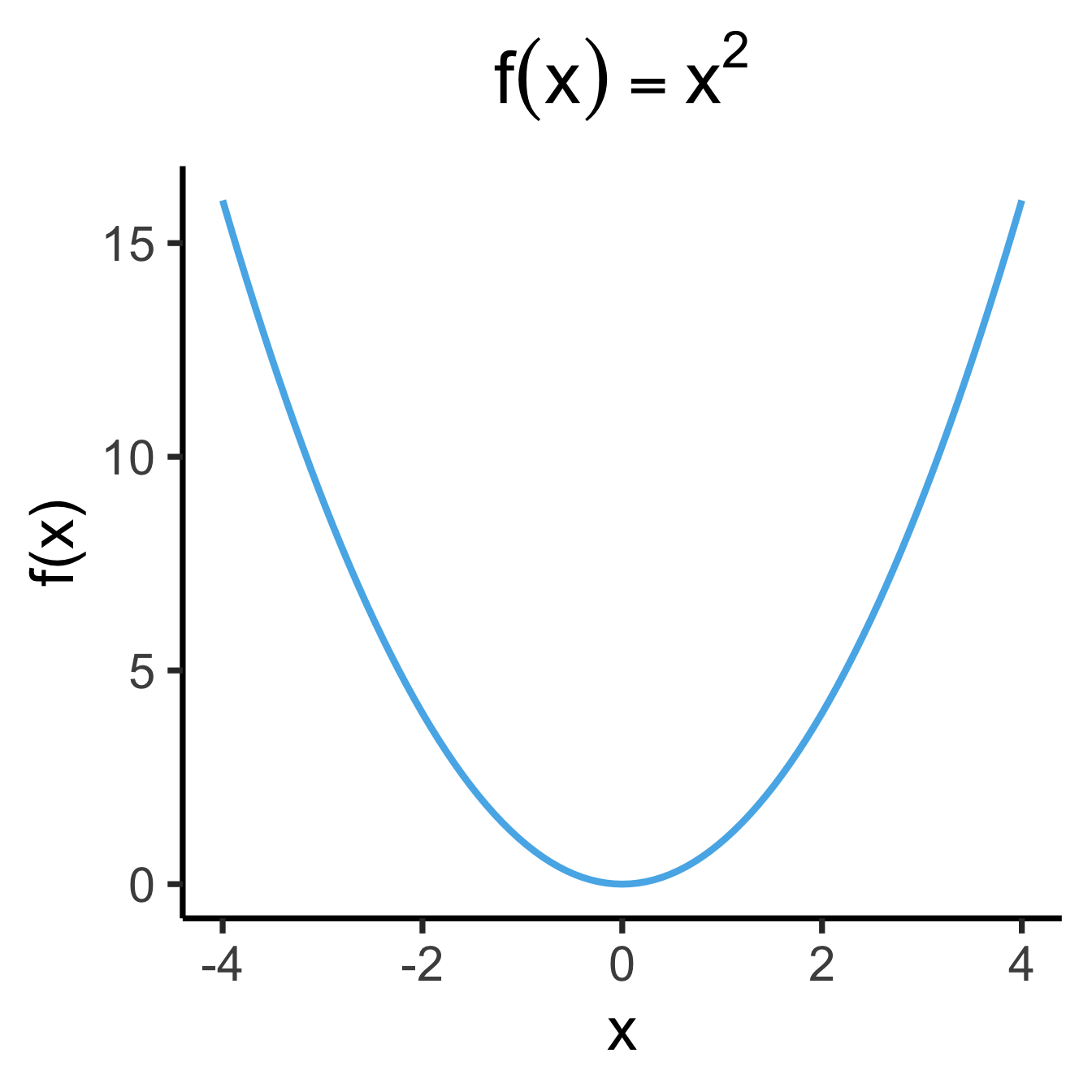

library(latex2exp)

x2_label <- TeX("$f(x) = x^2$")

ggplot(data.frame(x=c(-4,4)), aes(x=x)) +

stat_function(

fun =~ .x^2,

linewidth = g_linewidth * 1.5,

color=cb_palette[2],

) +

dsan_theme("quarter") +

labs(

title=x2_label,

y="f(x)"

)

library(latex2exp)

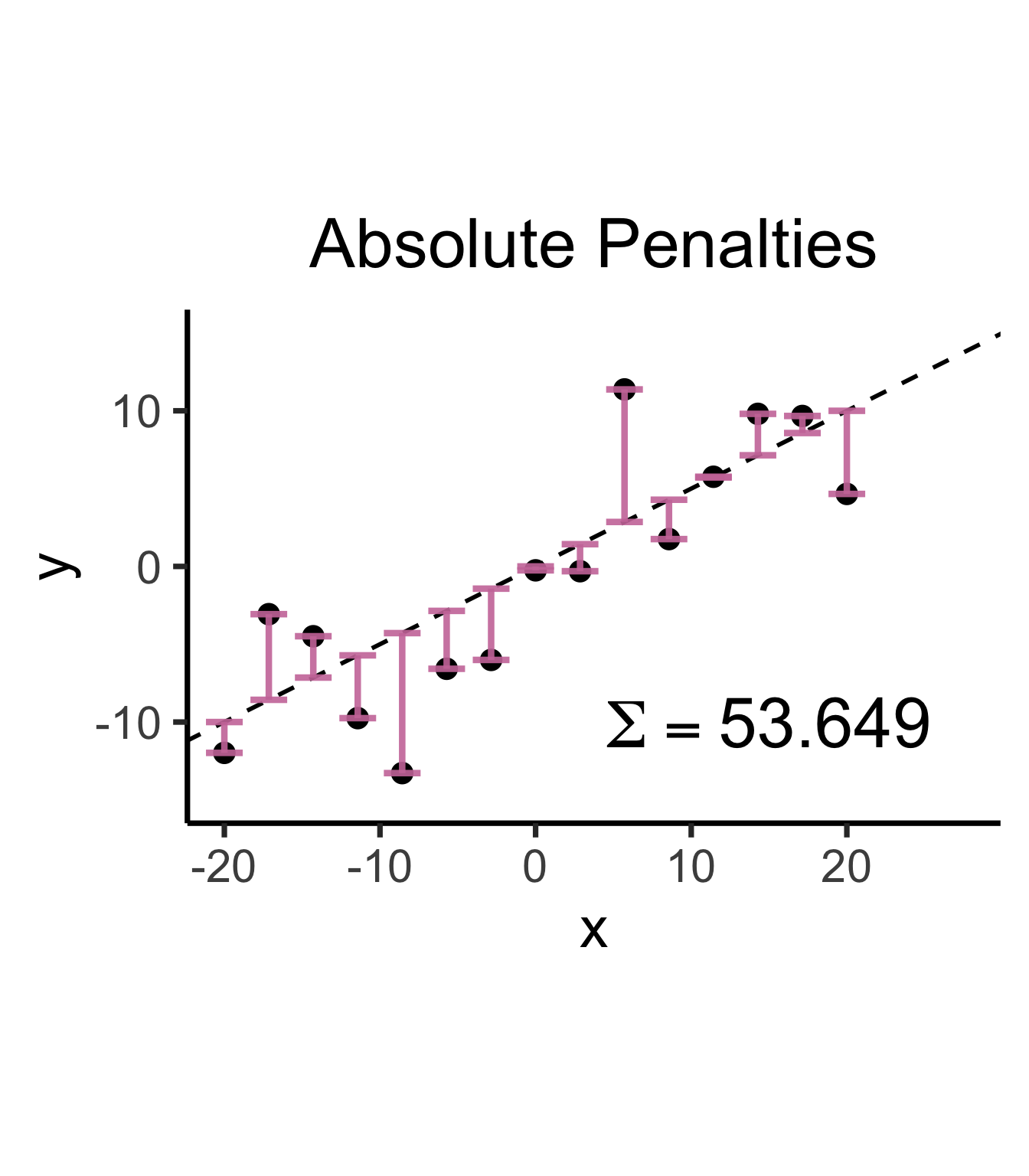

set.seed(5300)

slope <- 0.5

x_vals <- seq(from = -20, to = 20, length.out = 15)

N <- length(x_vals)

y_vals <- slope * x_vals + rnorm(N, 0, 5)

spread_vals <- y_vals - slope * x_vals

sim_lg_df <- tibble(

x = x_vals, y = y_vals, spread = spread_vals

)

abs_sum <- round(sum(abs(sim_lg_df$spread)), 3)

abs_label <- TeX(paste0("$\\Sigma = ",abs_sum,"$"))

sim_lg_df |> ggplot(aes(x=x, y=y)) +

geom_point(size=g_pointsize * 0.9) +

geom_abline(

slope=slope,

intercept=0,

linetype="dashed",

color='black',

linewidth=g_linewidth

) +

geom_segment(

aes(xend=x, yend=slope * x),

arrow=arrow(

angle=90,

length=unit(0.125,'inches'),

ends='both'

),

linewidth=1.5*g_linewidth,

color=cb_palette[7],

alpha=0.9,

) +

ylim(-15, 15) +

xlim(-20, 27.5) +

coord_equal() +

theme_dsan(base_size=28) +

labs(title="Absolute Penalties") +

geom_text(

data=data.frame(x=15, y=-10), label=abs_label,

size=12

)

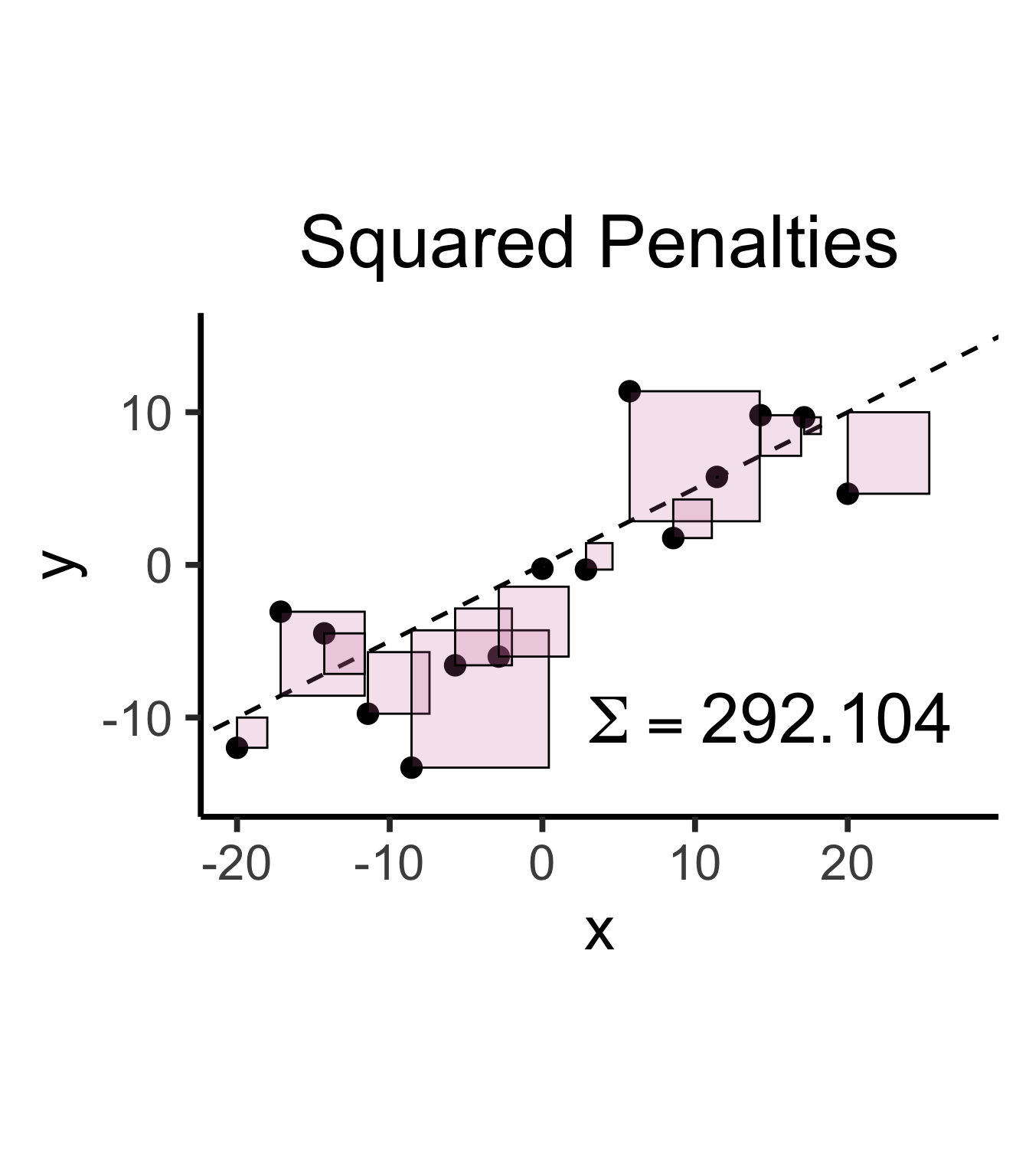

sq_sum <- round(sum((sim_lg_df$spread)^2), 3)

sq_label <- TeX(paste0("$\\Sigma = ",sq_sum,"$"))

sim_lg_df |> ggplot(aes(x=x, y=y)) +

geom_point(size=g_pointsize * 0.9) +

geom_abline(

slope=slope,

intercept=0,

linetype="dashed",

color='black',

linewidth=g_linewidth

) +

geom_rect(

aes(

xmin=x,

xmax=x+abs(spread),

ymin=ifelse(spread < 0, y, y - spread),

ymax=ifelse(spread < 0, y - spread, y)

),

color='black',

fill=cb_palette[7],

alpha=0.2,

) +

ylim(-15, 15) +

xlim(-20, 27.5) +

coord_equal() +

theme_dsan(base_size=30) +

labs(title="Squared Penalties") +

geom_text(

data=data.frame(x=15, y=-10), label=sq_label,

size=12

)Warning in is.na(x): is.na() applied to non-(list or vector) of type

'expression'

Warning in is.na(x): is.na() applied to non-(list or vector) of type

'expression'

\[ \widehat{y} = \underbrace{\widehat{\beta}_0}_{\mathclap{\small\begin{array}{c}\text{Estimated} \\[-5mm] \text{intercept}\end{array}}} ~+~ \underbrace{\widehat{\beta}_1}_{\mathclap{\small\begin{array}{c}\text{Estimated} \\[-4mm] \text{slope}\end{array}}}\cdot x \]

is chosen so that

\[ \widehat{\theta} = \left(\widehat{\beta}_0, \widehat{\beta}_1\right) = \argmin_{\beta_0, \beta_1}\left[ \sum_{x_i \in X} \left(~~\overbrace{\widehat{y}(x_i)}^{\mathclap{\small\text{Predicted }y}} - \overbrace{\expect{Y \mid X = x_i}}^{\small \text{Avg. }y\text{ when }x = x_i}\right)^{2~} \right] \]

“Fitting” a statistical model to data means minimizing some loss function that measures “how bad” our predictions are:

Find \(x^*\), the solution to

\[ \begin{align} \min_{x} ~ & f(x) &\text{(Objective function)} \\ \text{s.t. } ~ & g(x) = 0 &\text{(Constraints)} \end{align} \]

\[ x^* = \argmax_{x,~\lambda}f(x) - \lambda[g(x)] \]

(Why worry about constraints when OLS is unconstrained? …Soon we’ll need to penalize complexity!)

Find \(x^*\), the solution to

\[ \begin{align} \min_{x} ~ & f(x) = 3x^2 - x \\ \text{s.t. } ~ & \varnothing \end{align} \]

Computing the derivative:

\[ f'(x) = \frac{\partial}{\partial x}f(x) = \frac{\partial}{\partial x}\left[3x^2 - x\right] = 6x - 1, \]

Solving for \(x^*\), the value(s) satisfying \(\frac{\partial}{\partial x}f'(x^*) = 0\) for just-derived \(f'(x)\):

\[ f'(x^*) = 0 \iff 6x^* - 1 = 0 \iff x^* = \frac{1}{6}. \]

| Type of Thing | Thing | Change in Thing when \(x\) Changes by Tiny Amount |

|---|---|---|

| Polynomial | \(f(x) = x^n\) | \(f'(x) = \frac{\partial}{\partial x}f(x) = nx^{n-1}\) |

| Fraction | \(f(x) = \frac{1}{x}\) | Use Polynomial rule (since \(\frac{1}{x} = x^{-1}\)) to get \(f'(x) = -\frac{1}{x^2}\) |

| Logarithm | \(f(x) = \ln(x)\) | \(f'(x) = \frac{\partial}{\partial x} = \frac{1}{x}\) |

| Exponential | \(f(x) = e^x\) | \(f'(x) = \frac{\partial}{\partial x}e^x = e^x\) (🧐❗️) |

| Multiplication | \(f(x) = g(x)h(x)\) | \(f'(x) = g'(x)h(x) + g(x)h'(x)\) |

| Division | \(f(x) = \frac{g(x)}{h(x)}\) | Too hard to memorize… turn it into Multiplication, as \(f(x) = g(x)(h(x))^{-1}\) |

| Composition (Chain Rule) | \(f(x) = g(h(x))\) | \(f'(x) = g'(h(x))h'(x)\) |

| Fancy Logarithm | \(f(x) = \ln(g(x))\) | \(f'(x) = \frac{g'(x)}{g(x)}\) by Chain Rule |

| Fancy Exponential | \(f(x) = e^{g(x)}\) | \(f'(x) = g'(x)e^{g(x)}\) by Chain Rule |