Week 3: Getting Fancy with Regression

DSAN 5300: Statistical Learning

Spring 2025, Georgetown University

Monday, January 27, 2025

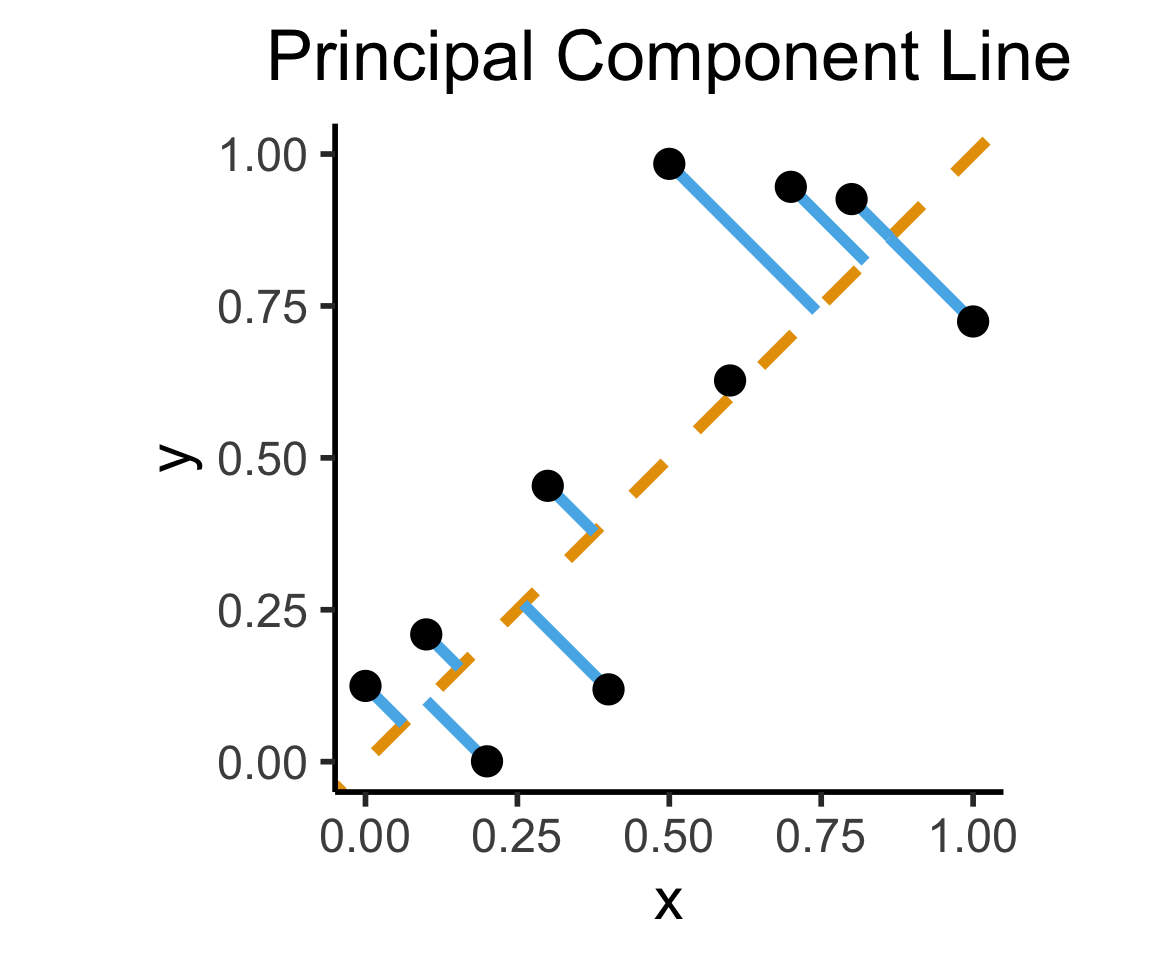

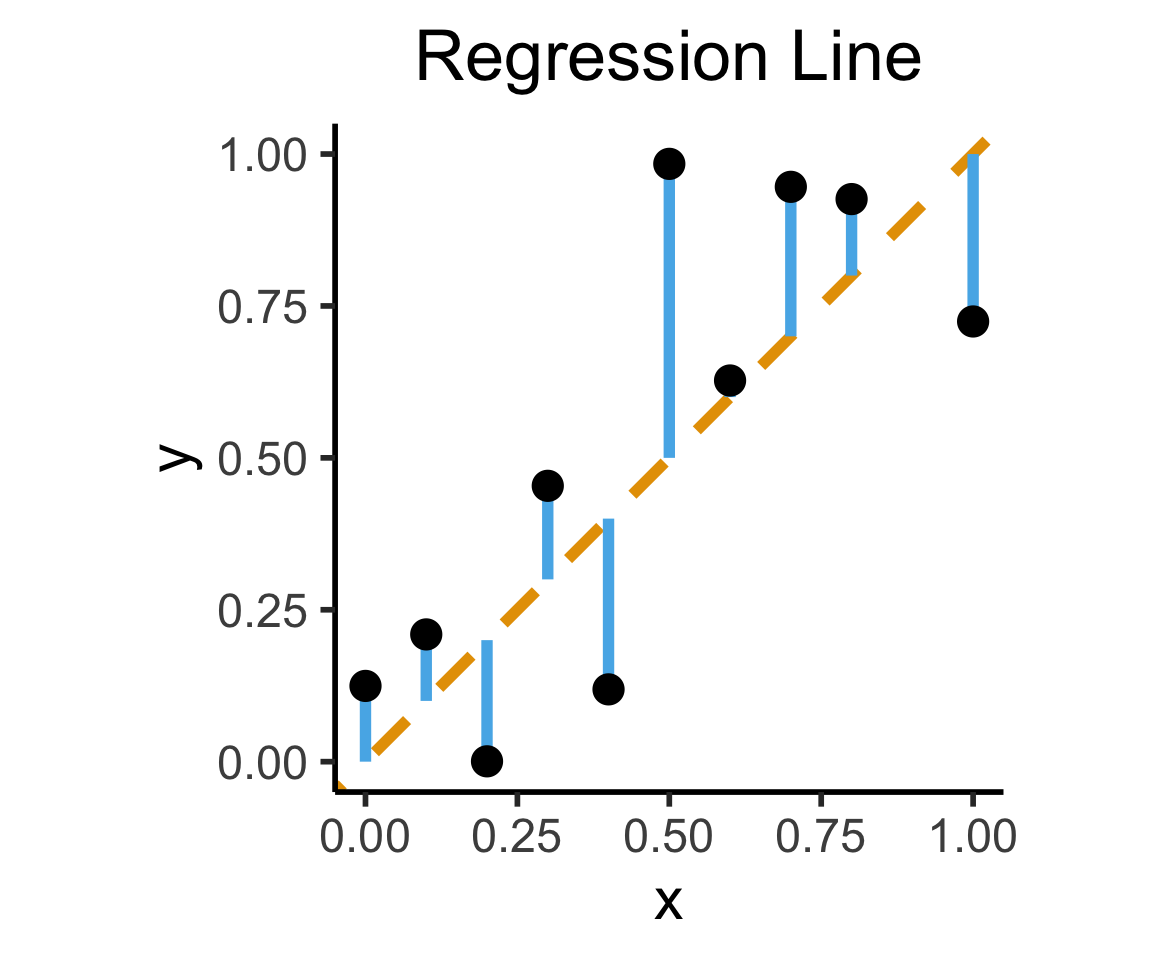

How Do We Define “Best”?

- Intuitively, two different ways to measure how well a line fits the data:

Code

library(tidyverse)

set.seed(5321)

N <- 11

x <- seq(from = 0, to = 1, by = 1 / (N - 1))

y <- x + rnorm(N, 0, 0.2)

mean_y <- mean(y)

spread <- y - mean_y

df <- tibble(x = x, y = y, spread = spread)

ggplot(df, aes(x=x, y=y)) +

geom_abline(slope=1, intercept=0, linetype="dashed", color=cbPalette[1], linewidth=g_linewidth*2) +

geom_segment(xend=(x+y)/2, yend=(x+y)/2, linewidth=g_linewidth*2, color=cbPalette[2]) +

geom_point(size=g_pointsize) +

coord_equal() +

xlim(0, 1) + ylim(0, 1) +

dsan_theme("half") +

labs(

title = "Principal Component Line"

)

ggplot(df, aes(x=x, y=y)) +

geom_abline(slope=1, intercept=0, linetype="dashed", color=cbPalette[1], linewidth=g_linewidth*2) +

geom_segment(xend=x, yend=x, linewidth=g_linewidth*2, color=cbPalette[2]) +

geom_point(size=g_pointsize) +

coord_equal() +

xlim(0, 1) + ylim(0, 1) +

dsan_theme("half") +

labs(

title = "Regression Line"

)

Visualizing Multiple Linear Regression

(ISLR, Fig 3.5): A pronounced non-linear relationship. Positive residuals (visible above the surface) tend to lie along the 45-degree line, where budgets are split evenly. Negative residuals (most not visible) tend to be away from this line, where budgets are more lopsided.

Another MLR Superpower: Incorporating Categorical Vars

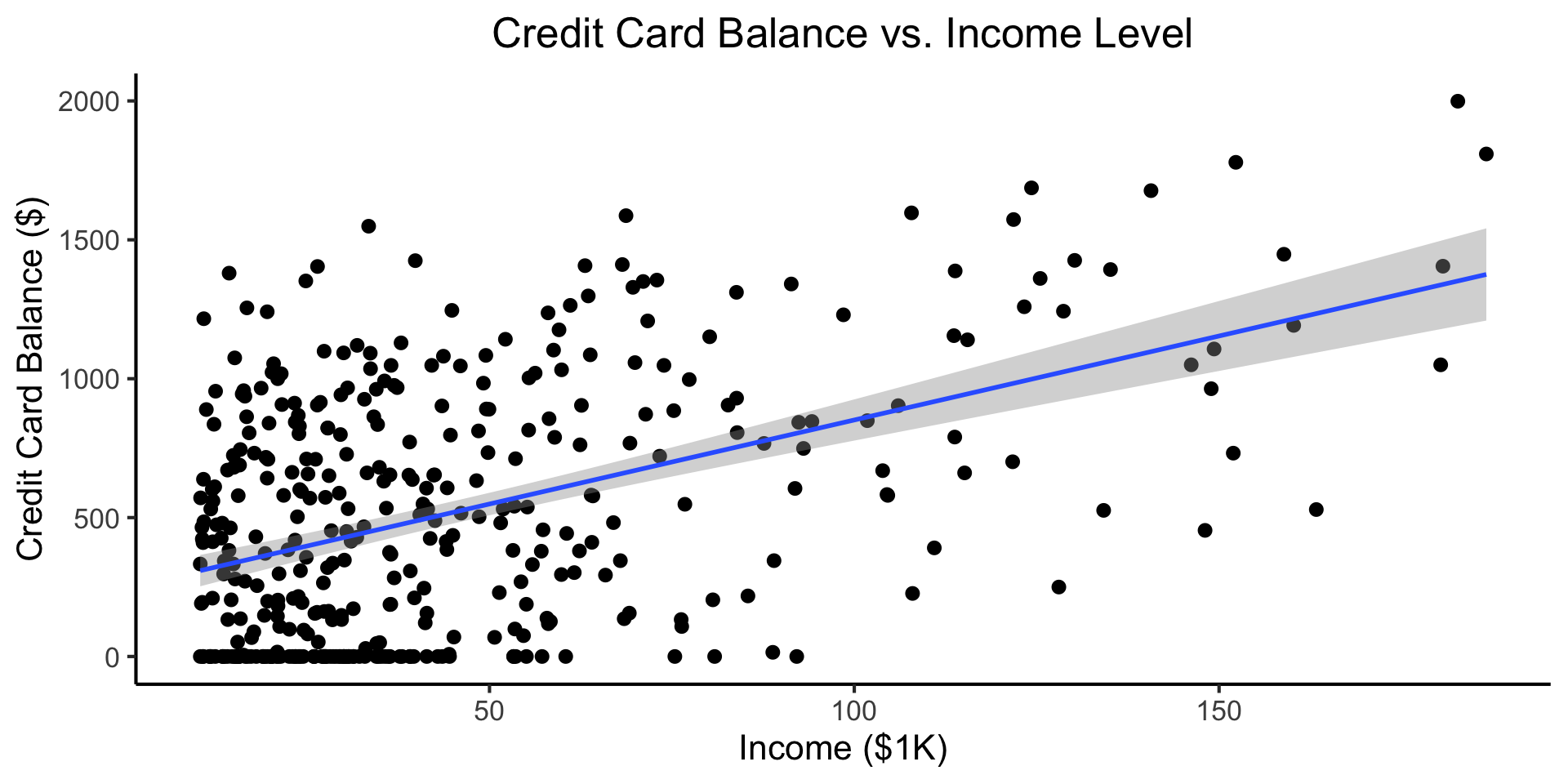

\[ \begin{align*} Y &= \beta_0 + \beta_1 \times \texttt{income} \\ &\phantom{Y} \end{align*} \]

Code

credit_df <- read_csv("assets/Credit.csv")

credit_plot <- credit_df |> ggplot(aes(x=Income, y=Balance)) +

geom_point(size=0.5*g_pointsize) +

geom_smooth(method='lm', formula="y ~ x", linewidth=1) +

theme_dsan() +

labs(

title="Credit Card Balance vs. Income Level",

x="Income ($1K)",

y="Credit Card Balance ($)"

)

credit_plot

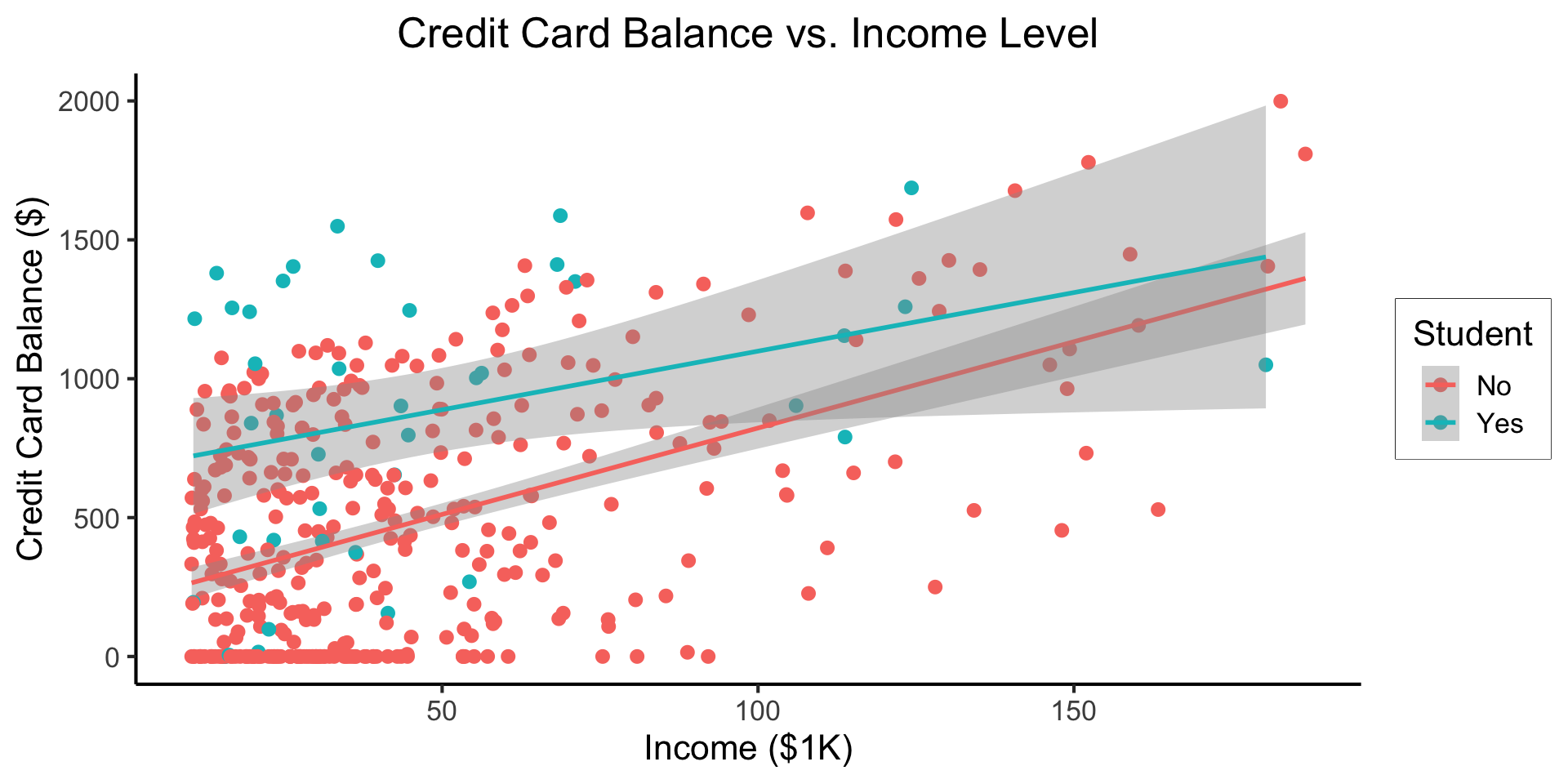

\[ \begin{align*} Y = &\beta_0 + \beta_1 \times \texttt{income} + \beta_2 \times \texttt{Student} \\ &+ \beta_3 \times (\texttt{Student} \times \texttt{Income}) \end{align*} \]

Code

- Why do we need the \(\texttt{Student} \times \texttt{Income}\) term?

- Understanding this setup will open up a vast array of possibilities for regression 😎

- (Dear future Jeff, let’s go through this on the board! Sincerely, past Jeff)

From MLR to Logistic Regression

- As DSAN students, you know that we’re still sweeping classification under the rug!

- We saw how to include binary/multiclass covariates, but what if the actual thing we’re trying to predict is binary?

- The wrong approach is the “Linear Probability Model”:

\[ \Pr(Y \mid X) = \beta_0 + \beta_1 X + \varepsilon \]

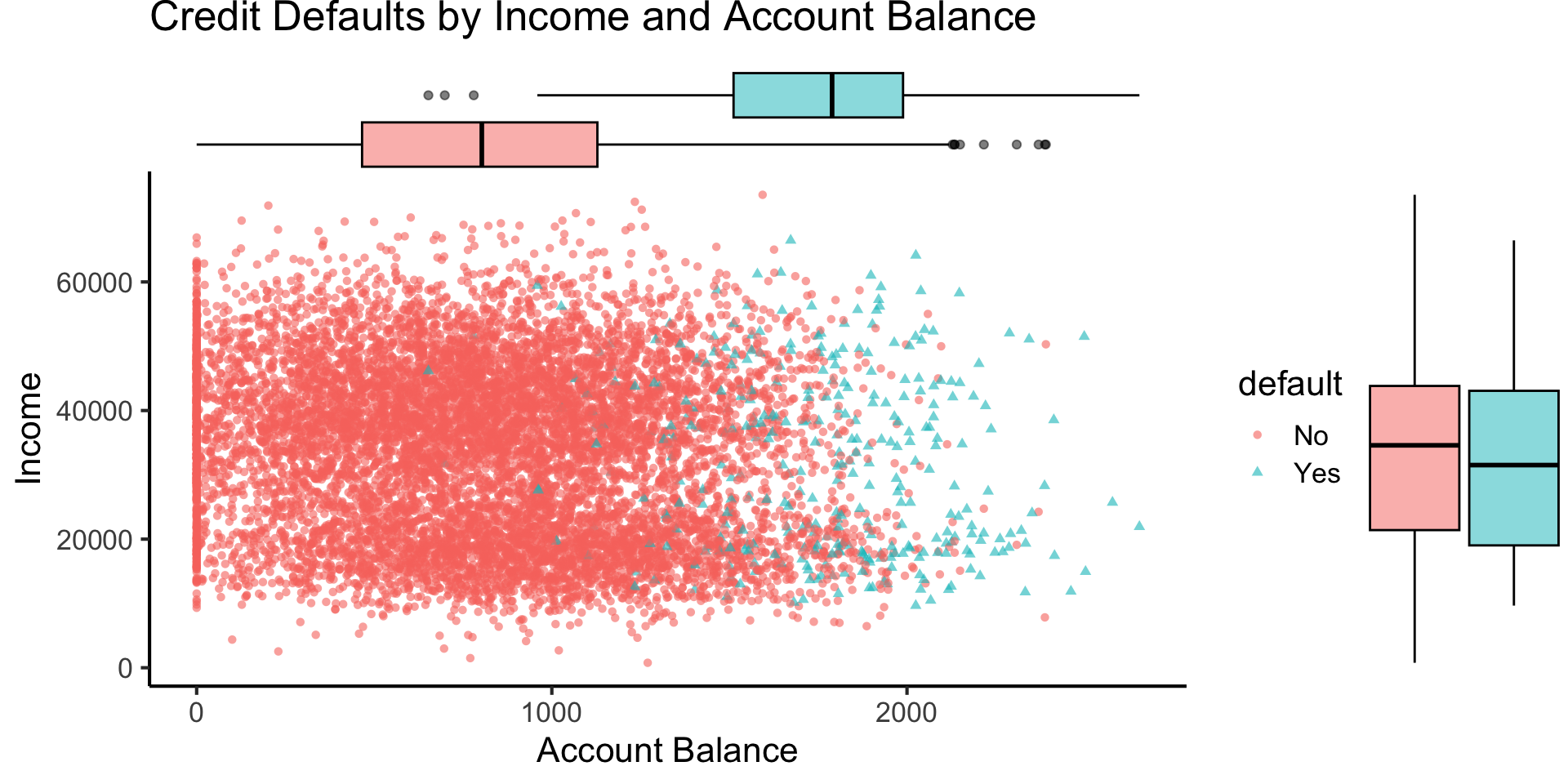

Credit Default

Code

library(tidyverse)

library(ggExtra)

default_df <- read_csv("assets/Default.csv") |>

mutate(default_num = ifelse(default=="Yes",1,0))

default_plot <- default_df |> ggplot(aes(x=balance, y=income, color=default, shape=default)) +

geom_point(alpha=0.6) +

theme_classic(base_size=16) +

labs(

title="Credit Defaults by Income and Account Balance",

x = "Account Balance",

y = "Income"

)

default_mplot <- default_plot |> ggMarginal(type="boxplot", groupColour=FALSE, groupFill=TRUE)

default_mplot

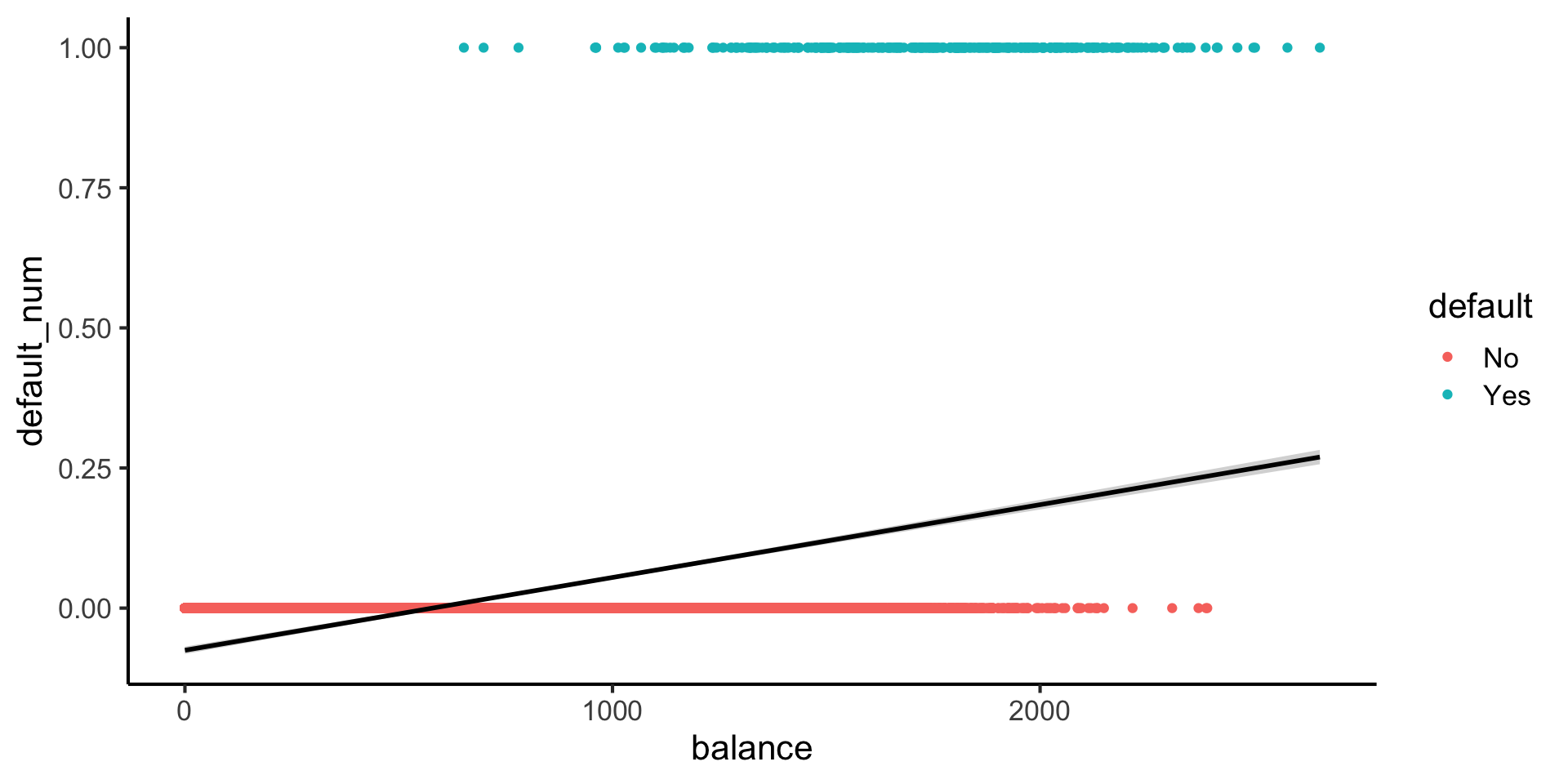

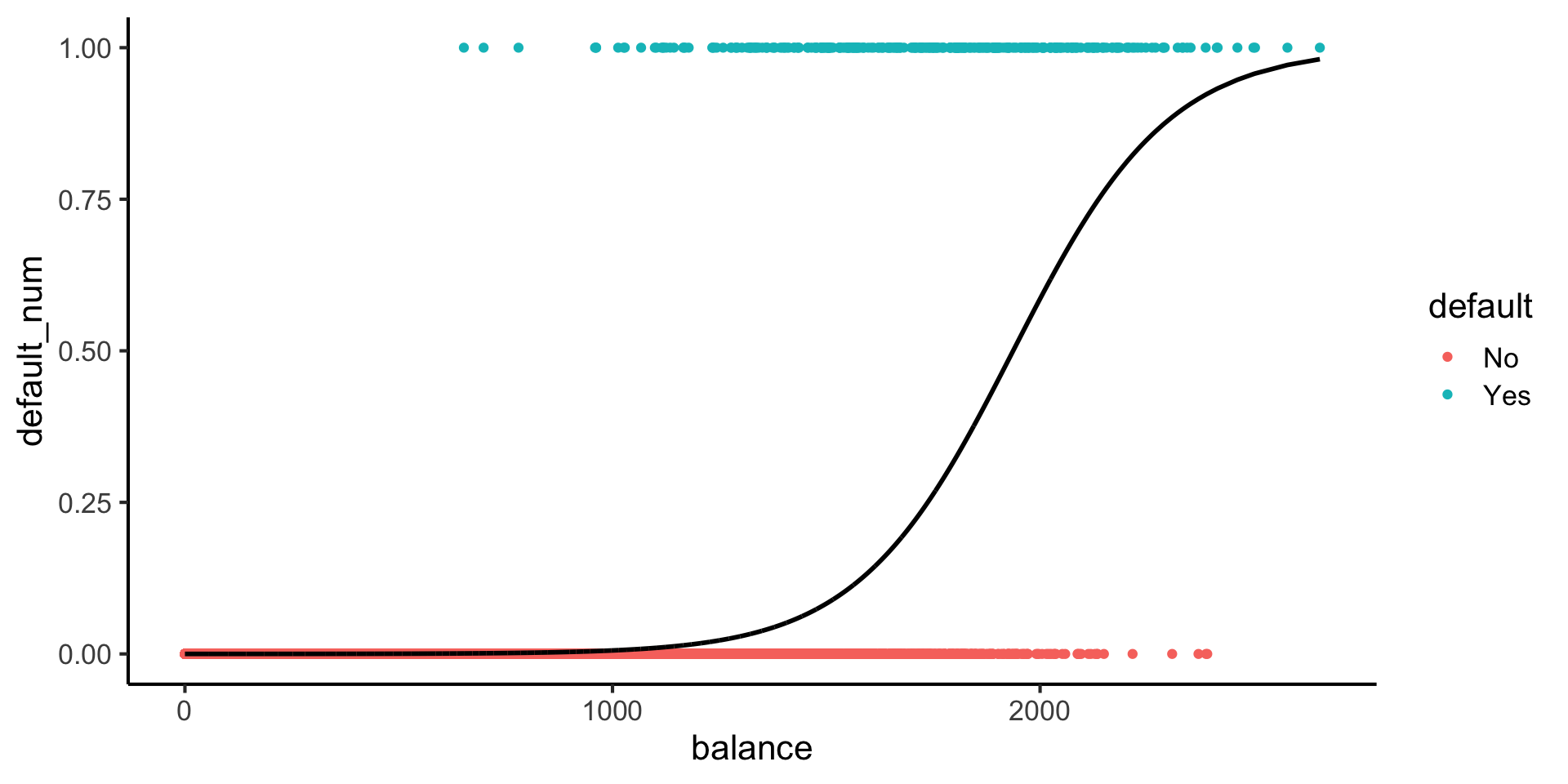

Lines vs. Sigmoids(!)

Here’s what lines look like for this dataset:

Here’s what sigmoids look like:

Code

library(tidyverse)

logistic_model <- glm(default_num ~ balance, family=binomial(link='logit'),data=default_df)

default_df$predictions <- predict(logistic_model, newdata = default_df, type = "response")

my_sigmoid <- function(x) 1 / (1+exp(-x))

default_df |> ggplot(aes(x=balance, y=default_num)) +

#stat_function(fun=my_sigmoid) +

geom_point(aes(color=default)) +

geom_line(

data=default_df,

aes(x=balance, y=predictions),

linewidth=1

) +

theme_classic(base_size=16)

\[ \Pr(Y \mid X) = \beta_0 + \beta_1 X + \varepsilon \]

\[ \log\underbrace{\left[ \frac{\Pr(Y \mid X)}{1 - \Pr(Y \mid X)} \right]}_{\mathclap{\smash{\text{Odds Ratio}}}} = \beta_0 + \beta_1 X + \varepsilon \]