Week 11: Hypothesis Testing

DSAN 5100: Probabilistic Modeling and Statistical Computing

Section 01

Tuesday, November 11, 2025

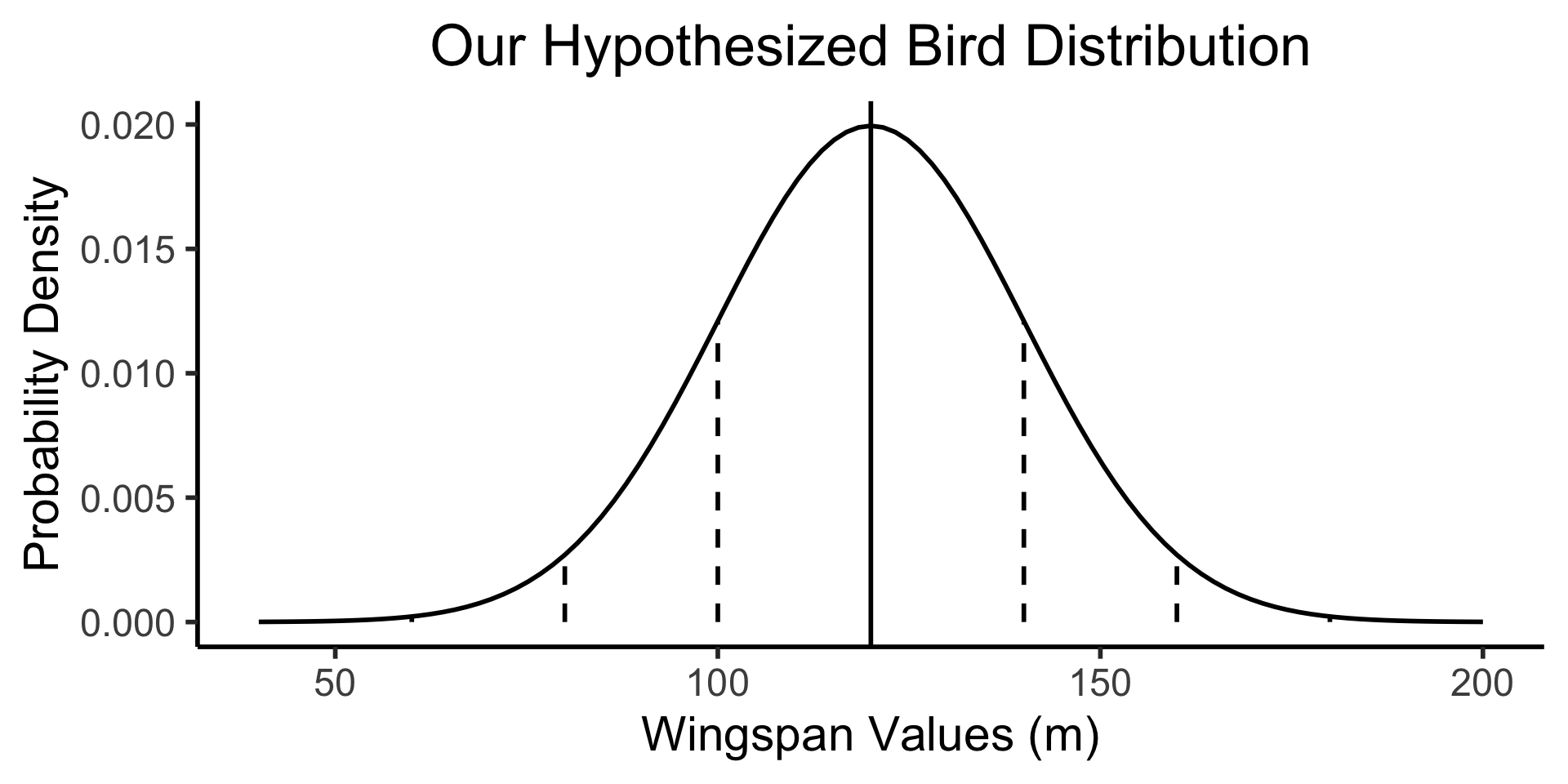

Example 1: Bird Wingspans

- Trying to figure out the population distribution of bird wingspans.

- We hypothesize \(\mu_0 = 120\text{cm}\)

- Somehow we know the population variance \(\sigma = 20\text{cm}\), and we know that bird wingspans form a normal distribution, but we don’t know the true \(\mu\):

Code

library(tidyverse)

hyp_mu <- 120

sigma <- 20

bird_dnorm <- function(x) dnorm(x, mean=hyp_mu, sd=sigma)

sigma_df <- tribble(

~x,

hyp_mu - 3 * sigma,

hyp_mu - 2 * sigma,

hyp_mu - 1 * sigma,

hyp_mu + 1 * sigma,

hyp_mu + 2 * sigma,

hyp_mu + 3 * sigma

)

sigma_df <- sigma_df |> mutate(

y = 0,

xend = x,

yend = bird_dnorm(x)

)

plot_rad <- 4 * sigma

plot_bounds <- c(hyp_mu - plot_rad, hyp_mu + plot_rad)

bird_plot <- ggplot(data=data.frame(x=plot_bounds), aes(x=x)) +

stat_function(fun=bird_dnorm, linewidth=g_linewidth) +

geom_vline(aes(xintercept=hyp_mu), linewidth=g_linewidth) +

geom_segment(data=sigma_df, aes(x=x, y=y, xend=xend, yend=yend), linewidth=g_linewidth, linetype="dashed") +

dsan_theme("half") +

labs(

title = "Our Hypothesized Bird Distribution",

x = "Wingspan Values (m)",

y = "Probability Density"

)

bird_plot

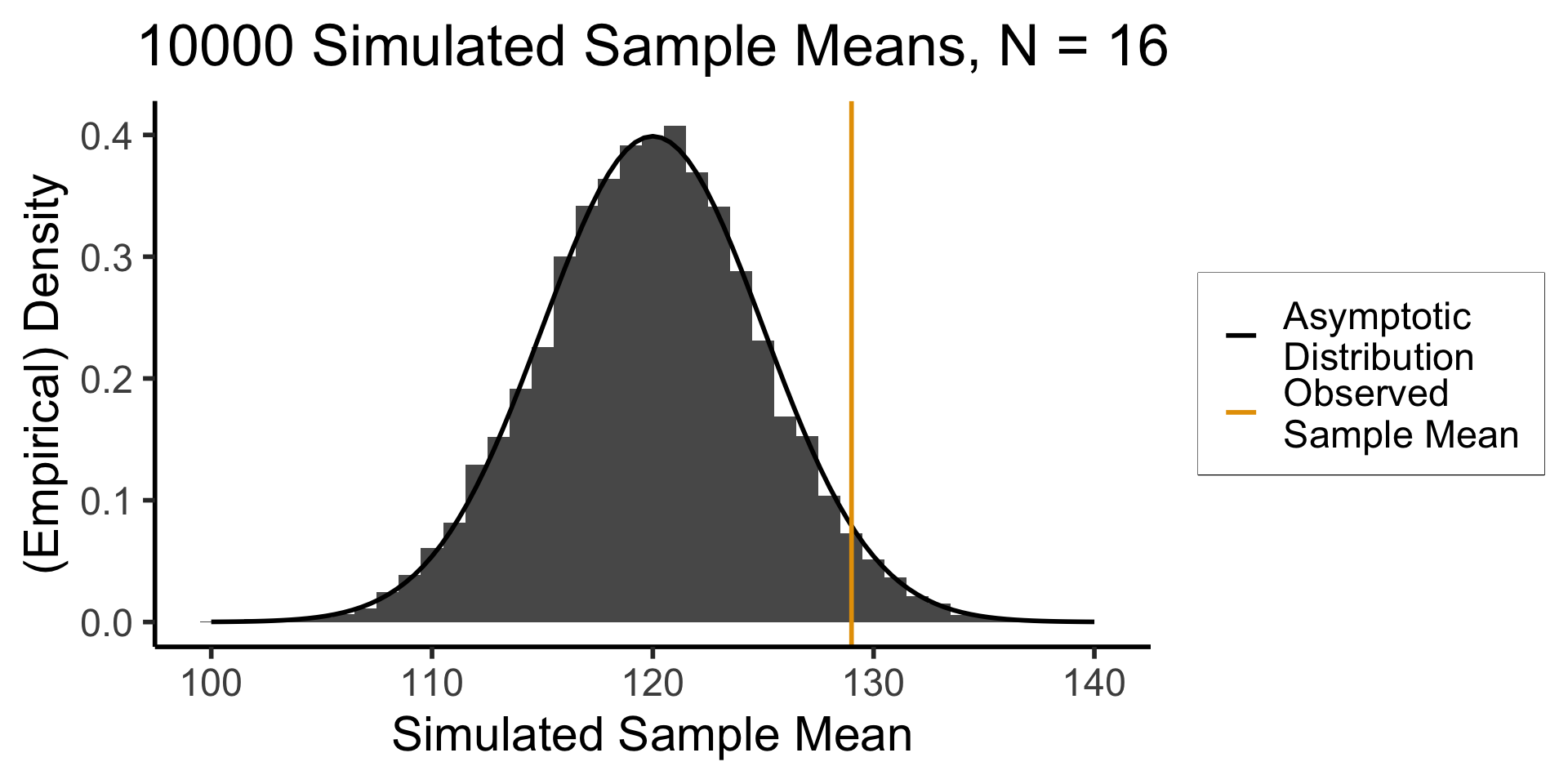

What Would Sample Means Look Like If Hypothesis Was True?

- What we know, from asymptotic sample theory, is that \(Z = \frac{\overline{X} - \mu}{\sigma / \sqrt{N}}\) is approximately standard normal, for sufficiently large values of \(N\)!

- So, let’s (1) plot this distribution, for a bunch of potential sample means, and then (2) see where our actual observed sample mean lies on this distribution!

- Sanity check: let’s actually simulate taking sample means from 1000 size-16 samples:

Code

simulate_sample_mean <- function(N, mu, sigma) {

samples <- rnorm(N, mu, sigma)

sample_mean <- mean(samples)

return(sample_mean)

}

N <- 16

obs_sample_mean <- 129

num_reps <- 10000

sample_means <- as_tibble(replicate(num_reps, simulate_sample_mean(N, hyp_mu, sigma)))

asymp_dnorm <- function(x) dnorm((x - hyp_mu)/(sigma / sqrt(N)), 0, 1)

ggplot() +

geom_histogram(

data=sample_means,

aes(x=value, y=5*after_stat(density)),

binwidth=1) +

stat_function(

data=data.frame(x=c(100,140)),

aes(x=x, color='asymp'),

fun=asymp_dnorm,

linewidth = g_linewidth

) +

geom_segment(

aes(x = obs_sample_mean, xend=obs_sample_mean, y=-Inf, yend=Inf, color='obs'),

linewidth = g_linewidth

) +

dsan_theme("half") +

labs(

x = "Simulated Sample Mean",

y = "(Empirical) Density",

title = paste0(num_reps," Simulated Sample Means, N = 16")

) +

scale_color_manual(values=c('asymp'='black', 'obs'=cbPalette[1]), labels=c('asymp'='Asymptotic\nDistribution', 'obs'='Observed\nSample Mean')) +

remove_legend_title()

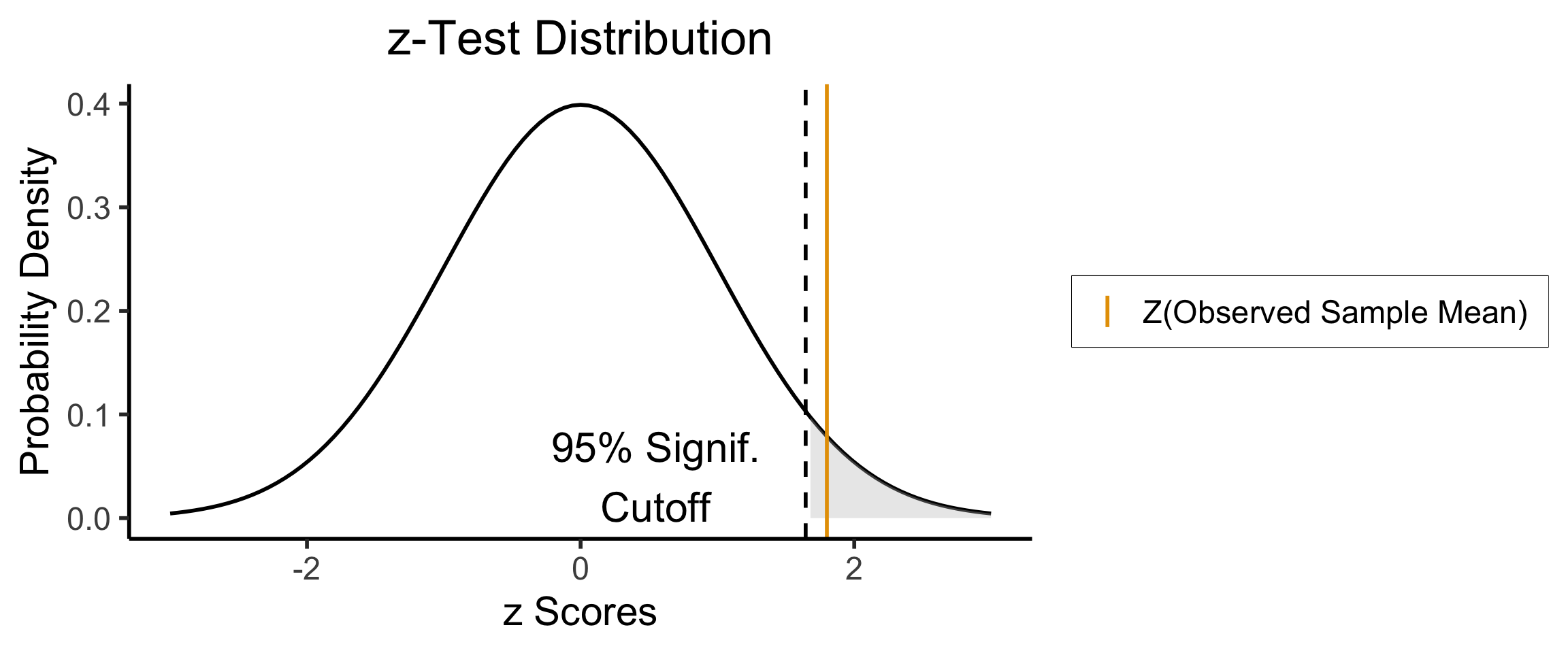

Right-Tailed Test

- Null hypothesis (in all cases) is \(H_0: \mu = \mu_0\); Right-tailed test is of alternative hypothesis \(H_A: \mu > \mu_0\)

- We reject the null if the observed sample mean \(\overline{X} = 131\) is too unlikely in the world where the null is true: \(Z(\overline{X}) \approx 1.8\)

- What cutoff should we use for “too unlikely”? (See last week’s slides…) here we’ll use \(\alpha = 0.05\): \(\int_{1.645}^{\infty}\varphi(x)dx = 0.05\), so \(1.645\) is our “critical” (cutoff) value

Code

label_df_signif_int <- tribble(

~x, ~y, ~label,

0.55, 0.04, "95% Signif.\nCutoff"

)

signif_cutoff <- 1.645

funcShaded <- function(x, lower_bound, upper_bound){

y <- dnorm(x)

y[x < lower_bound | x > upper_bound] <- NA

return(y)

}

funcShadedIntercept <- function(x) funcShaded(x, int_tstat, Inf)

funcShadedSignif <- function(x) funcShaded(x, signif_cutoff, Inf)

compute_z_val <- function(x) {

return ((x - hyp_mu) / (sigma / sqrt(N)))

}

obs_zval <- compute_z_val(obs_sample_mean)

obs_zval_str <- sprintf("%.2f", obs_zval)

sample_dnorm <- function(x) dnorm(compute_z_val(x))

ggplot(data=data.frame(x=c(-3,3)), aes(x=x)) +

stat_function(fun=dnorm, linewidth=g_linewidth) +

#geom_segment(data=sigma_df, aes(x=x, y=y, xend=xend, yend=yend), linewidth=g_linewidth, linetype="dashed") +

stat_function(fun = funcShadedSignif, geom = "area", fill = "grey", alpha = 0.333) +

geom_vline(aes(xintercept = signif_cutoff), linewidth=g_linewidth, linetype="dashed") +

geom_text(label_df_signif_int, mapping = aes(x = x, y = y, label = label), size = 8) +

geom_vline(aes(xintercept = obs_zval, color='sample_mean'), linewidth=g_linewidth) +

dsan_theme("half") +

labs(

title = "z-Test Distribution",

x = "z Scores",

y = "Probability Density"

) +

scale_color_manual(values=c('sample_mean'=cbPalette[1]), labels=c('sample_mean'='Z(Observed Sample Mean)')) +

remove_legend_title()

- Since \(Z(\overline{X}) > 1.645\), we reject the null hypothesis that this sample mean was generated by a distribution with mean \(\mu_0\)!

Two-Tailed Test

- Null hypothesis (in all cases) is \(H_0: \mu = \mu_0\); Two-tailed test is of alternative hypothesis \(H_A: \mu \neq \mu_0\) (the actual logical negation of the null hypothesis…)

- Reject the null if observed sample mean \(\overline{X} = 131\) is too unlikely in null world

- What cutoff should we use for “too unlikely”? Here we’ll use \(\alpha = 0.05\), but for a two tailed test we find \(\int_{-\infty}^{-1.96}\varphi(x)dx + \int_{1.96}^{\infty}\varphi(x)dx = 0.05\), so \(1.96\) is our “critical” (cutoff) value

Code

signif_cutoff <- 1.96

neg_signif_cutoff <- -signif_cutoff

label_df_signif_int <- tribble(

~x, ~y, ~label,

-2.45, 0.18, paste0("Left\nCutoff\n(",neg_signif_cutoff,")"),

2.45, 0.18, paste0("Right\nCutoff\n(",signif_cutoff,")")

)

funcShaded <- function(x, lower_bound, upper_bound){

y <- dnorm(x)

y[x < lower_bound | x > upper_bound] <- NA

return(y)

}

funcShadedIntercept <- function(x) funcShaded(x, int_tstat, Inf)

funcShadedNegSignif <- function(x) funcShaded(x, -Inf, neg_signif_cutoff)

funcShadedSignif <- function(x) funcShaded(x, signif_cutoff, Inf)

compute_z_val <- function(x) {

return ((x - hyp_mu) / (sigma / sqrt(N)))

}

obs_zval <- compute_z_val(obs_sample_mean)

sample_dnorm <- function(x) dnorm(compute_z_val(x))

ggplot(data=data.frame(x=c(-3,3)), aes(x=x)) +

stat_function(fun=dnorm, linewidth=g_linewidth) +

#geom_segment(data=sigma_df, aes(x=x, y=y, xend=xend, yend=yend), linewidth=g_linewidth, linetype="dashed") +

stat_function(fun = funcShadedSignif, geom = "area", fill = "grey", alpha = 0.333) +

stat_function(fun = funcShadedNegSignif, geom = "area", fill = "grey", alpha = 0.333) +

geom_vline(aes(xintercept = neg_signif_cutoff), linewidth=g_linewidth, linetype="dashed") +

geom_vline(aes(xintercept = signif_cutoff), linewidth=g_linewidth, linetype="dashed") +

geom_text(label_df_signif_int, mapping = aes(x = x, y = y, label = label), size = 8) +

geom_vline(aes(xintercept = obs_zval, color='sample_mean'), linewidth=g_linewidth) +

dsan_theme("half") +

labs(

title = "z-Test Distribution",

x = "z Scores",

y = "Probability Density"

) +

scale_color_manual(values=c('sample_mean'=cbPalette[1]), labels=c('sample_mean'='Z(Observed Sample Mean)')) +

remove_legend_title()

- Since \(|Z(\overline{X})| < 1.96\), we fail to reject the null hypothesis that this sample mean was generated by a distribution with mean \(\mu_0\)!

What Is Regression?

- If science is understanding relationships between variables, regression is the most basic but fundamental tool we have to start measuring these relationships

- Often exactly what humans do when we see data!

psychology

trending_flat

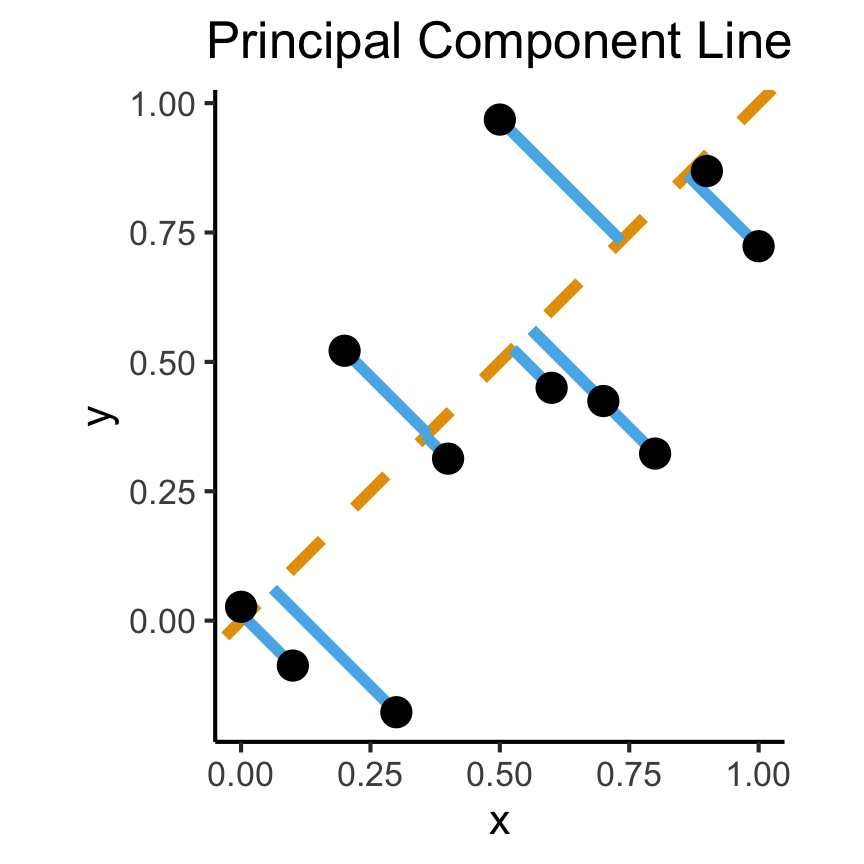

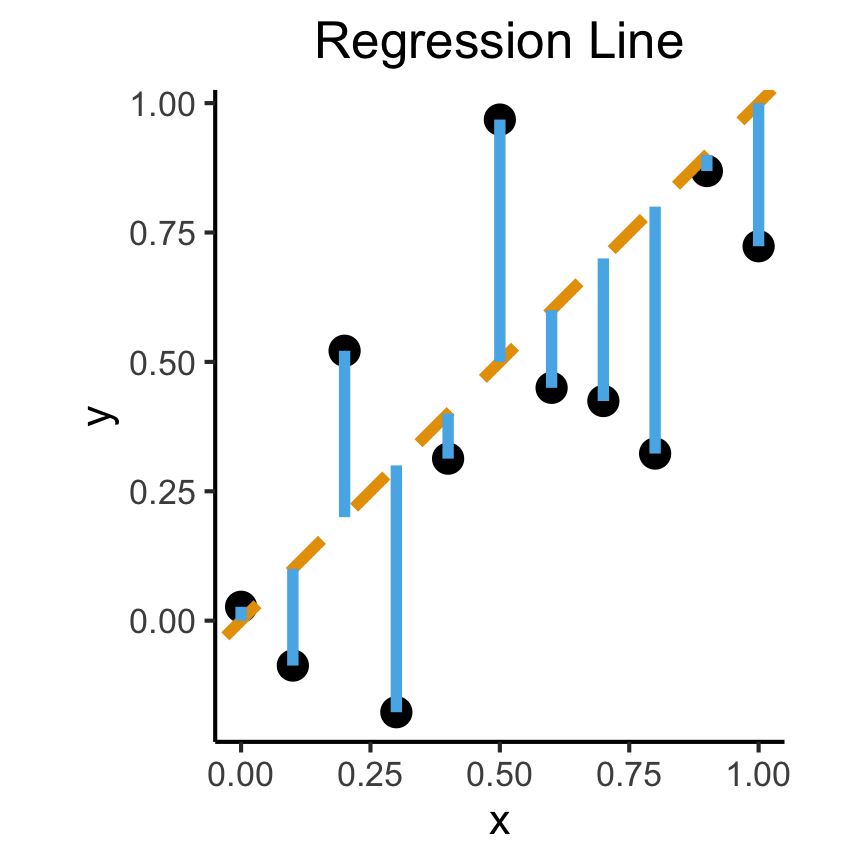

How Do We Define “Best”?

- Intuitively, two different ways to measure how well a line fits the data:

Code

set.seed(5100)

N <- 11

x <- seq(from = 0, to = 1, by = 1 / (N - 1))

y <- x + rnorm(N, 0, 0.25)

mean_y <- mean(y)

spread <- y - mean_y

df <- tibble(x = x, y = y, spread = spread)

ggplot(df, aes(x=x, y=y)) +

geom_abline(slope=1, intercept=0, linetype="dashed", color=cbPalette[1], linewidth=g_linewidth*2) +

geom_segment(xend=(x+y)/2, yend=(x+y)/2, linewidth=g_linewidth*2, color=cbPalette[2]) +

geom_point(size=g_pointsize) +

coord_equal() +

dsan_theme("full") +

labs(

title = "Principal Component Line"

)

Code

ggplot(df, aes(x=x, y=y)) +

geom_point(size=g_pointsize) +

geom_abline(slope=1, intercept=0, linetype="dashed", color=cbPalette[1], linewidth=g_linewidth*2) +

geom_segment(xend=x, yend=x, linewidth=g_linewidth*2, color=cbPalette[2]) +

dsan_theme("full") +

labs(

title = "Regression Line"

) +

coord_equal()

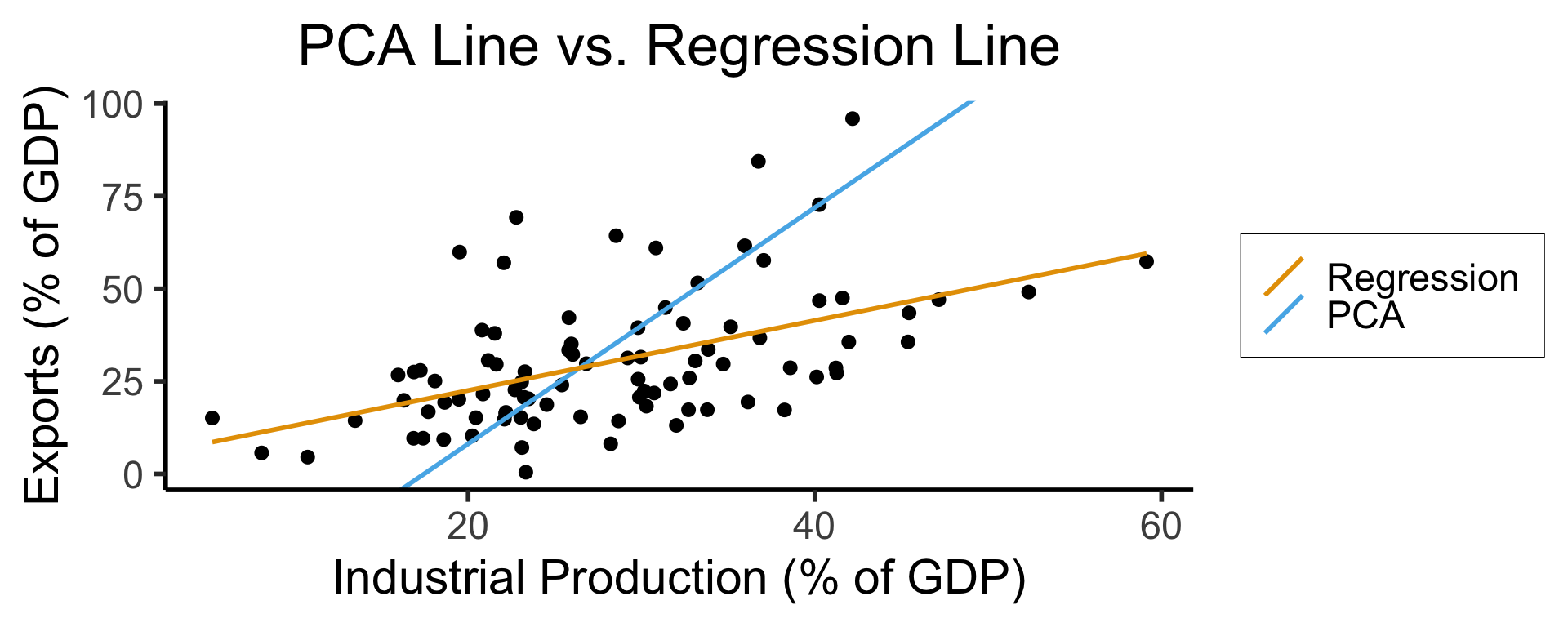

Principal Component Analysis

Principal Component Line allows projecting data onto its dimension of highest variance

More simply: PCA can discover meaningful axes in data (unsupervised learning / exploratory data analysis settings)

Code

library(readr)

library(ggplot2)

gdp_df <- read_csv("assets/gdp_pca.csv")

dist_to_line <- function(x0, y0, a, c) {

numer <- abs(a * x0 - y0 + c)

denom <- sqrt(a * a + 1)

return(numer / denom)

}

# Finding PCA line for industrial vs. exports

x <- gdp_df$industrial

y <- gdp_df$exports

lossFn <- function(lineParams, x0, y0) {

a <- lineParams[1]

c <- lineParams[2]

return(sum(dist_to_line(x0, y0, a, c)))

}

o <- optim(c(0, 0), lossFn, x0 = x, y0 = y)

ggplot(gdp_df, aes(x = industrial, y = exports)) +

geom_point(size=g_pointsize/2) +

geom_abline(aes(slope = o$par[1], intercept = o$par[2], color="pca"), linewidth=g_linewidth, show.legend = TRUE) +

geom_smooth(aes(color="lm"), method = "lm", se = FALSE, linewidth=g_linewidth, key_glyph = "blank") +

scale_color_manual(element_blank(), values=c("pca"=cbPalette[2],"lm"=cbPalette[1]), labels=c("Regression","PCA")) +

dsan_theme("half") +

remove_legend_title() +

labs(

title = "PCA Line vs. Regression Line",

x = "Industrial Production (% of GDP)",

y = "Exports (% of GDP)"

)

- See here for an amazing blog post using PCA to explore UN voting patterns!

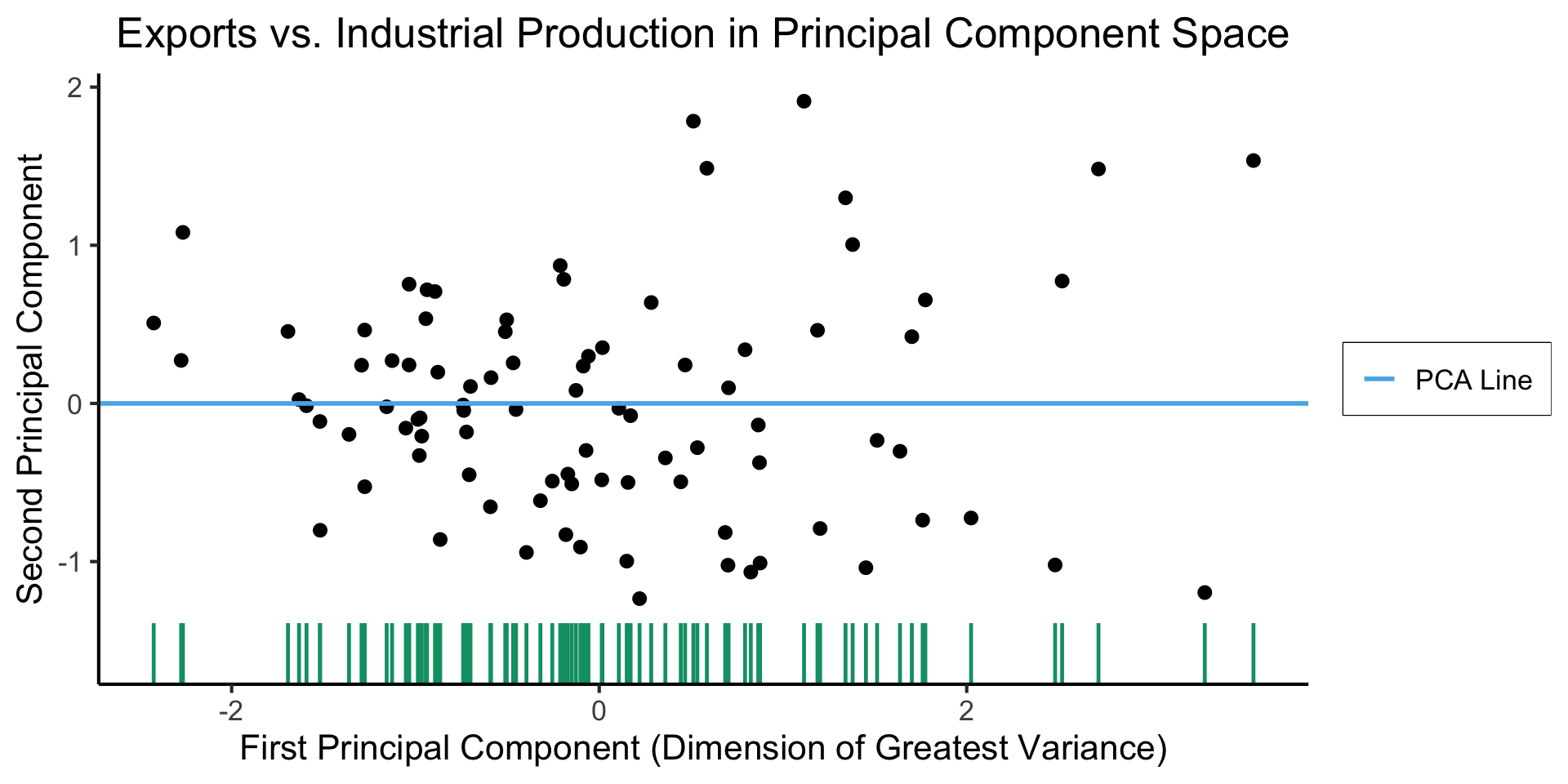

Create Your Own Dimension!

Code

ggplot(gdp_df, aes(pc1, .fittedPC2)) +

geom_point(size = g_pointsize/2) +

geom_hline(aes(yintercept=0, color='PCA Line'), linetype='solid', size=g_linesize) +

geom_rug(sides = "b", linewidth=g_linewidth/1.2, length = unit(0.1, "npc"), color=cbPalette[3]) +

expand_limits(y=-1.6) +

scale_color_manual(element_blank(), values=c("PCA Line"=cbPalette[2])) +

dsan_theme("full") +

remove_legend_title() +

labs(

title = "Exports vs. Industrial Production in Principal Component Space",

x = "First Principal Component (Dimension of Greatest Variance)",

y = "Second Principal Component"

)

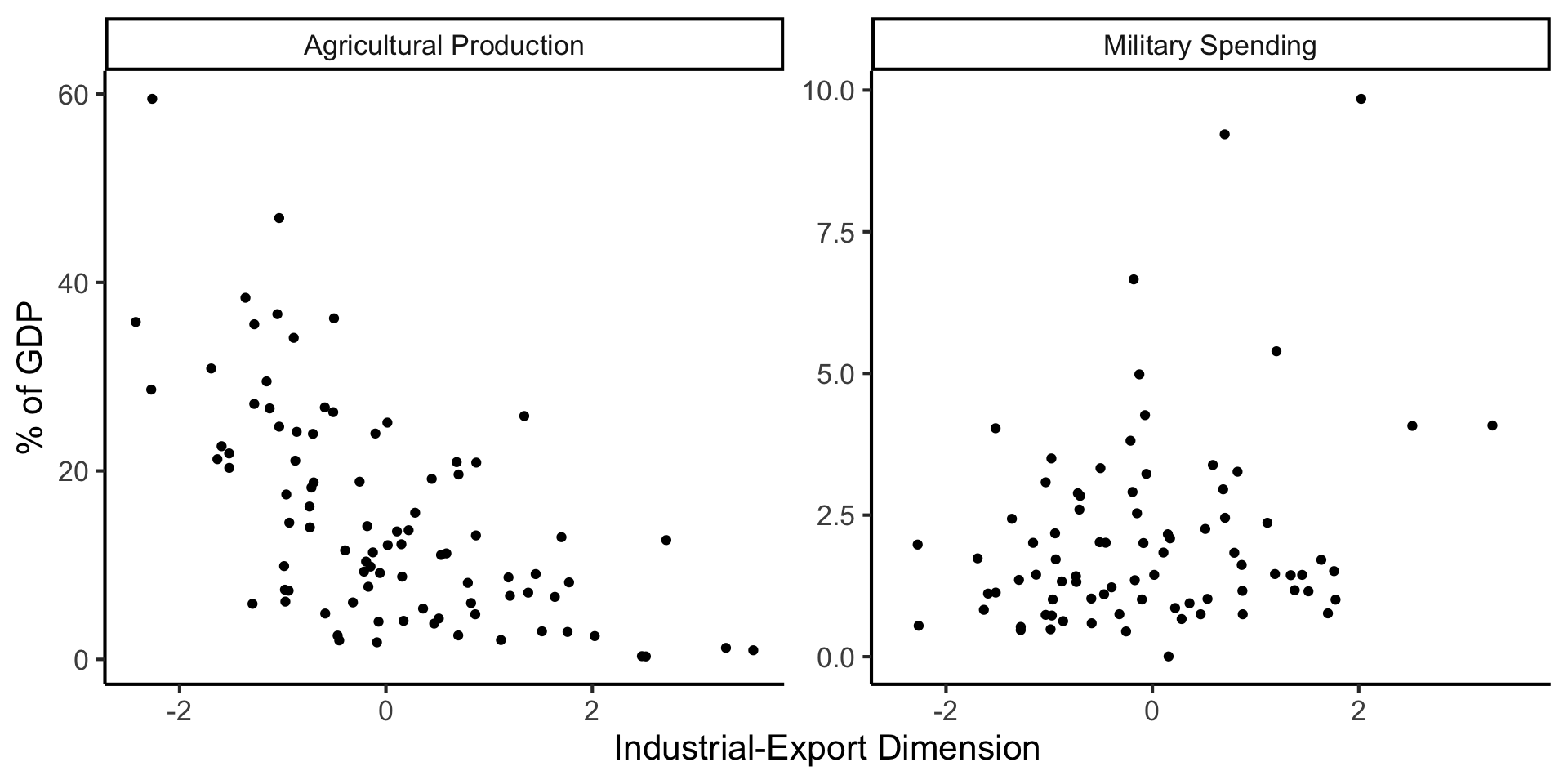

And Use It for EDA

Code

library(dplyr)

library(tidyr)

plot_df <- gdp_df %>% select(c(country_code, pc1, agriculture, military))

long_df <- plot_df %>% pivot_longer(!c(country_code, pc1), names_to = "var", values_to = "val")

long_df <- long_df |> mutate(

var = case_match(

var,

"agriculture" ~ "Agricultural Production",

"military" ~ "Military Spending"

)

)

ggplot(long_df, aes(x = pc1, y = val, facet = var)) +

geom_point() +

facet_wrap(vars(var), scales = "free") +

dsan_theme("full") +

labs(

x = "Industrial-Export Dimension",

y = "% of GDP"

)

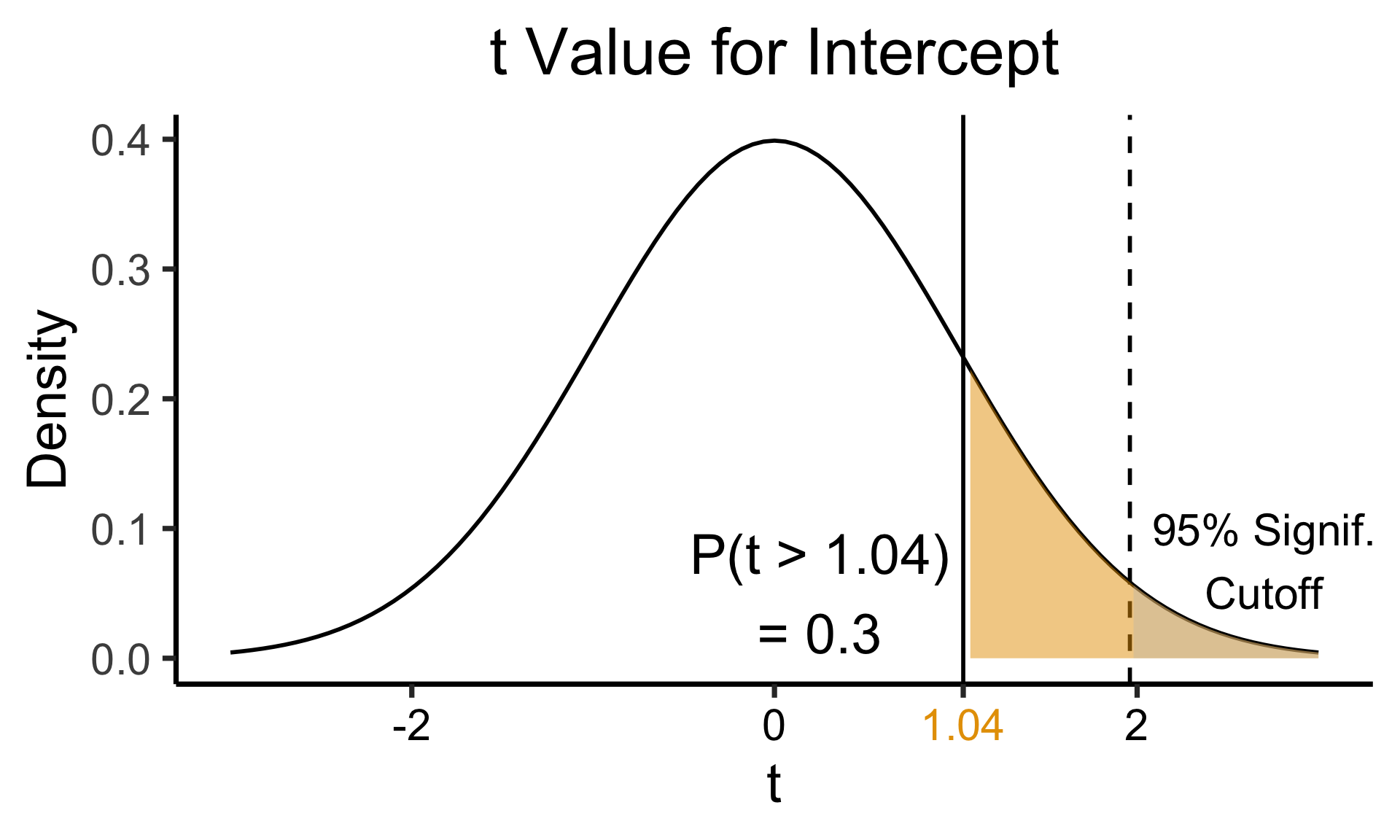

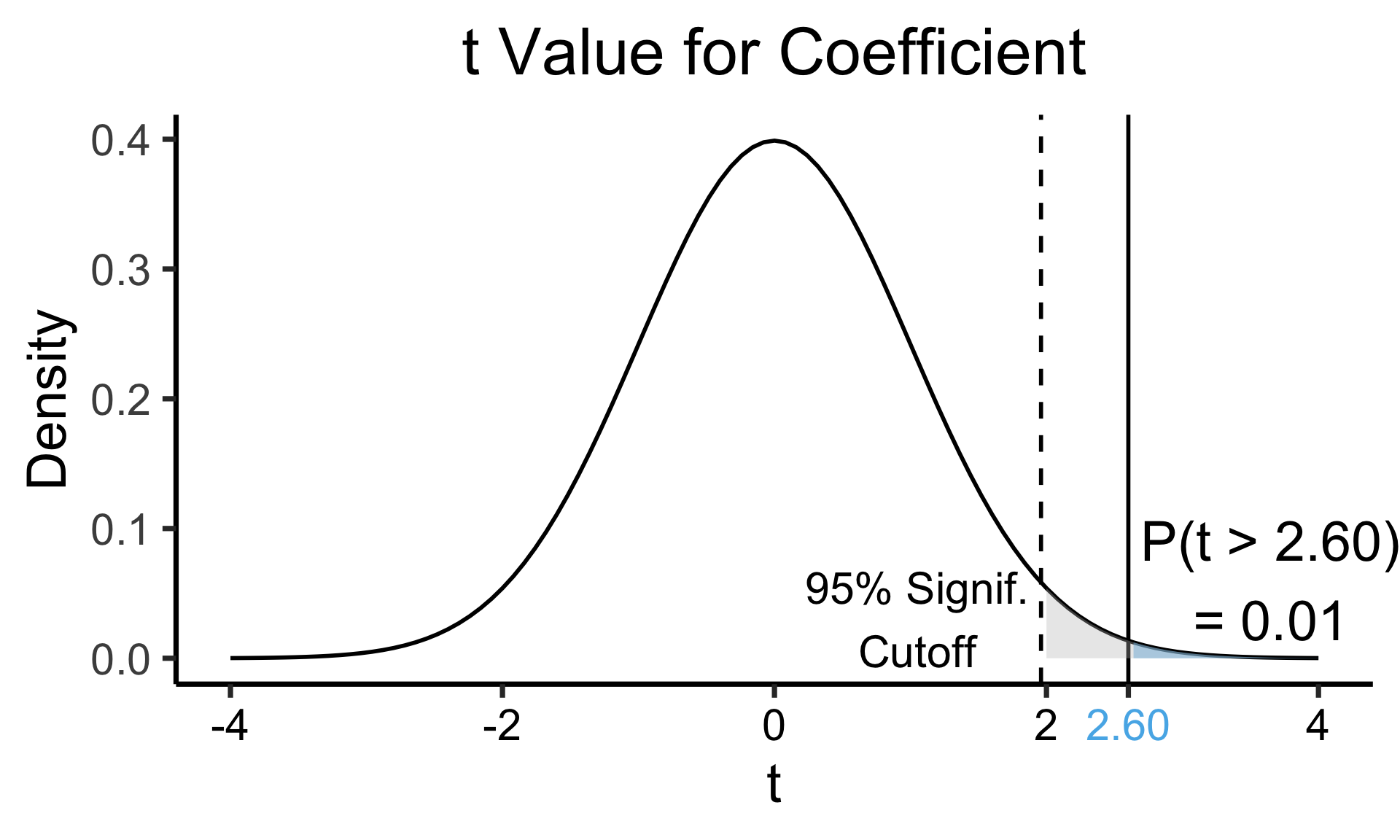

Zooming In: Significance

| Estimate | Std. Error | t value | Pr(>|t|) | ||

|---|---|---|---|---|---|

| (Intercept) | 0.61969 | 0.59526 | 1.041 | 0.3010 | |

| industrial | 0.05253 | 0.02019 | 2.602 | 0.0111 | * |

| \(\widehat{\beta}\) | Uncertainty | Test statistic | How extreme is test stat? | Statistical significance |

Code

library(ggplot2)

int_tstat <- 1.041

int_tstat_str <- sprintf("%.02f", int_tstat)

label_df_int <- tribble(

~x, ~y, ~label,

0.25, 0.05, paste0("P(t > ",int_tstat_str,")\n= 0.3")

)

label_df_signif_int <- tribble(

~x, ~y, ~label,

2.7, 0.075, "95% Signif.\nCutoff"

)

funcShaded <- function(x, lower_bound, upper_bound){

y <- dnorm(x)

y[x < lower_bound | x > upper_bound] <- NA

return(y)

}

funcShadedIntercept <- function(x) funcShaded(x, int_tstat, Inf)

funcShadedSignif <- function(x) funcShaded(x, 1.96, Inf)

ggplot(data=data.frame(x=c(-3,3)), aes(x=x)) +

stat_function(fun=dnorm, linewidth=g_linewidth) +

geom_vline(aes(xintercept=int_tstat), linewidth=g_linewidth) +

geom_vline(aes(xintercept = 1.96), linewidth=g_linewidth, linetype="dashed") +

stat_function(fun = funcShadedIntercept, geom = "area", fill = cbPalette[1], alpha = 0.5) +

stat_function(fun = funcShadedSignif, geom = "area", fill = "grey", alpha = 0.333) +

geom_text(label_df_int, mapping = aes(x = x, y = y, label = label), size = 10) +

geom_text(label_df_signif_int, mapping = aes(x = x, y = y, label = label), size = 8) +

# Add single additional tick

scale_x_continuous(breaks=c(-2, 0, int_tstat, 2), labels=c("-2","0",int_tstat_str,"2")) +

dsan_theme("quarter") +

labs(

title = "t Value for Intercept",

x = "t",

y = "Density"

) +

theme(axis.text.x = element_text(colour = c("black", "black", cbPalette[1], "black")))

Code

library(ggplot2)

coef_tstat <- 2.602

coef_tstat_str <- sprintf("%.02f", coef_tstat)

label_df_coef <- tribble(

~x, ~y, ~label,

3.65, 0.06, paste0("P(t > ",coef_tstat_str,")\n= 0.01")

)

label_df_signif_coef <- tribble(

~x, ~y, ~label,

1.05, 0.03, "95% Signif.\nCutoff"

)

funcShadedCoef <- function(x) funcShaded(x, coef_tstat, Inf)

ggplot(data=data.frame(x=c(-4,4)), aes(x=x)) +

stat_function(fun=dnorm, linewidth=g_linewidth) +

geom_vline(aes(xintercept=coef_tstat), linetype="solid", linewidth=g_linewidth) +

geom_vline(aes(xintercept=1.96), linetype="dashed", linewidth=g_linewidth) +

stat_function(fun = funcShadedCoef, geom = "area", fill = cbPalette[2], alpha = 0.5) +

stat_function(fun = funcShadedSignif, geom = "area", fill = "grey", alpha = 0.333) +

# Label shaded area

geom_text(label_df_coef, mapping = aes(x = x, y = y, label = label), size = 10) +

# Label significance cutoff

geom_text(label_df_signif_coef, mapping = aes(x = x, y = y, label = label), size = 8) +

coord_cartesian(clip = "off") +

# Add single additional tick

scale_x_continuous(breaks=c(-4, -2, 0, 2, coef_tstat, 4), labels=c("-4", "-2","0", "2", coef_tstat_str,"4")) +

dsan_theme("quarter") +

labs(

title = "t Value for Coefficient",

x = "t",

y = "Density"

) +

theme(axis.text.x = element_text(colour = c("black", "black", "black", "black", cbPalette[2], "black")))

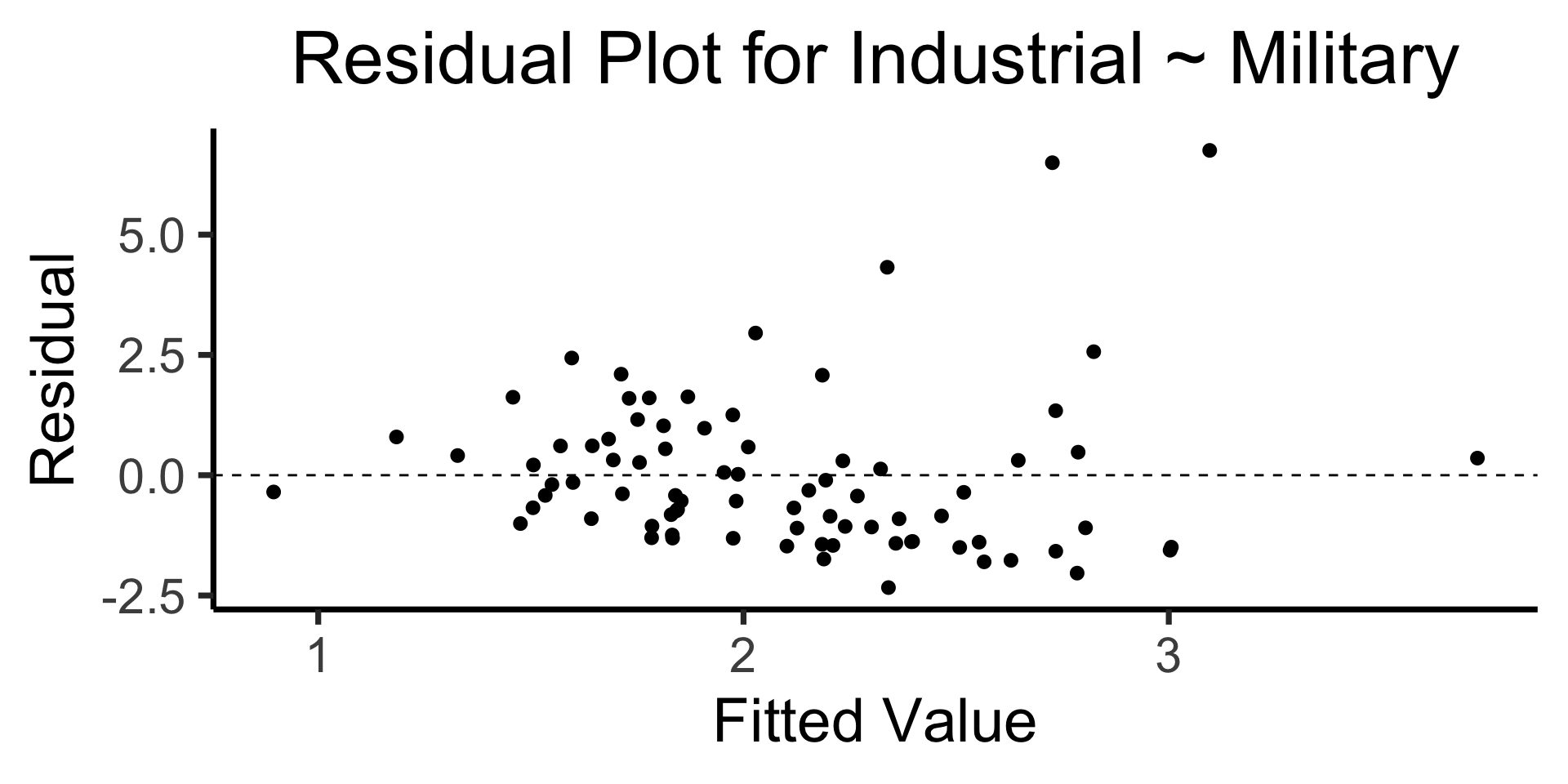

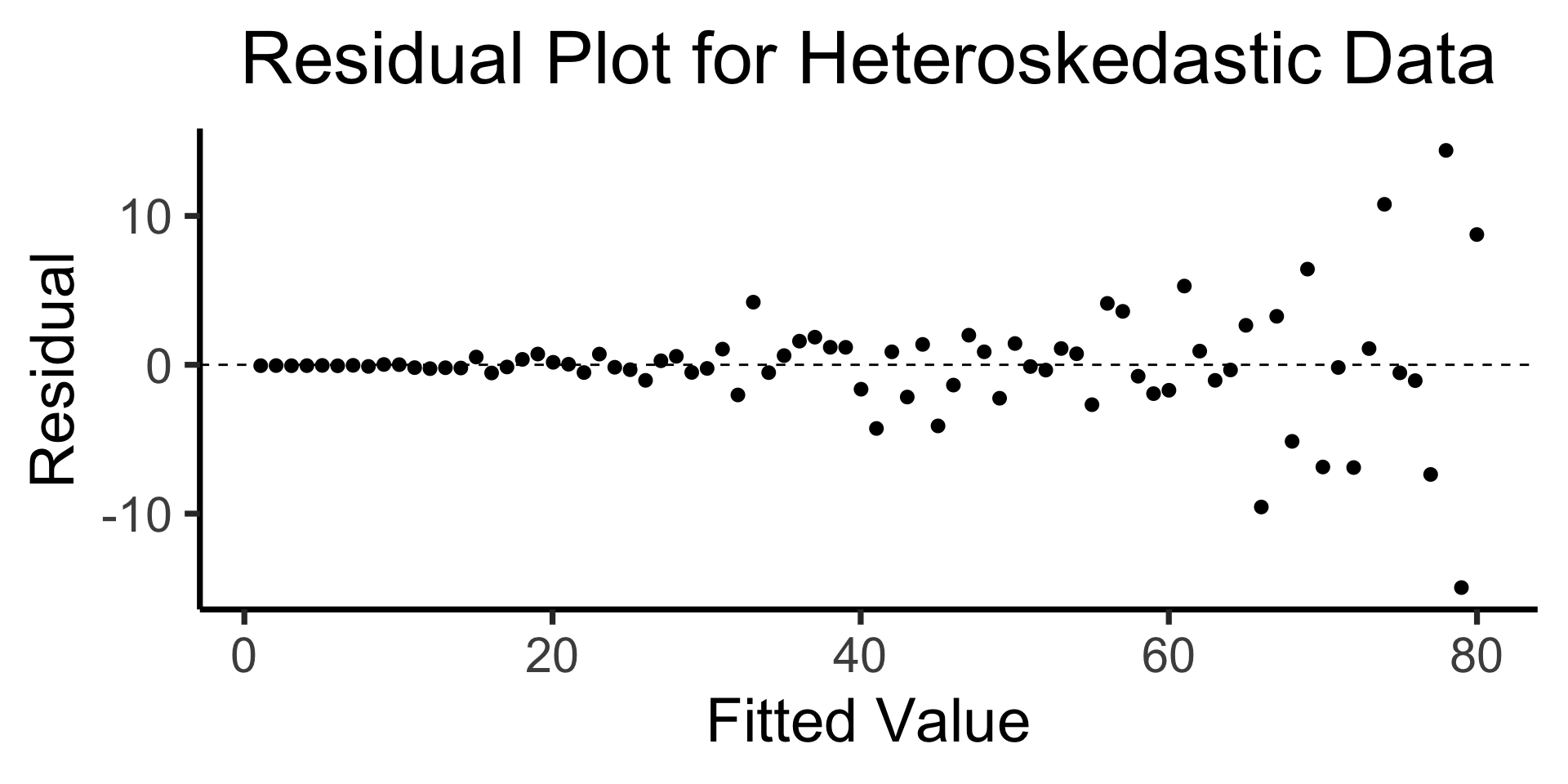

The Residual Plot

- A key assumption required for OLS: “homoskedasticity”

- Given our model \[ y_i = \beta_0 + \beta_1x_i + \varepsilon_i \] the errors \(\varepsilon_i\) should not vary systematically with \(i\)

- Formally: \(\forall i \left[ \Var{\varepsilon_i} = \sigma^2 \right]\)

Code

library(broom)

gdp_resid_df <- augment(lin_model)

ggplot(gdp_resid_df, aes(x = .fitted, y = .resid)) +

geom_point(size = g_pointsize/2) +

geom_hline(yintercept=0, linetype="dashed") +

dsan_theme("quarter") +

labs(

title = "Residual Plot for Industrial ~ Military",

x = "Fitted Value",

y = "Residual"

)

Code

x <- 1:80

errors <- rnorm(length(x), 0, x^2/1000)

y <- x + errors

het_model <- lm(y ~ x)

df_het <- augment(het_model)

ggplot(df_het, aes(x = .fitted, y = .resid)) +

geom_point(size = g_pointsize / 2) +

geom_hline(yintercept = 0, linetype = "dashed") +

dsan_theme("quarter") +

labs(

title = "Residual Plot for Heteroskedastic Data",

x = "Fitted Value",

y = "Residual"

)

Observations vs. Base Rates

Steve is very shy and withdrawn, invariably helpful but with very little interest in people or in the world of reality. A meek and tidy soul, he has a need for order and structure, and a passion for detail.

\(\Pr(\text{Steve is a librarian} \mid \text{description})?\)

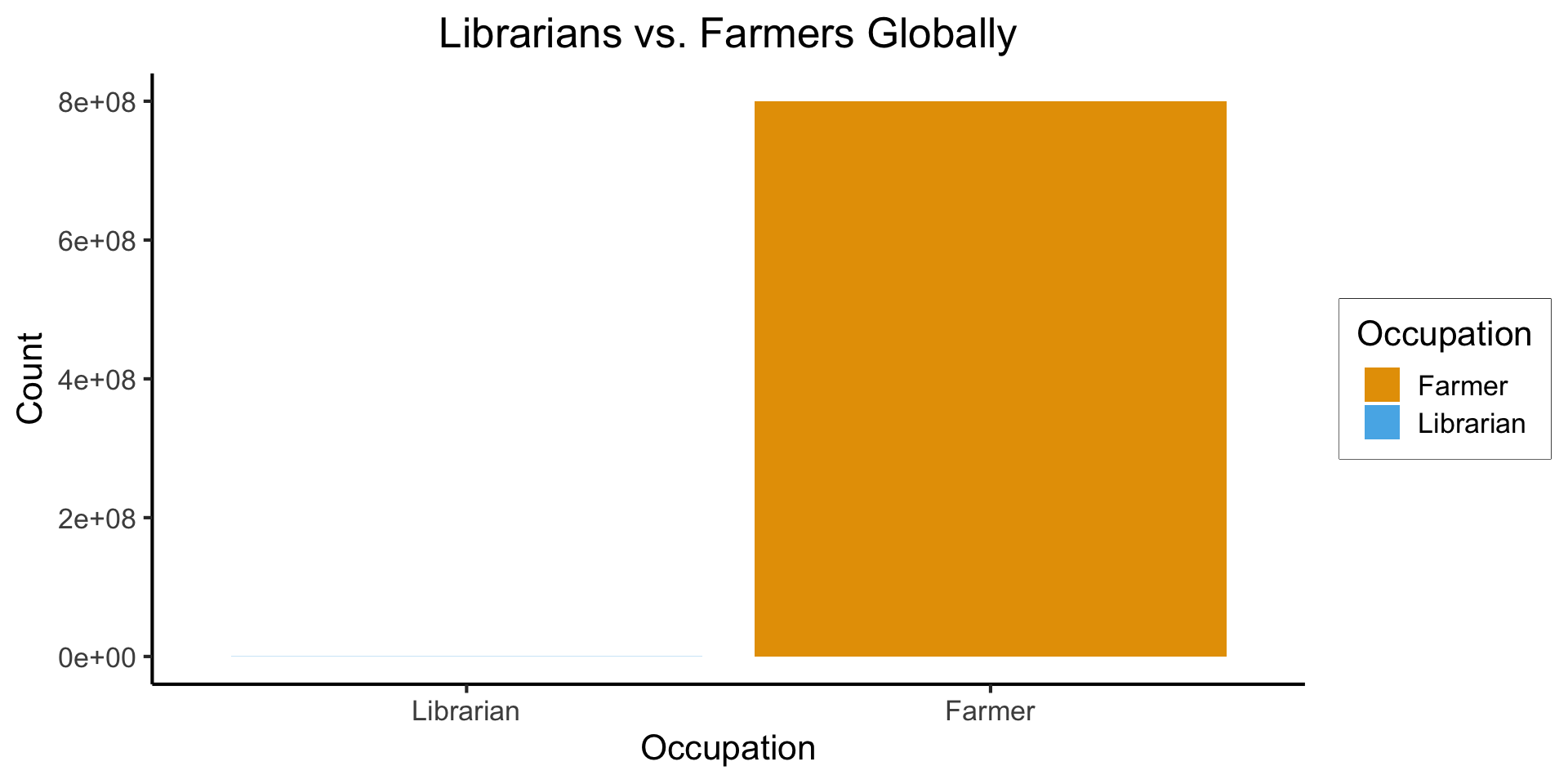

Base Rates

- Globally: ~350,000 librarians vs. ~800 million farmers

Code

library(tidyverse)

num_librarians <- 350000

num_farmers <- 800000000

occu_df <- tribble(

~Occupation, ~Count,

"Farmer", num_farmers,

"Librarian", num_librarians,

)

ggplot(occu_df, aes(x=factor(Occupation, levels=c("Librarian","Farmer")), y=Count, fill=Occupation)) +

geom_bar(stat='identity') +

dsan_theme() +

labs(

x = "Occupation",

y = "Count",

title = "Librarians vs. Farmers Globally"

)

The Difference, In Math

Code

library(tidyverse)

library(latex2exp)

my_const <- function(x) 1

my_ratio <- function(x) 1/x

#data_df <- data_df |> mutate(

# z = my_diff(x, y)

#)

#print(data_df)

x_label <- TeX("$\\mu_2$")

td_title <- TeX("Stability of $t_d$")

td_label <- TeX("$t'_d(\\mu_2)$")

base_plot <- ggplot(data=data.frame(x=c(-5,5)), aes(x=x)) +

dsan_theme("quarter") +

labs(

x = x_label

)

diff_plot <- base_plot + stat_function(

fun = my_const,

linewidth = g_linewidth

) + labs(

title = td_title,

y = td_label

)

diff_plot

tr_title <- TeX("Stability of $t_r$")

tr_label <- TeX("$t'_r(\\mu_2)$")

ratio_plot <- base_plot + stat_function(

fun = my_ratio,

linewidth = g_linewidth

) + labs(

title = tr_title,

y = tr_label

)

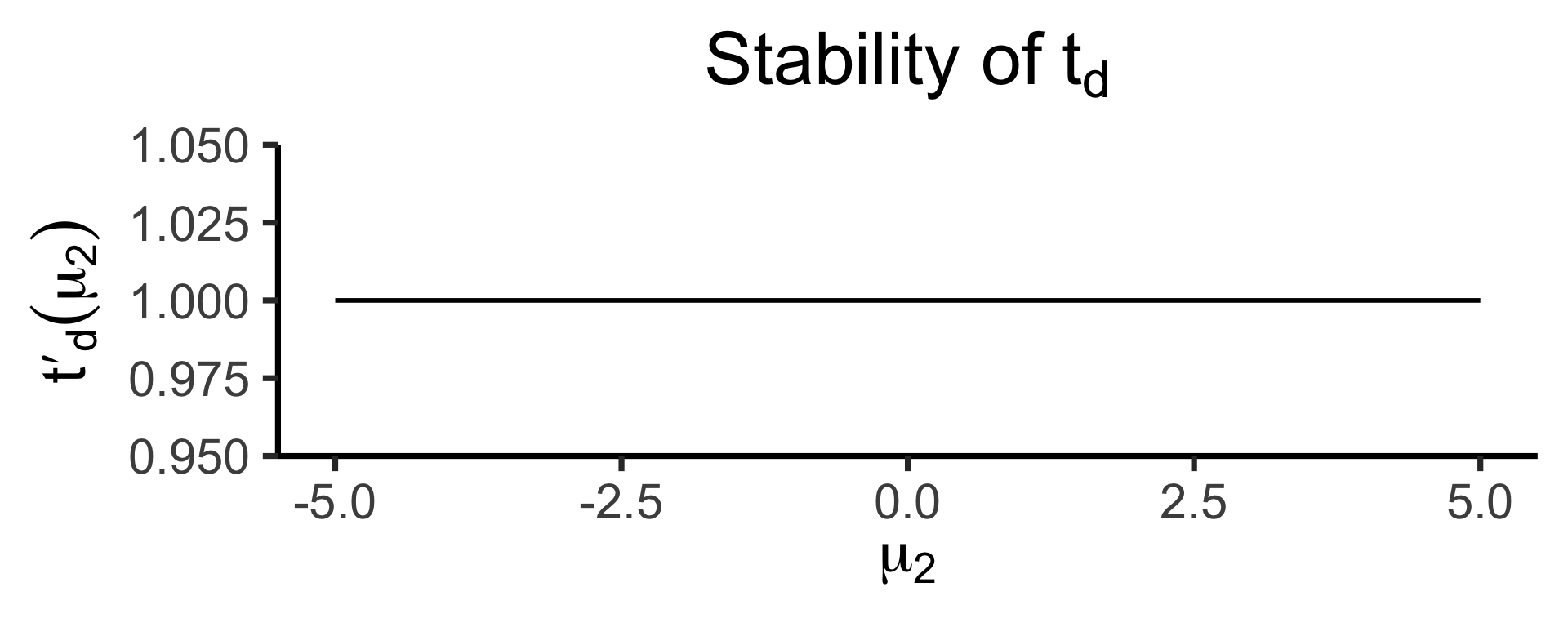

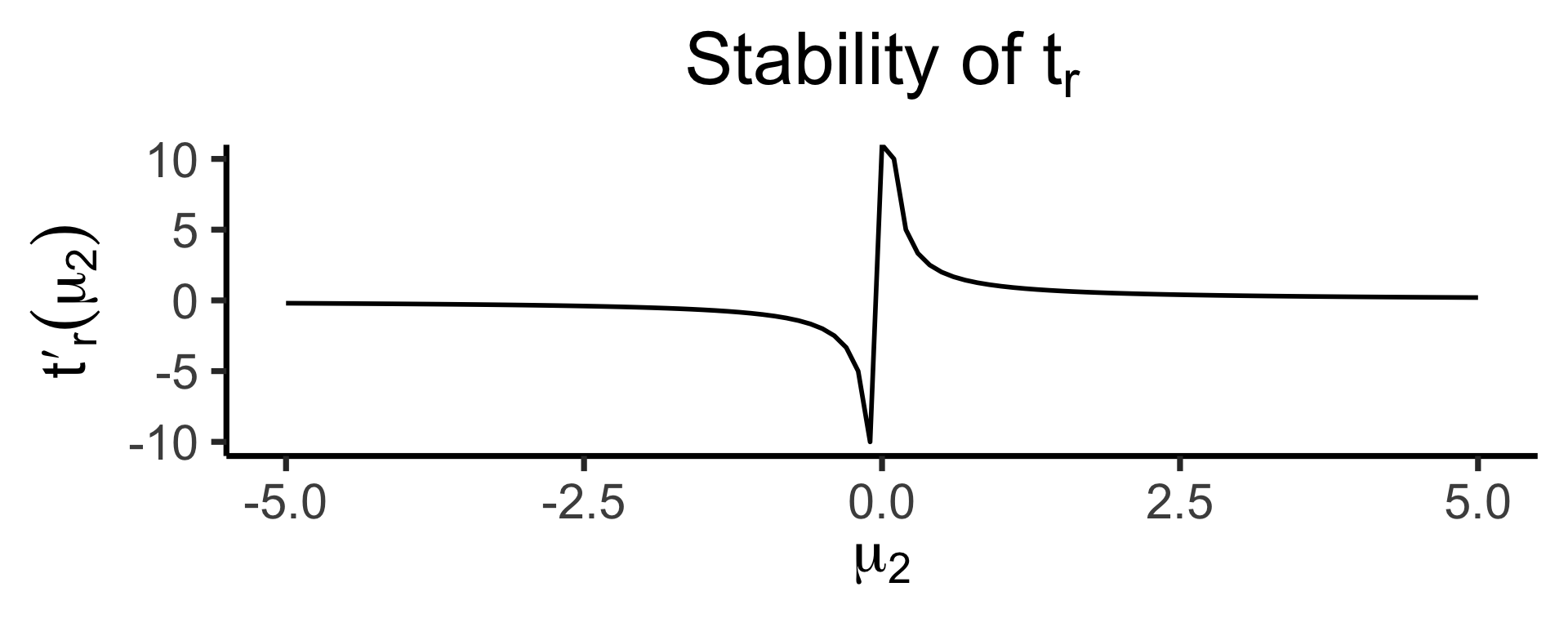

ratio_plotOur test statistic is some function \(t(\mu_1, \mu_2)\).

Let \(t_d(\mu_1, \mu_2) = \mu_1 - \mu_2\)

Let \(t_r(\mu_1, \mu_2) = \frac{\mu_1}{\mu_2}\)

How sensitive are these two ways of defining \(t\) to changes in the individual terms?

\[ t'_d(\mu_2) = \frac{\partial t^-(\mu_1, \mu_2)}{\partial \mu_1} = 1, \]

whereas

\[ t'_r(\mu_2) = \frac{\partial t^\div(\mu_1, \mu_2)}{\partial \mu_1} = \frac{1}{\mu_2} \]

\(z\)-Test \(\rightarrow\) \(t\)-Test

Code

library(tidyverse)

my_normal <- function(x) dnorm(x)

my_st <- function(x) dt(x, 2)

ggplot(data=data.frame(x=c(-3,3)), aes(x=x)) +

stat_function(

aes(color='norm'),

fun=my_normal,

linewidth = g_linewidth

) +

stat_function(

aes(color='st'),

fun=my_st,

linewidth = g_linewidth

) +

dsan_theme("half") +

scale_color_manual(

"Distribution",

values=c('norm'=cbPalette[1],'st'=cbPalette[2]),

labels=c('norm'="Standard Normal",'st'="Student's t (df=2)")

) +

remove_legend_title() +

labs(

title = "Standard Normal vs. Student's t Distribution"

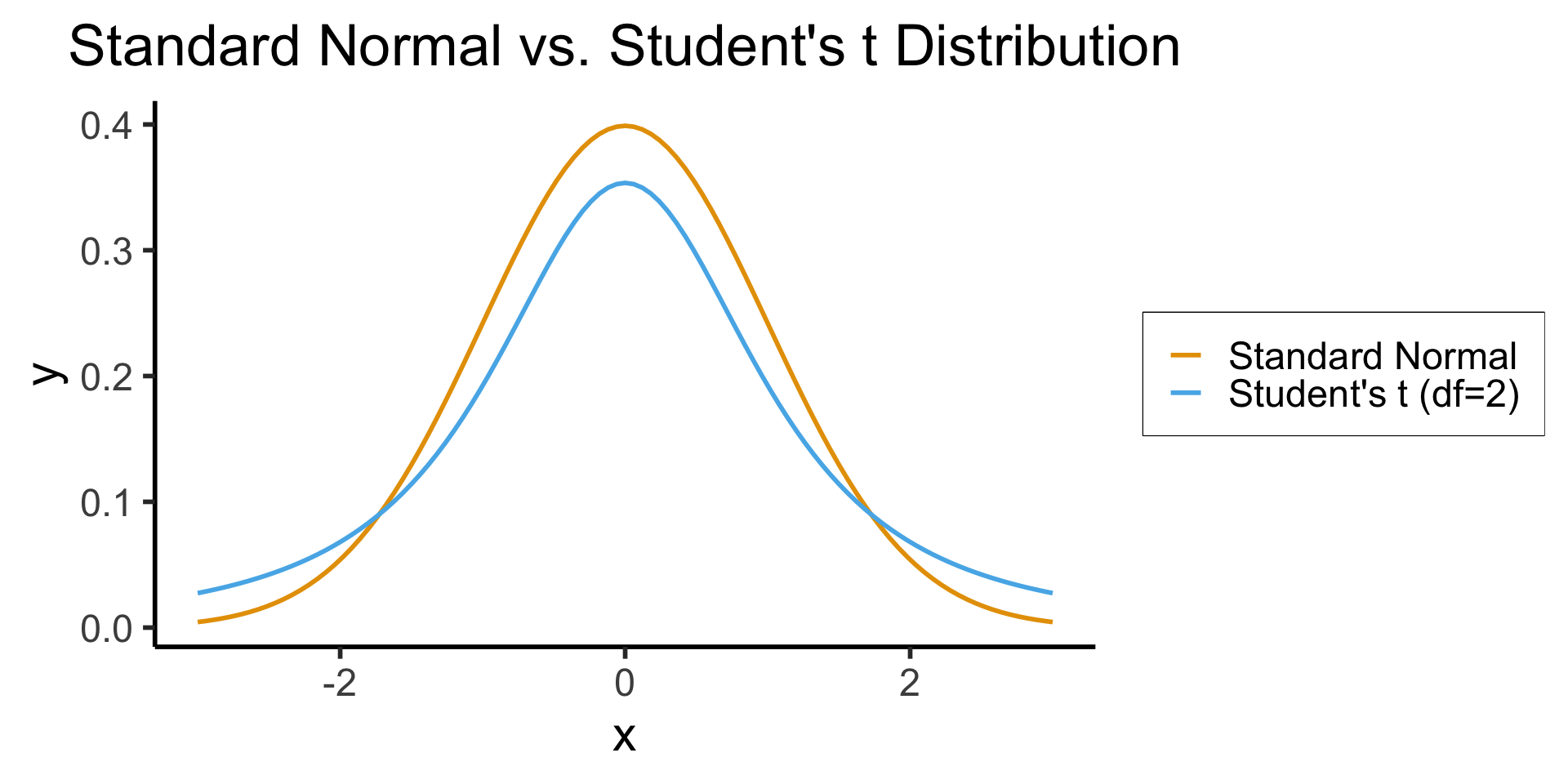

)- When we know \(\sigma^2\) but we estimate \(\mu\) from a sample, we represent our uncertainty via test statistic \(z \sim \mathcal{N}(\widehat{\mu}, \sigma^2)\)

- When we estimate both \(\mu\) and \(\sigma^2\) from a sample, we use a test statistic \(t\) with a wider “Student’s \(t\)” Distribution in place of the Normal Distribution: \(t \sim \mathcal{T}(\widehat{\mu}, \widehat{\sigma}^2, N)\)

- As \(N \rightarrow \infty\), \(\mathcal{T}_N(\widehat{\mu},\widehat{\sigma}^2,N) \rightarrow \mathcal{N}(\widehat{\mu},\widehat{\sigma}^2)\)

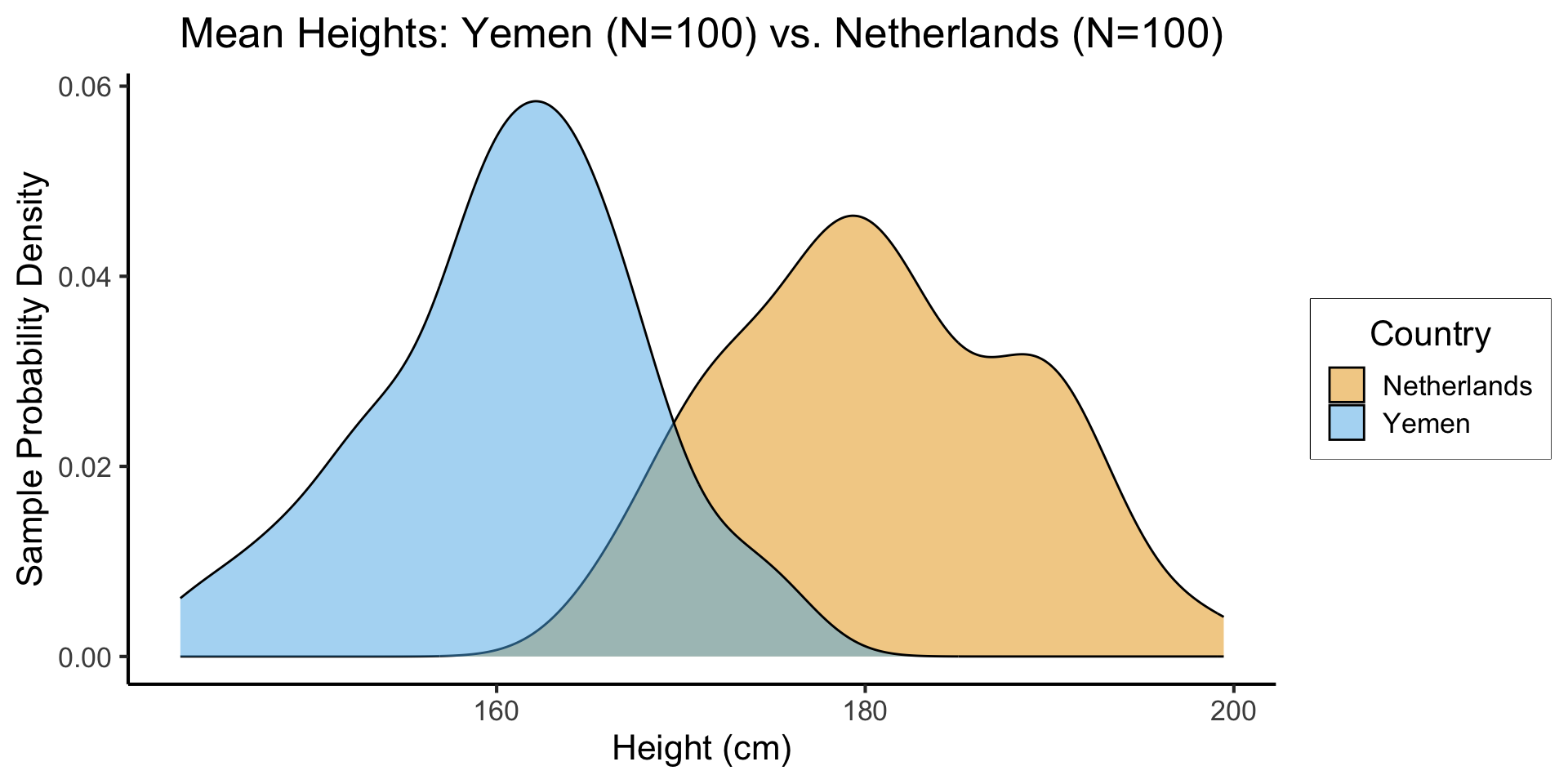

In R

- Let’s create a tibble containing samples from two populations

Code

library(tidyverse)

library(infer)

nl_height_mean <- 182.535

nl_height_sd <- 8

yemen_height_mean <- 159.887

yemen_height_sd <- 8

N <- 100

nl_sample <- rnorm(N, mean=nl_height_mean, sd = nl_height_sd)

nl_df <- tibble(height=nl_sample, Country="Netherlands")

yemen_sample <- rnorm(N, mean=yemen_height_mean, sd = yemen_height_sd)

yemen_df <- tibble(height=yemen_sample, Country="Yemen")

data_df <- bind_rows(nl_df, yemen_df)

ggplot(data_df, aes(x=height, fill=Country)) +

geom_density(alpha=0.5) +

dsan_theme() +

#xlim(150,200) +

labs(

title = "Mean Heights: Yemen (N=100) vs. Netherlands (N=100)",

x = "Height (cm)",

y = "Sample Probability Density"

) +

scale_fill_manual("Country", values=c('Netherlands'=cbPalette[1], 'Yemen'=cbPalette[2]))

- \(H_0: \mu_{\text{NL}} - \mu_{\text{Yem}} = 0\), \(H_A: \mu_{\text{NL}} - \mu_{\text{Yem}} > 0\), \(t = \overline{h}_{\text{NL}} - \overline{h}_{\text{Yem}}\)

The Chi-Squared Test of Independence